This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As a result, most pay out very generous distributions, which are similar to dividends, but much of the payout is considered a return of capital. Between 2011 and 2016, MLPs traded at an average multiple of 13.7 times last quarter based on its distributable cash flow (operating cash flow minus capital expenditures for maintenance ).

Meanwhile, Enterprise Products Partners has entered more of a growth phase, beginning to ramp up capital expenditures ( capex ) given the growth opportunities it is seeing. Cheap stocks Energy Transfer, Enterprise Products Partners, and Williams all have strong growth ahead from increasing natural gas demand. Data by YCharts.

Incline Equity Partners has announced the above-target final closing of Incline Ascent Fund II LP (Ascent II), with $500 million in committed capital. billion of capital. Pittsburgh-headquartered Incline was formed in 2011 and is led by Mr. Glover and Senior Partner Leon Rubinov.

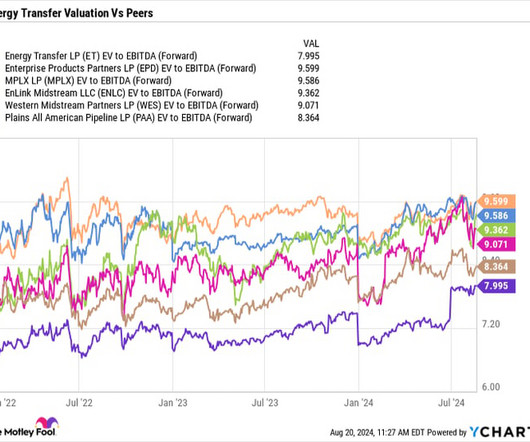

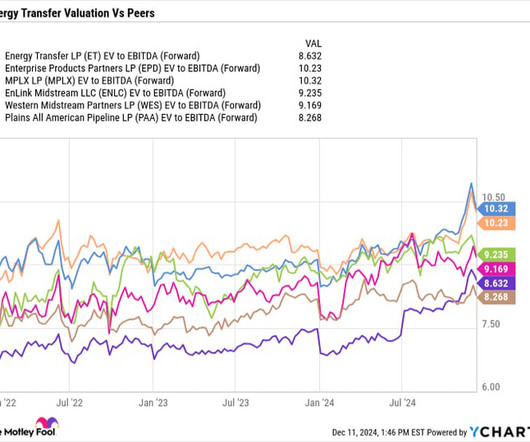

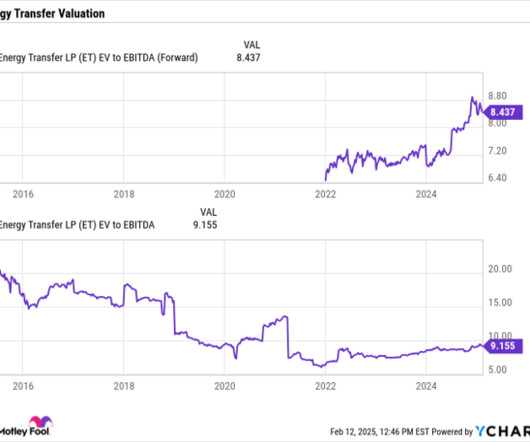

billion in growth capital expenditures (capex) on new projects. Multiple expansion opportunities From a valuation perspective, Energy Transfer is the cheapest stock among its master limited partnership (MLP) midstream peers, trading at 8x on a forward enterprisevalue -to-adjusted EBITDA basis. billion to $3.5 billion $15.88

Today, Chevron is the world's third largest oil company by market capitalization , just behind Saudi Arabian Oil Group -- better known as Saudi Aramco -- and ExxonMobil. In 2020, which was an exceptionally challenging year for the oil and gas industry, Chevron swiftly cut production and slashed capital spending by nearly 35%.

times based on its non-consolidated distributable cash flow, which is cash flow before growth capital expenditures (capex) , and payout to partners. times EV/EBITDA average multiple between 2011 and 2016. Its second-quarter results reported a distribution coverage ratio of over 1.8

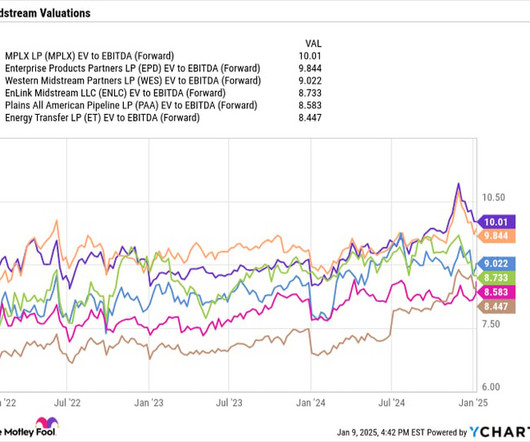

It is planning to spend $950 million in growth capital expenditure (capex) this year. < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6

.” Incline Equity invests in North America-based companies with enterprisevalues of $25 million to $750 million. Sectors of interest include services, value-added distribution, and specialized light manufacturing. billion of capital.

