This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

billion in growth capex a year would allow it to pay its distribution while having money left over from its cash flow to pay down debt and/or buy back stock. This metric takes into consideration a company's net debt while taking out non-cash items and is the most widely used way to value midstream companies. billion in debt, $3.9

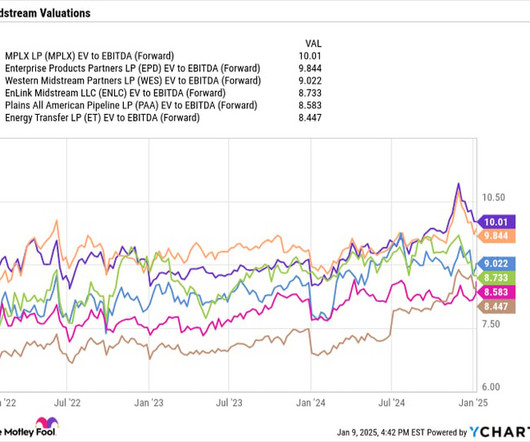

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6

Chevron's capital discipline shone through in 2022, when its return on capital employed (ROCE) hit 20%, a level last seen in 2011. Pare debt and maintain a strong balance sheet. Right now, Chevron is trading significantly below its five-year averages on two key valuation counts -- price-to-cash flow and enterprisevalue-to- EBITDA.

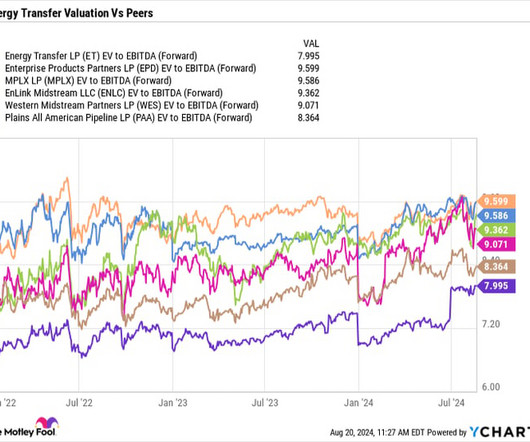

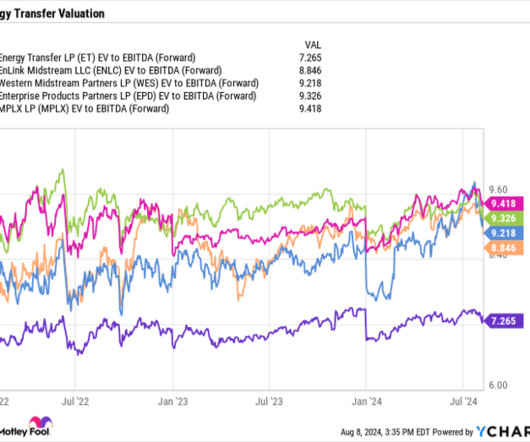

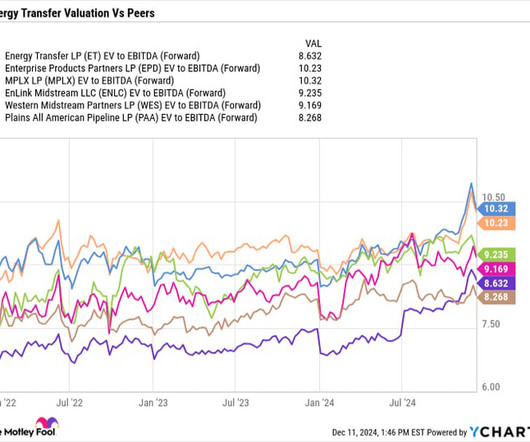

At the same time, Energy Transfer continues to trade at a forward enterprise-value -to- EBITDA multiple of 8 times based on 2025 estimates, which is well below historical levels, not to mention one of the lowest valuations in the MLP space. times EV/EBITDA average multiple between 2011 and 2016.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower.

Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. The first is that enterprisevalue takes into consideration the amount of net debt a company carries on its balance sheet. times average EV/EBITDA multiple between 2011 and 2016.

