This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Between 2011 and 2016, MLPs traded at an average multiple of 13.7 in enterprise-value- to- EBITDA (earnings before interest, taxes, depreciation, and amortization), the most common way to value these stocks. The company has also always taken a more conservative approach with leverage and maintained a strong balance sheet.

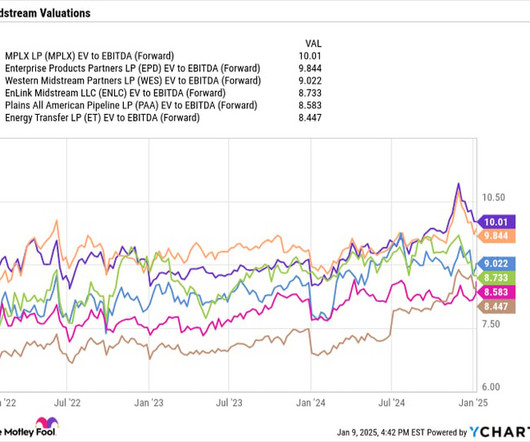

Cheap stocks Energy Transfer, Enterprise Products Partners, and Williams all have strong growth ahead from increasing natural gas demand. Midstream master limited partnerships (MLPs) traded at an average enterprisevalue to EBITDA multiple of 13.7 between 2011 and 2016. Data by YCharts.

.” Through Incline’s family of funds, the firm invests in middle-market businesses operating in the services, value-added distribution, and specialized light manufacturing sectors, targeting companies with enterprisevalues ranging from $25 million to $750 million.

Here's how the numbers break down: Average EnterpriseValue-to-Sales Ratio (EV/S) From: 2004-2013 2014-2023 2003-2023 Boeing 0.9 Here's how the numbers break down: Average EnterpriseValue-to-Sales Ratio (EV/S) From: 2004-2013 2014-2023 2003-2023 Boeing 0.9 General Dynamics 1.0 Huntington Ingalls 0.5* Lockheed Martin 0.8

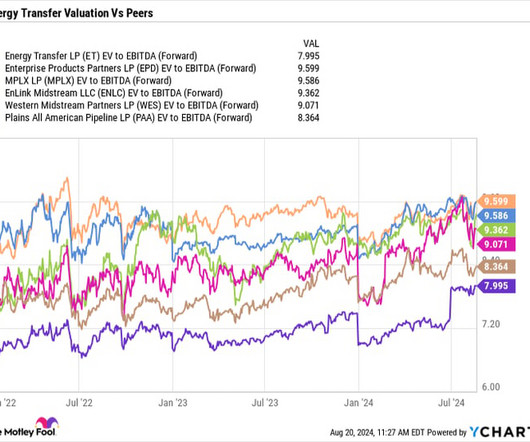

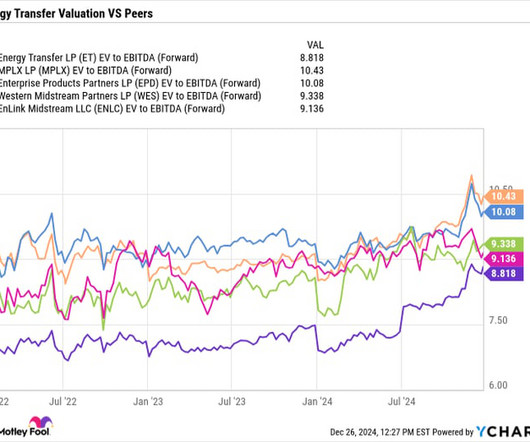

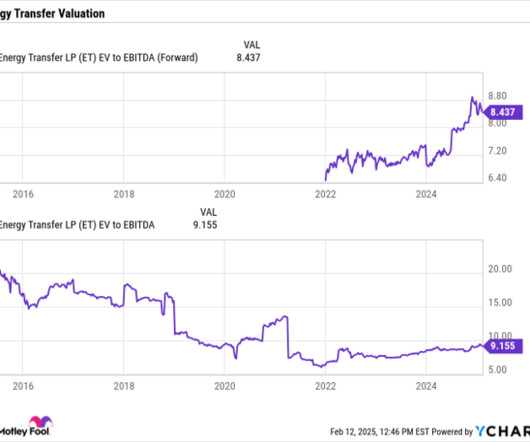

Multiple expansion opportunities From a valuation perspective, Energy Transfer is the cheapest stock among its master limited partnership (MLP) midstream peers, trading at 8x on a forward enterprisevalue -to-adjusted EBITDA basis. EV/EBITDA multiple between 2011 and 2016, so the industry as a whole has seen its multiple come down.