While similar, distributions include a return on capital that is untaxed until the units are typically sold, making them tax-deferred. This is based on its non-consolidated distributable cash flow, which is its cash flow before growth capital expenditures (capex). times average EV/EBITDA multiple between 2011 and 2016.

Charterhouse Capital Partners (Charterhouse), a private equity firm focused on investments in mid-market European companies in the services and healthcare sectors with an enterprisevalue of between €150m and €1bn, has invested in sports marketing company Two Circles.

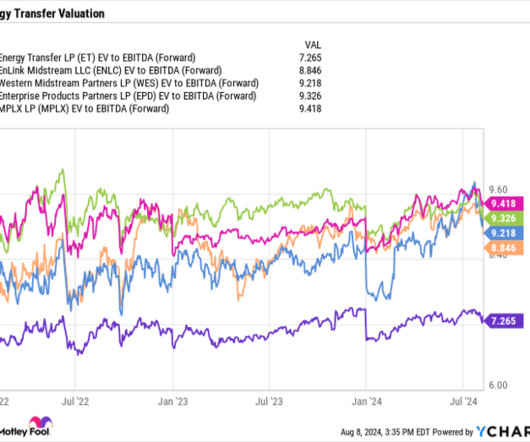

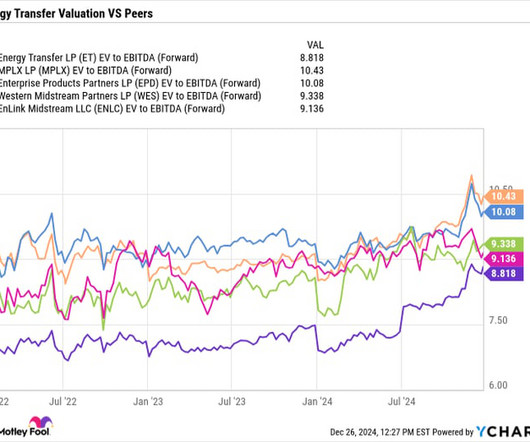

Distributable cash flow (DCF) to partners, which is how much cash the company generates before growth capital expenditures (capex) , was $2 billion, up nearly 32% from a year ago. An attractively valued stock Energy Transfer trades at an attractive forward enterprisevalue (EV) -to-EBITDA multiple of just 7.3x.