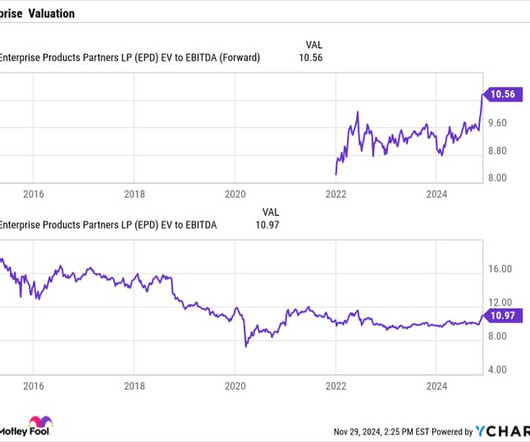

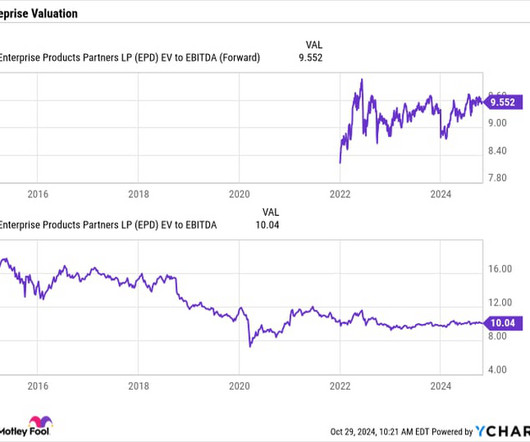

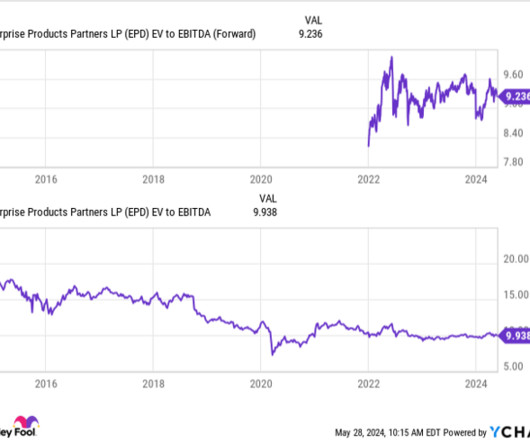

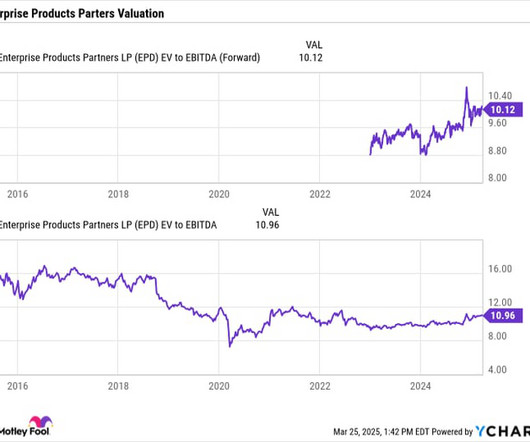

Last quarter, Enterprise Products Partners had a distribution coverage ratio of 1.7. The company's balance sheet also remains in good shape, with net debt (adjusted for equity credit in junior subordinated notes) standing at three times adjusted EBITDA. Its enterprise-value -to-EBITDA (EV/EBITDA) multiple stands at 10.5,

billion in cash toward paying down debt. An attractively valued stock Energy Transfer trades at an attractive forward enterprisevalue (EV) -to-EBITDA multiple of just 7.3x. EV/EBITDA multiple the stocks averaged between 2011 and 2016. It has paid $2.3 billion total for the year. That would give it about $1.2

It ended the quarter with leverage of 3x, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. An attractive valuation One of the most common ways investors value midstream companies is by using an enterprise-value -to-EBITDA (EV/EBITDA) multiple.

It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. The company trades at a forward- enterprisevalue -to-adjusted - EBITDA (EV/EBITDA) multiple of about 9.5. plus multiple between 2011 and 2016 when the companies were generally in worse financial shape.

Last quarter, Enterprise had a robust distribution coverage of 1.7 Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ).

The company defines leverage as net debt adjusted for equity credit in junior subordinated notes divided by adjusted EBITDA.) Enterprise currently has a robust forward yield of 7.2% Inexpensive valuation Despite its high yield and growth opportunities, Enterprise is still trading at an inexpensive valuation of a 9.3

The company defines leverage as net debt adjusted for equity credit in junior subordinated notes divided by adjusted EBITDA.) Enterprise currently has a robust forward yield of 7.2% Inexpensive valuation Despite its high yield and growth opportunities, Enterprise is still trading at an inexpensive valuation of a 9.3

times average enterprisevalue (EV) -to- EBITDA multiple between 2011 and 2016, while today most midstream stocks trade at under a 10 times multiple. EV/EBITDA tends to be the most used metric to value midstream companies, as it takes into consideration their debt positions and takes out non-cash expenses.

Attractive valuation Besides having some of the best growth opportunities in the pipeline space, Energy Transfer is also one of the most attractively valued MLPs. Enterprisevalue (EV) to EBITDA is typically the preferred metric investors use when valuing midstream companies. Image source: Getty Images.

In fact, roughly 30% of the debt of companies in the Russell 2000 small cap index is floating-rate , compared with only 6% in the S&P 500. Between 1999 and 2011, the small-cap Russell 2000 index outperformed the S&P 500 index by a whopping 6.5 in only one or two end markets. That makes them highly intersest-rate sensitive.

