This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By and large, this structure has been eliminated, and MLPs are generally in better financial shape as a result, carrying less leverage and being able to grow their business through free cash flow. Between 2011 and 2016, MLPs traded at an average multiple of 13.7

The sector has gone through a transformation in the past decade, with midstream companies reducing leverage and being more disciplined when it comes to funding growth projects. multiple that midstream MLPs traded at between 2011 and 2016. All three stocks trade well below the MLP average multiple from that 2011-to-2016 period.

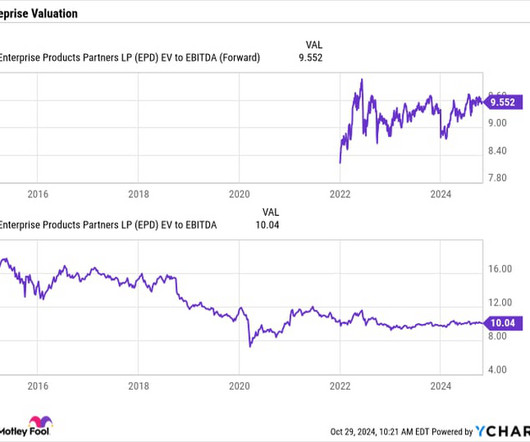

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprise value (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6

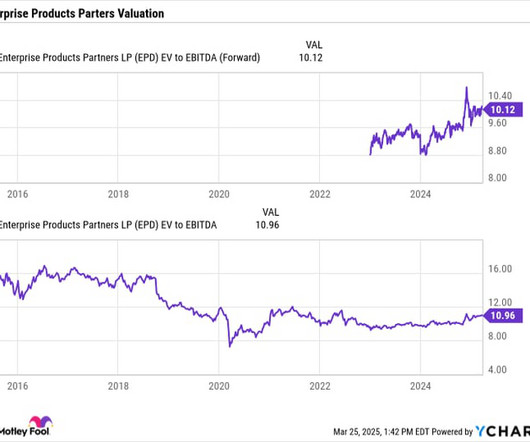

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprise value (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, climbed 10% to nearly $2.4 It ended the quarter with leverage of 3 times. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

The company's balance sheet is currently in good shape, with leverage (as used by rating agencies) toward the low end of its 4x to 4.5x EBITDA, meanwhile, excludes non-cash depreciation expenses that would otherwise be included with earnings. times average EV/EBITDA multiple between 2011 and 2016. target range.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) also rose 5% to nearly $2.44 It ended the quarter with leverage of 3x, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. It produced distributable cash flow (DCF) of $1.96

Meanwhile, it has historically been conservative with its leverage, distribution coverage ratio, and growth capital expenditure (capex) spending. on average, between 2011 and 2016. Enterprise's consistency stems from its largely fee-based model, where the company only takes on minimal commodity or spread risk.

The company has also leveraged the strength of core businesses like e-commerce to add on higher-margin businesses like advertising, consumer financing, its third-party marketplace, and digital payments. That bodes well for Remitly, which was founded in 2011 but has grown rapidly. In its most recent quarter, revenue rose 43% to $241.6

Understanding SoFi's business SoFi, which is short for Social Finance, was founded at Stanford University in 2011. Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) turned positive in 2021 and increased at a CAGR of 279%, from $30 million to $432 million. Image source: Getty Images.

We drove strong wholesale GPU despite experiencing steep depreciation, and we stabilized CAF's net interest margins while we maintained penetration. We achieved this despite experiencing steep depreciation that was concentrated primarily in June and July. SG&A as a percent of gross profit was 84%, a leverage of 6.3

This figure excludes $156 million of depreciation. I would like to highlight that this represents the 14th consecutive increase in annual dividends, since we initiated dividends in fiscal 2011. Q4 operating income was $8.8 billion and was up 53% from a year ago, with operating margin at 63% of revenue. Adjusted EBITDA was $9.1

It's also nicely improved its balance sheet over the past few years so that its leverage is now in the lower half of its targeted 4 times to 4.5 Meanwhile, it plans to buy back stock once its leverage target is achieved. times range. It is looking to grow its distribution by 3% to 5% a year moving forward. Image source: Getty Images.

An early mover in the direct banking market SoFi, which is short for Social Finance, was founded in 2011. Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) turned positive in 2021 at $30 million, and that figure grew at a CAGR of 279% to $432 million in 2023.

