This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

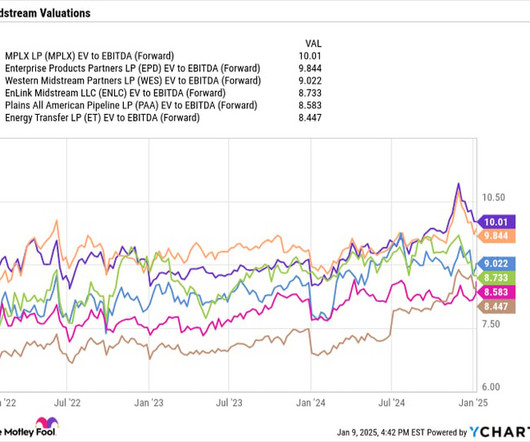

Between 2011 and 2016, MLPs traded at an average multiple of 13.7 in enterprise-value- to- EBITDA (earnings before interest, taxes, depreciation, and amortization), the most common way to value these stocks. Let's look at two great MLPs to buy right now.

Enterprise Products Partners Enterprise Products Partners (NYSE: EPD) is another large midstream operator with a strong position in Texas and the Permian. In fact, most of its natural gas pipeline and storage assets are in Texas or along the Gulf Coast. between 2011 and 2016. Data by YCharts.

The company has a solid history of finding assets that are ultimately more valuable as part of its integrated system than they are by themselves. times EV/EBITDA average multiple between 2011 and 2016. As a reference, the midstream industry as a whole traded at a 13.7

The company also recently acquired some G&P assets in the Utica and entered into an agreement to merge the Whistler Pipeline and Rio Bravo Pipeline projects into a new joint venture in order to link Permian supply to additional Gulf Coast demand, which it believes will lead to future growth opportunities. <

The midstream sector of the energy industry While the companies in the midstream space are best known for their pipeline assets, they perform a variety of tasks in the energy complex. Let's take a look at the dynamics of the industry and some stocks in the sector that look poised to outperform over the next several years.

Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. The first is that enterprisevalue takes into consideration the amount of net debt a company carries on its balance sheet. times average EV/EBITDA multiple between 2011 and 2016.

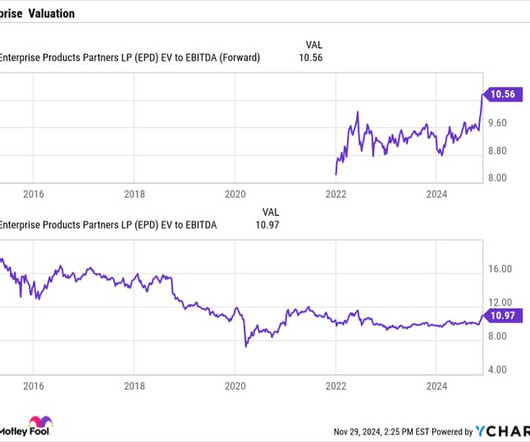

On its last earnings call, the company said this was one of the best signals in natural gas that it has seen in a long time, and that given its assets it was one of the few companies to really be able to take advantage of this opportunity. Its enterprise-value -to-EBITDA (EV/EBITDA) multiple stands at 10.5,

Enterprise said it is one of the few companies in the midstream space with the assets to benefit from increased natural demand from the data center buildout and the increased energy usage from artificial intelligence. This is because building long-life pipelines and other midstream assets is a capital intensive business.