At the same time, Energy Transfer continues to trade at a forward enterprise-value -to- EBITDA multiple of 8 times based on 2025 estimates, which is well below historical levels, not to mention one of the lowest valuations in the MLP space. times EV/EBITDA average multiple between 2011 and 2016.

< Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6 times (one of the most common ways to value midstream stocks) is attractive and well below the 13.7

Chevron's capital discipline shone through in 2022, when its return on capital employed (ROCE) hit 20%, a level last seen in 2011. Right now, Chevron is trading significantly below its five-year averages on two key valuation counts -- price-to-cash flow and enterprisevalue-to- EBITDA. billion, including debt.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5

Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. The first is that enterprisevalue takes into consideration the amount of net debt a company carries on its balance sheet. times average EV/EBITDA multiple between 2011 and 2016.

.” Incline Equity invests in North America-based companies with enterprisevalues of $25 million to $750 million. Sectors of interest include services, value-added distribution, and specialized light manufacturing. In October 2023, Incline closed its sixth fund, Incline Equity Partners VI LP , with $1.9 billion of capital.

Buffett has been in this position in the past, most notably during the financial crisis when he prudently invested $5 billion in preferred stock issued by Bank of America in 2011 and converted those warrants in 2017 for a $15 billion profit. Is Berkshire Hathaway stock a buy, hold, or sell?

Charterhouse Capital Partners (Charterhouse), a private equity firm focused on investments in mid-market European companies in the services and healthcare sectors with an enterprisevalue of between €150m and €1bn, has invested in sports marketing company Two Circles.

At its peak, Zoom's enterprisevalue reached $160 billion -- or 60 times the revenue it would generate in fiscal 2021. That's why Zoom now trades at about $68 with an enterprisevalue of $14 billion, or just three times the $4.5 When Cisco rejected that idea, Yuan left and founded Zoom in 2011.

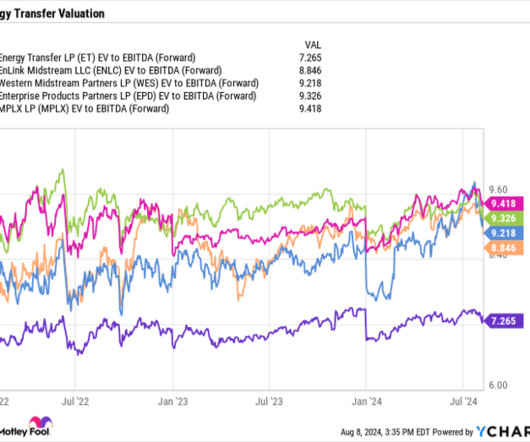

An attractively valued stock Energy Transfer trades at an attractive forward enterprisevalue (EV) -to-EBITDA multiple of just 7.3x. EV/EBITDA multiple the stocks averaged between 2011 and 2016. It has paid $2.3 billion in distributions thus far this year and should pay around $4.7 billion total for the year.

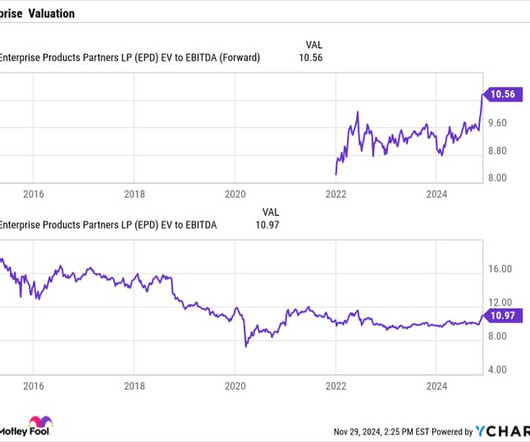

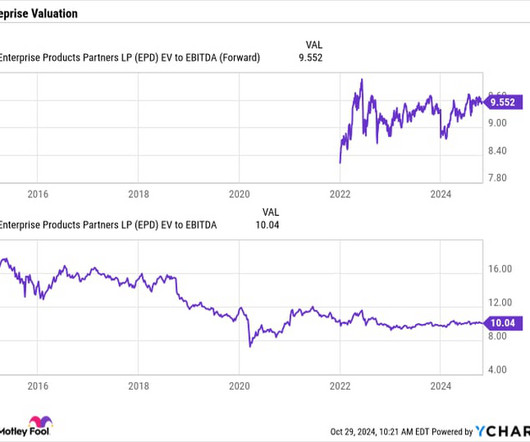

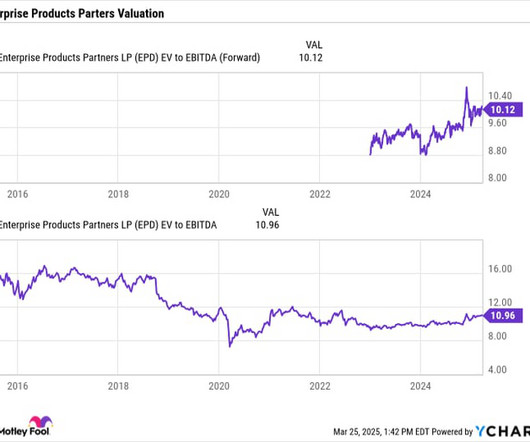

Attractive valuation Despite its strong performance this year, Enterprise's stock still trades at an attractive valuation from a historical perspective. Its enterprise-value -to-EBITDA (EV/EBITDA) multiple stands at 10.5, Before the pandemic, Enterprise would often carry an EV/EBITDA multiple of 15 or more.

The company trades at a forward- enterprisevalue -to-adjusted - EBITDA (EV/EBITDA) multiple of about 9.5. plus multiple between 2011 and 2016 when the companies were generally in worse financial shape. It has one of the most attractive integrated systems in the U.S.

Enterprise Products has an attractive valuation Despite its strong balance sheet and growth opportunities in front of it, Enterprise Products trades a very attractive valuation on an enterprisevalue to forward earnings before interest, taxes, depreciation, and amortization basis (EV/EBITDA) of 9.2

Attractive valuation Besides having some of the best growth opportunities in the pipeline space, Energy Transfer is also one of the most attractively valued MLPs. Enterprisevalue (EV) to EBITDA is typically the preferred metric investors use when valuing midstream companies. Image source: Getty Images.

After the current period of outsized spending on growth projects, Enterprise does expect to settle back into a lower range thereafter. An attractive valuation One of the most common ways investors value midstream companies is by using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. times EV/EBITDA multiple.

Inexpensive valuation Despite its high yield and growth opportunities, Enterprise is still trading at an inexpensive valuation of a 9.3 forward enterprisevalue (EV) -to- EBITDA multiple. This is one of the most common ways to value midstream stocks, as it takes into account their net debt while taking out non-cash expenses.

Inexpensive valuation Despite its high yield and growth opportunities, Enterprise is still trading at an inexpensive valuation of a 9.3 forward enterprisevalue (EV) -to- EBITDA multiple. This is one of the most common ways to value midstream stocks, as it takes into account their net debt while taking out non-cash expenses.

times average enterprisevalue (EV) -to- EBITDA multiple between 2011 and 2016, while today most midstream stocks trade at under a 10 times multiple. EV/EBITDA tends to be the most used metric to value midstream companies, as it takes into consideration their debt positions and takes out non-cash expenses.

Between 1999 and 2011, the small-cap Russell 2000 index outperformed the S&P 500 index by a whopping 6.5 Moreover, enterprisevalue is a better way to measure the total worth of the company than market cap, because it accounts for debt. How did small-caps do after the burst of the internet bubble?

While we believe there is tremendous value in the intellectual property, data, and experience we've amassed from the LTC business, our view of Genworth's enterprisevalue and future potential are rooted in our 81.6% Choice 2 is one of our newer blocks with policies written between 2003 and 2011. life companies.

Since 2011, KKR portfolio companies have awarded billions of dollars in equity to over 100,000 non-senior management employees across more than 40 portfolio companies. This strategy is based on the belief that employee engagement is a key driver in building stronger companies. For more information, visit www.jmi.com.

However, the US investor has been involved in the Costa Group journey for much longer than that, having been a majority owner of the company prior to its 2015 initial public offering (IPO) on the ASX with its first equity stake acquired in 2011, back when its name was Paine + Partners. per share 1.

Our absolute emissions are over 10% lower than the 2011 peak, and that's despite capacity growth of 30% since then. This deep commitment has not only resulted in industry-leading fuel efficiency, it has also resulted in lower absolute GHG emissions. