This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Ares Capital Ares Capital is the world's largest publicly traded businessdevelopmentcompany ( BDC ). As a result, heaps of well-run midsize businesses are starving for capital and willing to pay eye-popping interest rates. In the second quarter, the average yield on debt securities in Ares Capital's portfolio was 12.2%

Investors are more than a little concerned with a debt load of about $143 billion. With customers who rarely disconnect their mobile or fiber internet connections, AT&T's telecom business is a reliably profitable one that generated $18 billion in free cash flow over the past 12 months. at the end of June from just 7.7%

Before you plow every penny you can find into these two stocks, it's important to remember that an especially high yield means the market is worried the underlying business can't continue meeting and raising its dividend commitment. The average yield Ares received from its portfolio of debt securities was a healthy 12.2%

The company has raised its dividend payout for 17 straight years. Soaring interest rates have the market worried that Verizon's debt load could become too much of a burden. Steady cash flow generation and declining capital expenditures suggest its debt load will be manageable. Shares of Verizon offer a huge 7.7%

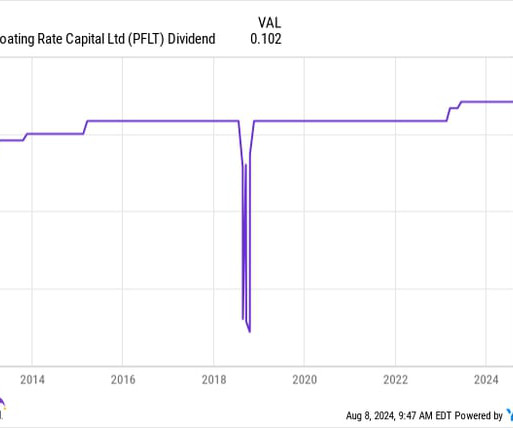

Time to pounce: PennantPark Floating Rate Capital (10.82% yield) A second ultra-high-yield dividend stock that's begging to be bought in May is off-the-radar businessdevelopmentcompany (BDC) PennantPark Floating Rate Capital (NYSE: PFLT). billion) is tied up in debt securities. billion) is tied up in debt securities.

Ares Capital (NASDAQ: ARCC) and PennantPark Floating Rate Capital (NYSE: PFLT) are a pair of well-manged businessdevelopmentcompanies (BDCs) that offer eye-popping dividend yields. banks have been increasingly hesitant to lend to businesses directly for decades. Just three companies representing 1.5%

PennantPark Floating Rate Capital PennantPark Floating Rate Capital is a businessdevelopmentcompany ( BDC ). That means it's essentially a bank that makes high-interest loans to midsize businesses that can't get regular banks to return their calls. The average yield PennantPark received from borrowers reached 12.1%

PennantPark Floating Rate Capital PennantPark Floating Rate Capital is a businessdevelopmentcompany (BDC). For decades, America's largest banks have stepped back from lending directly to mid-sized businesses. weighted-average yield on its debt investments. yield at recent prices. In Q2, the BDC reported a 12.1%

But Ares executives insist their firm remains steadfast in its goal of offering institutional investors more than just private debt. William Benjamin, head of Ares’ real estate group, describes the parent company’s prowess in private debt as an invaluable fundraising tool. Yet even there, private credit plays an outsize role.

However, the US investor has been involved in the Costa Group journey for much longer than that, having been a majority owner of the company prior to its 2015 initial public offering (IPO) on the ASX with its first equity stake acquired in 2011, back when its name was Paine + Partners. million, lease liabilities of $582.9

PennantPark Floating Rate Capital Direct lending between traditional banks and midsized American businesses hardly exists anymore. Instead, businessdevelopmentcompanies ( BDCs ) such as PennantPark Floating Rate Capital are raking in profits by originating relatively high-interest loans to capital-starved middle-market companies.

See the 10 stocks Dividend yields among most S&P 500 stocks aren't appealing, but there are a few businessdevelopmentcompanies (BDCs) that deserve more attention from income-seeking investors than they've been getting. It's been able to raise or maintain its dividend payout every year since it started paying one in 2011.

PennantPark Floating Rate Capital PennantPark Floating Rate Capital is a businessdevelopmentcompany ( BDC ), which means it lends to mid-sized businesses. American banks have been less inclined to lend directly to businesses for decades. The average yield on debt investments in this BDC's portfolio was 11.5%

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content