Enterprise'sassets touch most of the midstream value chain. This helps create a natural hedge for the company, as it can direct, store, and upgrade products in order to create the most value for customers and itself. forward enterprisevalue (EV) -to- EBITDA multiple. It's also well below the 13.7

Enterprise'sassets touch most of the midstream value chain. This helps create a natural hedge for the company, as it can direct, store, and upgrade products in order to create the most value for customers and itself. forward enterprisevalue (EV) -to- EBITDA multiple. It's also well below the 13.7

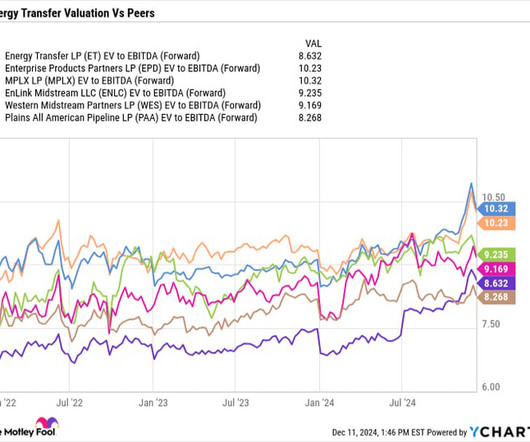

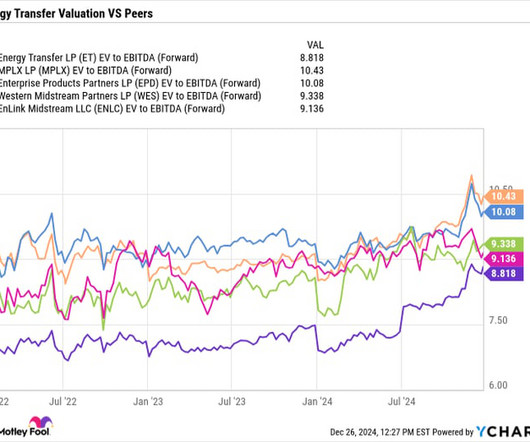

Attractive valuation Besides having some of the best growth opportunities in the pipeline space, Energy Transfer is also one of the most attractively valued MLPs. Enterprisevalue (EV) to EBITDA is typically the preferred metric investors use when valuing midstream companies. ET EV to EBITDA (Forward) data by YCharts.

times average enterprisevalue (EV) -to- EBITDA multiple between 2011 and 2016, while today most midstream stocks trade at under a 10 times multiple. EV/EBITDA tends to be the most used metric to value midstream companies, as it takes into consideration their debt positions and takes out non-cash expenses.

While we believe there is tremendous value in the intellectual property, data, and experience we've amassed from the LTC business, our view of Genworth's enterprisevalue and future potential are rooted in our 81.6% Choice 2 is one of our newer blocks with policies written between 2003 and 2011. life companies.

Since 2011, KKR portfolio companies have awarded billions of dollars in equity to over 100,000 non-senior management employees across more than 40 portfolio companies. implementation success rate, it’s clear why some of the largest companies choose Agiloft to unlock the value of contract data and accelerate business.

However, the US investor has been involved in the Costa Group journey for much longer than that, having been a majority owner of the company prior to its 2015 initial public offering (IPO) on the ASX with its first equity stake acquired in 2011, back when its name was Paine + Partners. per share 1. As a leader in U.S.

We also made meaningful headway on other strategic asset projects. We've also launched our Maritime Asset Strategy Transformation, or what we refer to internally as MAST. Our absolute emissions are over 10% lower than the 2011 peak, and that's despite capacity growth of 30% since then. A clear win-win.

Enterprisevalue (EV) -to- EBITDA is typically the most common way to value pipeline stocks, as EV takes into account net debt used to build out the asset base, while EBITDA removes the non-cash depreciation costs of those assets since the project costs are already captured in the net debt.

Despite Energy Transfer's strong position to benefit from the increasing power needs associated with AI, it is one of the cheapest MLP midstream stocks, trading at a forward enterprisevalue (EV)- to- EBITDA ratio of 8.8 The EV-to-EBITDA ratio is one of the most common ways to value pipeline stocks given their debt and growth capex.