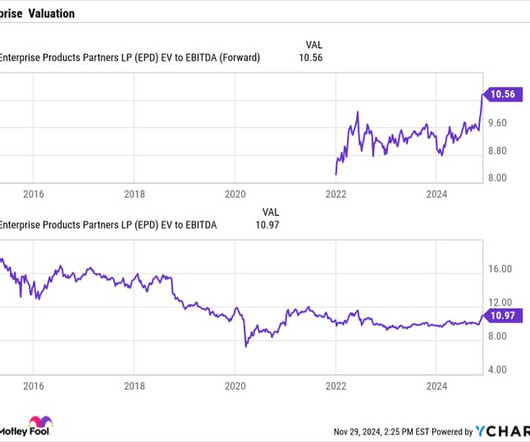

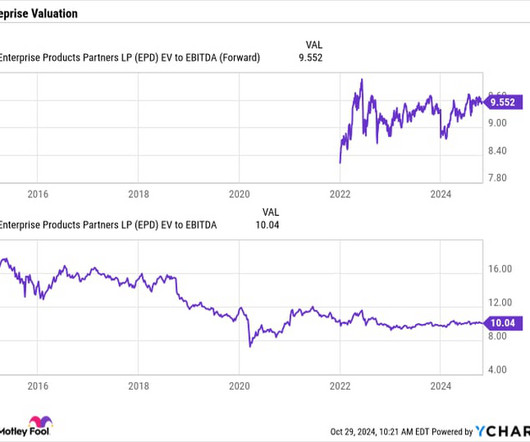

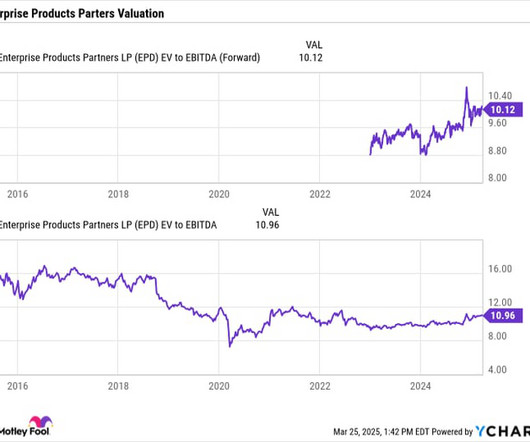

Meanwhile, it has historically been conservative with its leverage, distribution coverage ratio, and growth capital expenditure (capex) spending. Since 2018, Enterprise has averaged an approximately 13% return on invested capital (ROIC) on its growth projects. Its enterprise-value -to-EBITDA (EV/EBITDA) multiple stands at 10.5,

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

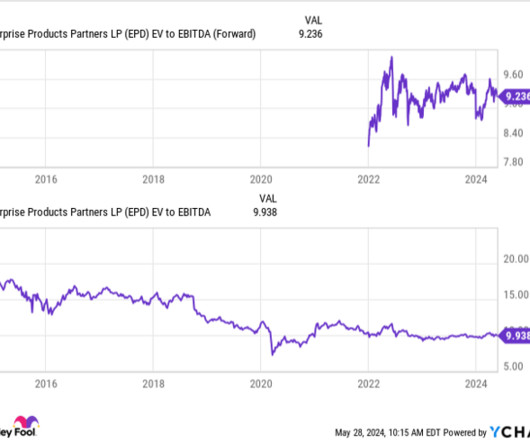

DCF is similar to free cash flow, except that operating cash flow is only reduced by maintenance capital expenditures ( capex ) and not growth capex. Based on its DCF, Enterprise's distribution coverage ratio was 1.7x. Enterprise currently has $6.9 On that front, Enterprise trades at a forward EV/EBITDA multiple of 9.5

Its FCF was lower compared to a year ago as the company increased its capital expenditures (capex) on new growth projects. Enterprise slowed down its growth projects during the pandemic but last year started to ramp them up once again. plus multiple between 2011 and 2016 when the companies were generally in worse financial shape.

Last quarter, Enterprise had a robust distribution coverage of 1.7 times based on its distributable cash flow (DCF), which is its operating cash flow minus maintenance capital expenditures (capex). Given the debt and capex spending in the midstream space, this tends to be one of the most common metrics by which to value these stocks.

In the past, it has talked about a $2 billion to $3 billion growth capital expenditure (capex) run rate, but it recently boosted that to between $2.5 Attractive valuation Besides having some of the best growth opportunities in the pipeline space, Energy Transfer is also one of the most attractively valued MLPs. billion and $3.5

times average enterprisevalue (EV) -to- EBITDA multiple between 2011 and 2016, while today most midstream stocks trade at under a 10 times multiple. EV/EBITDA tends to be the most used metric to value midstream companies, as it takes into consideration their debt positions and takes out non-cash expenses.

One final factor may be competition for dollars from large capital allocators. Many large pensions and endowments are eschewing public stocks in favor of private equity and venture capital these days. Between 1999 and 2011, the small-cap Russell 2000 index outperformed the S&P 500 index by a whopping 6.5

Free cash flow to the holding company remained strong, driven by Enact's return of capital and tax payments in 2023 from Enact and the U.S. GAAP accounting is noneconomic and has no impact on cash flows, capital levels, statutory results, or how we manage the business. We have no plans to put additional capital into the U.S.

Existing investor FTV Capital to invest additional capital in the Company NEW YORK & REDWOOD CITY, Calif.–( Since FTV’s initial investment in 2020, Agiloft has driven impressive growth by delivering a truly unique no-code platform to a quickly growing customer base globally,” said Alex Mason, Partner at FTV Capital.

However, the US investor has been involved in the Costa Group journey for much longer than that, having been a majority owner of the company prior to its 2015 initial public offering (IPO) on the ASX with its first equity stake acquired in 2011, back when its name was Paine + Partners. per share 1.

Our absolute emissions are over 10% lower than the 2011 peak, and that's despite capacity growth of 30% since then. Please see our Terms and Conditions for additional details, including our Obligatory Capitalized Disclaimers of Liability. Last year, we also exceeded our industry-leading shore power capability goal.

Buffett has been in this position in the past, most notably during the financial crisis when he prudently invested $5 billion in preferred stock issued by Bank of America in 2011 and converted those warrants in 2017 for a $15 billion profit. Is Berkshire Hathaway stock a buy, hold, or sell?

The difference between the two is tax-related, as distributions have a return of capital component that is tax-deferred. The distribution is well covered by its distributable cash flow (DCF), which is its operating cash flow minus maintenance capital expenditures (capex). Last quarter, the company paid out $1.1

billion annually in growth capital expenditure (capex) given the opportunities it is seeing. Despite Energy Transfer's strong position to benefit from the increasing power needs associated with AI, it is one of the cheapest MLP midstream stocks, trading at a forward enterprisevalue (EV)- to- EBITDA ratio of 8.8 billion and $3.5

Learn More Ramping up growth spending Energy Transfer plans to spend $5 billion in capital expenditures (capex) on growth projects in 2025. From a valuation perspective, the stock trades at an enterprisevalue (EV) -to-EBITDA multiple of about 8.5 times between 2011 and 2016. times the high end of its 2025 guidance.

Enterprise Products Partners (NYSE: EPD) continued to display its consistent nature when its reported its fourth-quarter earnings results on Tuesday. Meanwhile, the pipeline operator continues to ramp up its growth capital expenditures ( capex ) as it sees growing strong opportunities. It also spent $63 million buying back 2.1

In addition to owning predictable fee-based, cash-flow-generating assets, Enterprise tends to be conservative with its balance sheet as well. Operating a midstream company is capital-intensive, as growth comes from constructing new pipelines and facilities. DCF is operating cash flow minus maintenance capital expenditures.

Typically, a large percentage of distributions are treated as a return of capital. This also means that it is essentially taxed later at the lower capital gains tax rate and not as ordinary income. Enterprise Products Partners has a robust and growing distribution Enterprise currently sports an attractive forward yield of 6.3%.

To take advantage of the growing opportunities it is seeing, Energy Transfer plans to significantly boost its growth capital expenditure (capex) this year, taking it to $5 billion in 2025 from $3 billion last year. between 2011 and 2016. Meanwhile, the midstream MLP group as a whole traded at an average EV/EBITDA multiple of 13.7

When you multiply those things, that gives you a sense of the value of the equity of a company the market capitalization. If somebody else is buying them out, technically, the enterprisevalue, the actual amount being exchanged, is not 10 billion because you're buying a company with three billion just sitting in the bank.

Distributable cash flow (DCF) to partners, which is how much cash the company generates before growth project capital expenditures (capex) , edged up by $4 million to $1.99 Energy Transfer actually lowered its growth capital expenditures (capex) estimate for the year, now expecting to spend between $2.8 billion and $3 billion.

The total enterprisevalue of the transaction totalled 1.53 The Canada Pension Plan Investment Board is confirming the inclusion of Cedar Leaf Capital, an Indigenous-owned investment dealer, to its syndicate of dealers. based Aberdeen, Glasgow and Southampton airports. billion , having received all relevant regulatory approvals.

At the same time, it also has one of the cheapest stocks in the space, with it trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just over 8 times. times that midstream master limited partnerships (MLPs) averaged between 2011 and 2016.

Given the opportunities the company is seeing in this environment, it has upped its capital expenditure (capex) budget this year to take advantage of attractive project economics. Midstream companies are typically valued using an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) metric.

Pepsi has been in business for more than a century and has a market capitalization surpassing $200 billion. For this reason, it might be surprising to suggest that companies that were only founded in 2011 and 2012 could be worth more than Pepsi and Starbucks within five years. See the 10 stocks PEP Market Cap data by YCharts.

Palantir was backed by the CIA's venture capital arm, In-Q-Tel, and it was reportedly used to track down Osama Bin Laden in 2011. Its enterprisevalue of $172.3 It developed a streamlined data collection and analytics platform that broke down the inefficient silos between U.S. By the time it went public, most U.S.

Enterprise, meanwhile, plans to increase its growth capex this year to between $4 billion and $4.5 Enterprise has a history of being prudent with its capital expenditures (capex) , so it is notable that it plans to increase it nicely this year. billion, excluding any acquisitions, up from $3.9 billion in 2024.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content