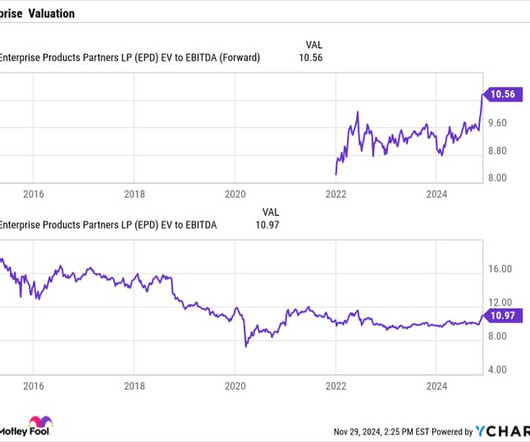

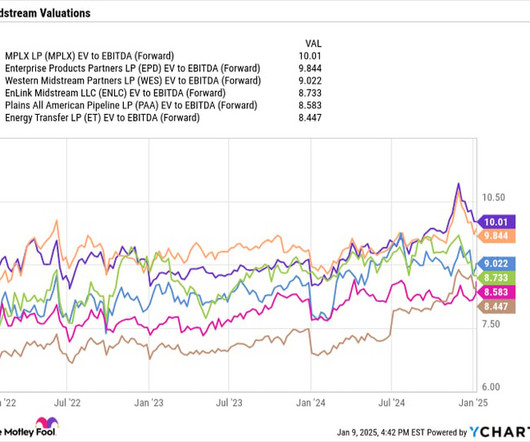

Energy Transfer trades at an enterprise value (EV) -to-earnings before interest, taxes, depreciation, and amortization ( EBITDA) multiple of 8.1 times EV/EBITDA multiple that midstream MLPs traded at between 2011 to 2016 when they had worse balance sheets and narrower distribution coverage ratios. times, while Enterprise trades at 9.8,

In addition, the company has a solid balance sheet with low leverage for the industry. Meanwhile, it ended the quarter with leverage of 3 times. Midstream companies typically carry leverage from 3x to 4.5x Midstream companies typically carry leverage from 3x to 4.5x

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, increased by 4% to nearly $2.6 It ended 2024 with a leverage ratio of 3.1 (It This is generally considered a low leverage ratio for the midstream industry, where levels between 3.5 billion, a 5% increase. are common.

Given that most of these projects won't be complete until later 2025 or 2026, the increased capex should have a larger impact on the growth of earnings before interest, taxes, depreciation, and amortization (EBITDA) in 2026 and 2027. between 2011 and 2016. Image source: Getty Images. However, it will be very tight.

This gives the company solid visibility into future cash flows and EBITDA (earnings before interest, taxes, depreciation, and amortization), the two metrics by which midstream companies are most commonly evaluated. Enterprise currently carries leverage (net debt adjusted for equity credit in junior subordinated notes/EBITDA) of around 3.1

In addition to these growth opportunities in front of it, Energy Transfer is cheap compared to its peers and from a historical level, trading at an enterprise value (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just 8.4 times between 2011 and 2016. billion.

During 2024, we also paid down 250 million in debt and reduced our total leverage ratio to 3.2 After my unsuccessful attempt in 2011, we succeeded in bringing Stephan aboard as chief strategy officer in 2023. Credit agreement EBITDA for the fourth quarter was $164 million, and we further reduced our total leverage ratio to 3.2

Learn More Midstream companies, meanwhile, now operate with lower leverage and have more robust coverage for their distributions. times that midstream master limited partnerships (MLPs) averaged between 2011 and 2016. Western Midstream's balance sheet is in stellar shape, with leverage below 3x, and it generated $1.3

The positive 160-basis-point change in profitability was primarily due to net sales leverage, product mix, and productivity improvements. We continue to target a gross debt to EBITDA leverage ratio in the range of one to two times. When expressed as a percentage of net sales, earnings for the segment were 16.5%, up from 14.9%.

Phil has been a strong leader for our modular business since 2011, and he led our TRS business prior to that. Rental equipment depreciation expense of $85 million to $89 million, direct cost of rental operations of $119 million to $123 million. Leverage is 1.68 His experience makes him ideal for the role. We're very comfortable.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content