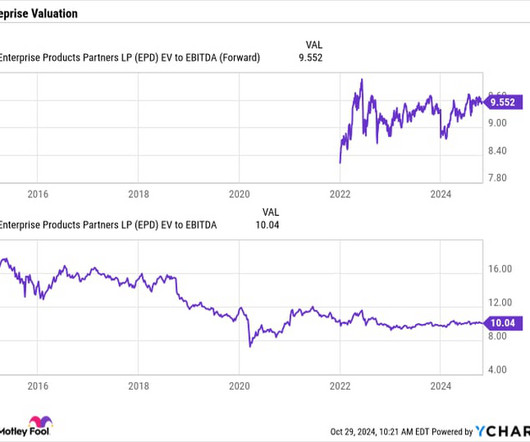

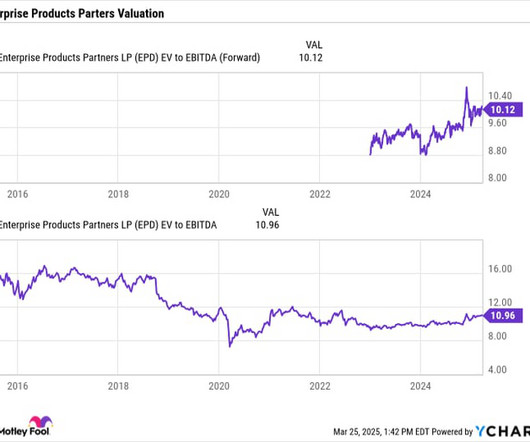

An attractive valuation Enterprise Products Partners trades at a forward enterprisevalue -to-EBITDA (EV/EBITDA) multiple of 9.8 EV/EBITDA is the most common metric used to value midstream companies because they spend a lot of money on building long-lived assets such as pipelines. based on analysts' 2025 estimates.

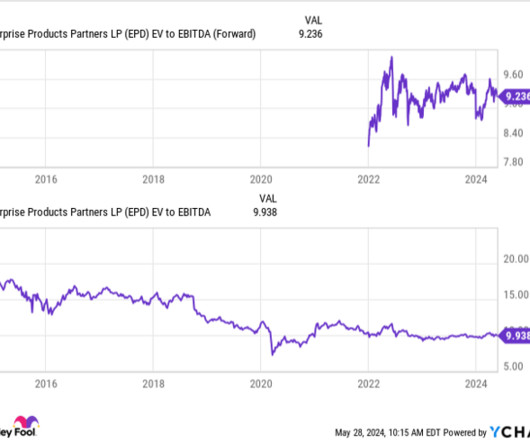

In addition to owning predictable fee-based, cash-flow-generating assets, Enterprise tends to be conservative with its balance sheet as well. It currently trades at an enterprisevalue (EV) -to-EBITDA multiple of 10, which is the most common metric used to value midstream companies.

See the 10 stocks From a business standpoint, Enterprise is an energy midstream company that owns a network of pipelines and other midstream assets. On that basis, Enterprise trades at an EV/EBITDA multiple of 10 times 2024 estimates. times, while Enterprise has generally traded at a premium given its consistent nature.

An attractive value Despite its strong performance and burgeoning growth opportunities, Energy Transfer continues to trade at both a relative and a historical discount. Enterprise trades at an EV/EBITDA multiple of 8.5 between 2011 and 2016. based on 2025 analyst estimates, which is toward the low end of valuations in the group.

If somebody else is buying them out, technically, the enterprisevalue, the actual amount being exchanged, is not 10 billion because you're buying a company with three billion just sitting in the bank. The enterprisevalue, you subtract the cash from the market cap to get the enterprisevalue, which would be $7 billion.

The offering represents the third offering by the OMERS using European currency and was led by asset managers (55 per cent) and followed by treasuries and private banks class (19 per cent), central banks and official institutions (18 per cent) and pension, insurance and other (seven per cent).

Energy Transfer (NYSE: ET) arguably has some of the best midstream assets in the country. At the same time, it also has one of the cheapest stocks in the space, with it trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just over 8 times.

Midstream companies are typically valued using an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) metric. Instead, they are spread out over the useful life of the asset, although the actual useful lives for pipelines tend to be much longer than their depreciation schedules.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content