This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Growth investors are often willing to look past a company's underwhelming bottom line if they're convinced that the business has a promising future and path forward. Investors are bullish on its long-term prospects, given the company's varied AI services, which can attract customers from many different industries.

That's one of several reasons it is home to solid dividend stocks, including Pfizer (NYSE: PFE) and Bristol Myers Squibb (NYSE: BMY) , two of the leading pharmaceutical companies in the world. Sales of its coronavirus products fell off a cliff, and some of the company's older products are no longer the growth drivers they once were.

Even well-run companies face hard times now and again. In fact, it is the ability to survive the hard times that makes a company well run in the first place. Wall Street, however, tends to always react to hard times in the same way, by selling the company facing them. So far, the company's hedging efforts have held off the pain.

The company itself is still in its early stages when expenses remain high and earning a profit is still relatively far out. Or should one buy the dip in Tesla stock based on its existing profitability and prospects beyond its current EV lineup. Now the company has a steady and profitable EV business. billion in free cash flow.

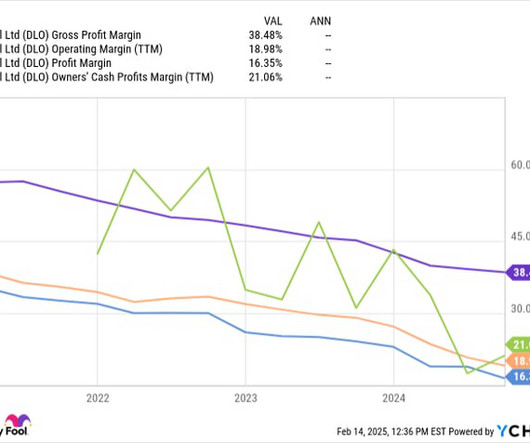

The Uruguay-based company connects merchants to more than 2 billion people in 40 countries (and counting) through more than 900 different local payment methods. The company went public in 2021, but its shares remain 81% below their all-time highs. The company went public in 2021, but its shares remain 81% below their all-time highs.

MicroStrategy's Bitcoin portfolio is equal to about a third of the company's enterprise value of $73.3 So why is this enterprise software company still so bullish on Bitcoin? Prior to 2020, most investors knew the company as a slow-growth provider of data mining and analytics software. billion, and about 1.4%

The company's "Singularity" platform identifies and stops attacks in real-time, securing digital assets and protecting sensitive data. With its technological edge and unique value proposition, the company believes it's well-positioned to tap into a $100 billion estimated total addressable market opportunity. Image source: SentinelOne.

Among the companies vying to capture this massive potential, Archer Aviation (NYSE: ACHR) , valued at $3.88 Namely, the company has forged an exclusive partnership with defense technology innovator Anduril while completing a strategic $430 million capital raise that solidifies its top-tier position within the industry.

Two of them focus on AI -- and they belong to the same company -- Alphabet (NASDAQ: GOOG) (NASDAQ: GOOGL). Google Cloud should have tremendous growth prospects as more organizations migrate to the cloud over the next decade, with AI accelerating this shift. His Pershing Square Capital Management hedge fund owns only 10 stocks.

The company developed more than 40 industry-specific solutions to help entities address their AI needs. Given the company's challenges, I see C3.ai Through the company's enterprise software, entities can develop and implement AI applications quickly. ai as an AI stock investors should continue to avoid, and here's why.

The company went from primarily serving the video-gaming market with its chips and generating less than $5 billion in annual revenue to a position as artificial intelligence (AI) chip leader. My prediction is one catalyst will help this AI powerhouse do something that no other company has ever done. Image source: Getty Images.

As the maker of graphics processing units (GPUs) the company's chips became the backbone of AI infrastructure. As a result, CUDA became the program on which developers learned to train GPUs, which is what has helped create the large moat the company sees today. It currently has about a 90% market share in GPUs as a result.

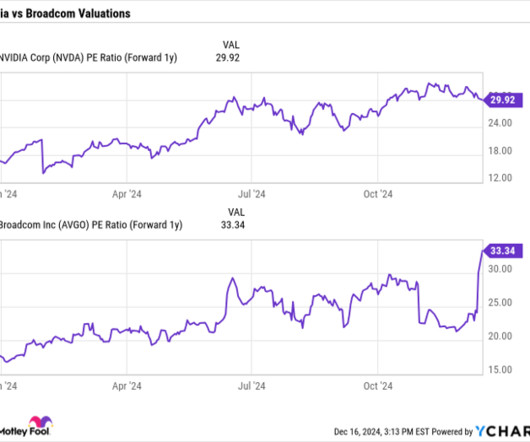

Companies responsible for AI processing have some of the largest opportunities, which is why Nvidia (NASDAQ: NVDA) , Broadcom (NASDAQ: AVGO) , and Taiwan Semiconductor Manufacturing (NYSE: TSM) could supercharge your returns in the coming years. In the company's first quarter, AI revenue jumped 77% to $4.1 trillion market by 2030.

Nvidia (NASDAQ: NVDA) was one of the biggest beneficiaries of this rally, gaining close to 702% in the past two years as companies and governments have been buying its AI chips hand over fist. The company on which Nvidia relies for manufacturing its AI chips has clocked relatively smaller gains of 142% in the last two years.

The surge in artificial intelligence (AI) has led many companies to urgently reassess their energy strategies. These companies, along with several countries, have also committed to slashing carbon emissions to help slow climate change. The company supplies about 10% of the nation's clean energy, and 90% of its energy is carbon-free.

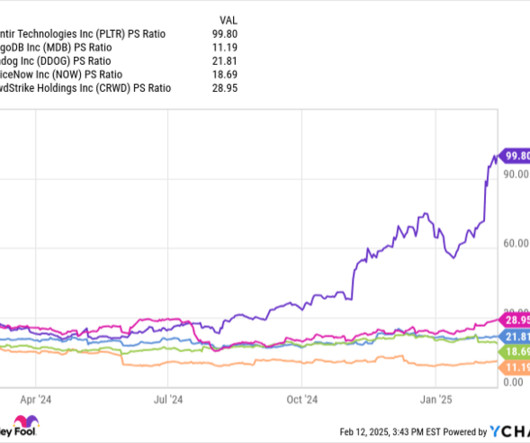

One AI company that has bucked the trend, however, is data analytics provider Palantir Technologies (NASDAQ: PLTR). What I mean by that is the company's profit margins are widening, thereby strengthening Palantir's cash-flow generation and liquidity position. The clear anomaly shown is Palantir's valuation relative to its peers.

AI agents, which leverage LLMs to perform complex, multistep tasks, could be a huge deal as companies race to adopt the technology. LLMs can do a lot of things, but they may not be well suited for the kinds of real-world tasks that will ultimately generate revenue for companies. Start Your Mornings Smarter!

Learn More The most magnificent of the seven Alphabet is one of seven leading tech companies dubbed the Magnificent Seven due to their strong growth prospects and stock price performance in recent years. That's a robust growth rate for a company as big as Alphabet. Alphabet is capitalizing on that same growth catalyst.

The tech company reported mixed quarterly results that fell short of expectations while providing ambitious long-term projections. The company's guidance for its fourth quarter of 9% revenue growth also missed previous forecasts of 9.5% The stock lost 3.2% as of 2:45 p.m. ET today and was down as much as 7.5% earlier in the day.

Felbro Food Products , a food and beverage manufacturer, has been recapitalized by Felbro Culinary Specialties , a newly formed portfolio company of Clover Capital Partners and Evanston Partners. Also included in the investment group are members of the companys management team and the founding Feldmar family.

That makes sense, given that Bitcoin hit the $100,000 mark approximately a month after the presidential election, when investors were feeling very bullish about the prospects of crypto headed into 2025. They will become more positive about its long-term price prospects, and more willing to pump additional money into the Bitcoin ETFs.

That's why FuboTV stock soared 251% the day the companies announced the pairing. It's a reasonably good fit and an apparent win for both companies. On rare occasions, our expert team of analysts issues a Double Down stock recommendation for companies that they think are about to pop.

Not only is it growing sales at a rapid clip, it's a major profit center for the company. The advent of artificial intelligence (AI), particularly around the desire of many companies to implement this technology within their own operations, makes AWS' prospects even more exciting. an unbelievable position.

The stock dropped in response, but investors are now feeling more optimistic about the company'sprospects. On rare occasions, our expert team of analysts issues a Double Down stock recommendation for companies that they think are about to pop. That's helping to drive shares higher today. at 1:45 p.m.

ET Monday morning after the company announced it will sell its Cylance endpoint security assets to private cybersecurity operator Arctic Wolf. BlackBerry already isn't a profitable company, losing $138 million over the last 12 months, and reporting $81 million in negative free cash flow.

12, raising questions about the company's growth prospects. So the company made some changes in response to the recent underperformance. On rare occasions, our expert team of analysts issues a Double Down stock recommendation for companies that they think are about to pop. Adjusted earnings jumped 44% higher to $0.59

Revenue declined, and the company warned that tariffs could slow its recovery, adding to investors' doubts about its turnaround prospects. Gross margin in the quarter was down 330 basis points to 41.5%, showing the company is still clearing inventory through markdowns. As a result, the stock was down 5.3% as of noon ET.

While it's not unusual for companies to occasionally deliver below-expected results, it's rare for this programmatic advertising company. In fact, the company has exceeded its guidance in the last eight years, and the recent miss is the first since it went public. So far, the answer is no.

The stock is down after the company posted a slight decline in revenue and subscribers last year, but its 5% dividend yield looks very tempting at these lower share prices. Last year's decline is a blip for a company that has grown its annual revenue at a 7% annualized rate over the last 10 years.

AMD (NASDAQ: AMD) management elaborated on its prospects for 2025 and beyond. On rare occasions, our expert team of analysts issues a Double Down stock recommendation for companies that they think are about to pop. And the numbers speak for themselves: Nvidia: if you invested $1,000 when we doubled down in 2009, youd have $346,349 !*

Shareholders haven't been immune to a deep reset in the company's expectations, with the stock losing 92% of its value from its all-time high. Post-pandemic revenue slump In recent years, the challenge for the company has been managing the steep revenue decline following the pandemic's peak. billion in 2022 to $3.2 billion and $2.5

Moreover, the company's CEO mentioned it has seen signs of a cautious consumer, feeding today's worries over tariffs and a spending pullback in U.S. That's because the company's fourth quarter had one extra week compared with 2023. Both of those prospects are highly suspect at the moment. Where to invest $1,000 right now?

These three stocks aren't conventionally seen as artificial intelligence (AI) stocks, yet AI is a critical part of the growth story of HVAC and building controls/software company Johnson Controls (NYSE: JCI) , and electrical solutions company nVent Electric (NYSE: NVT). Data source: Johnson Controls presentations. Chart by author.

Since the aptly named "Oracle of Omaha" became CEO in the mid-1960s, he's overseen a jaw-dropping aggregate return in his company's Class A shares (BRK.A) While Buffett is anything but tech-savvy, there are three ways his company is positioned to take advantage of the rise of AI. billionaire CEO Warren Buffett. trillion come 2030.

The company is a solid artificial intelligence (AI) expert with fantastic business prospects over the long haul. I love the company and expect it to soar for years to come -- but I would not recommend buying it at these extremely lofty prices. SoundHound AI (NASDAQ: SOUN) is an unusual beast. Let me explain.

Nvidia (NASDAQ: NVDA) has been one of the best performing stocks over the past few years, a run that catapulted it into the world's most valuable company. But over the last month or two, it slipped to second place and then -- briefly -- to third, behind two other big tech companies, Apple and Microsoft. 2 spot with a market cap of $3.41

When tech companies started investing heavily into artificial intelligence (AI), it led to robust demand for Nvidia's next-gen chips. That may prompt companies to scale back on some of their capital spending in the near future. And there's still reason to remain bullish on their prospects for even more gains in the future.

Companies that consistently raise their dividends demonstrate three crucial qualities: robust financial health, prudent management, and enduring competitive advantages. Together, these metrics help identify companies built for sustainable dividend growth. Dividend growth investing is a powerful strategy for long-term wealth creation.

If you invested $25,000 into the stock back in July 2009, when the Great Recession had just ended, that investment would now be worth a staggering $8.9 Other tech companies may still be trying to figure out AI and how best to create models and make money from new products. The company is a big player in cloud and storage solutions.

Investors may be wondering why a company at the cutting edge of AI is such a bargain. When investors are optimistic about a company's near-term growth prospects, they may be willing to pay a premium price for the stock. The company is working to expand its AI infrastructure presence considerably. It trades at 17.7

The company continues to generate ample cash flow to keep that streak going. The company operates over 50,000 miles of pipeline (along with other midstream energy assets), raking in money each month regardless of commodity price fluctuations. The good news is that its growth prospects look promising.

Further, the company plans to steadily increase its payment each quarter, targeting yearly growth at a 3% to 5% annual rate. Here's a closer look at this higher-yielding midstream company. interest in the MLP and 2% of its operating company. The oil company has been slowly monetizing that position to raise cash to repay debt.

The company is coming off yet another fantastic earnings report where its sales more than doubled from the previous year. The Great Recession began in latter stages of 2007 and ended in June 2009. Why Nvidia may struggle along with the economy The main reason to invest in Nvidia is for its promising growth prospects.

handsomely during this period as the company's recent results have been good enough to boost investors' confidence following an IT outage in July last year that sent its shares plunging. Does this mean this cybersecurity company could consider splitting its stock? That could increase the demand for a company's stock.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content