Strong EBITDA and cash from operations also propelled us on our journey to reduce the debt load necessitated during the pause in operations. Our absolute emissions are over 10% lower than the 2011 peak, and that's despite capacity growth of 30% since then. billion of our highest-cost debt. billion of debt cost.

While we believe there is tremendous value in the intellectual property, data, and experience we've amassed from the LTC business, our view of Genworth's enterprisevalue and future potential are rooted in our 81.6% Choice 2 is one of our newer blocks with policies written between 2003 and 2011. life companies.

However, the US investor has been involved in the Costa Group journey for much longer than that, having been a majority owner of the company prior to its 2015 initial public offering (IPO) on the ASX with its first equity stake acquired in 2011, back when its name was Paine + Partners. per share 1. million, lease liabilities of $582.9

Let's look at three reasons why I think the stock might be worth a $1,000 (or more) investment if you have cash available that isn't needed for monthly bills, an emergency fund, or to pay off short-term debt. Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free 1.

Currently, Buffett is placing the lion's share of that cash in Treasury bills -- a debt instrument backed by the U.S. While some of its major holdings, like Apple , Bank of America, and Coca-Cola would be out of the question due to their high enterprisevalues , others like DaVita , Kraft-Heinz , and Sirius XM could be in play.

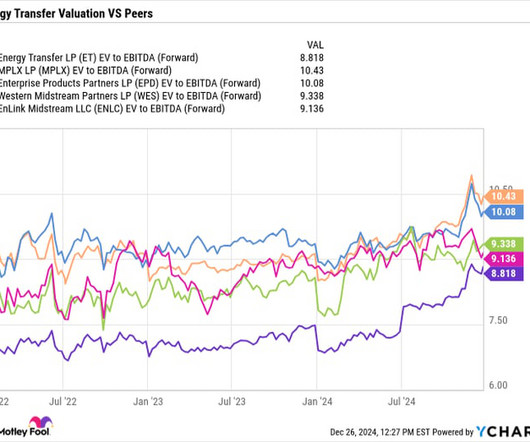

Despite Energy Transfer's strong position to benefit from the increasing power needs associated with AI, it is one of the cheapest MLP midstream stocks, trading at a forward enterprisevalue (EV)- to- EBITDA ratio of 8.8 The EV-to-EBITDA ratio is one of the most common ways to value pipeline stocks given their debt and growth capex.

An early mover in the direct banking market SoFi, which is short for Social Finance, was founded in 2011. SoFi has also been finding fresh ways to gain new customers without taking on more debt. At $16, it has an enterprisevalue of $16.2 Should investors buy SoFi today and expect it to hit those Street-high estimates?

As such, midstream companies typically carry debt to fund these projects. Enterprise currently carries leverage (net debt adjusted for equity credit in junior subordinated notes/EBITDA) of around 3.1 That's low for a midstream company, and as such its debt carries an investment grade.

Enterprise Products Partners had a distribution coverage ratio of 1.8 It defines that metric as net debt adjusted for equity credit in junior subordinated notes [hybrids] divided by adjusted EBITDA.) An attractive valuation Enterprise Products Partners trades at a forward enterprisevalue -to-EBITDA (EV/EBITDA) multiple of 9.8

due to the strong cash-flow nature of the industry, while Enterprise has a conservative target range between 2.75x and 3.25x. Note that Enterprise defines leverage as its net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ).

An attractive value Despite its strong performance and burgeoning growth opportunities, Energy Transfer continues to trade at both a relative and a historical discount. Enterprise trades at an EV/EBITDA multiple of 8.5 between 2011 and 2016. based on 2025 analyst estimates, which is toward the low end of valuations in the group.

They have $3 billion of cash on the balance sheet and no debt. If somebody else is buying them out, technically, the enterprisevalue, the actual amount being exchanged, is not 10 billion because you're buying a company with three billion just sitting in the bank. It has a lot of debt.

Midstream companies are typically valued using an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) metric. The reason for this is that these are capital-intensive businesses, and, as such, the companies carry debt in order to build out their pipeline systems.

Inexpensive stocks Companies organized as master limited partnerships , like Enterprise and Energy Transfer, currently trade at historically attractive valuations, well below the average 13.7 times enterprisevalue -to-EBITDA (EV/EBITDA) multiple the group traded at between 2011 and 2016.

To do this, I mined data on the stocks' average enterprise-value-to-sales ratio from my favorite financial data provider, S&P Global Market Intelligence. Huntington Ingalls data begins in 2011, the year when Northrop Grumman spun off Huntington Ingalls as a separate company. General Dynamics (NYSE: GD) 1.04

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content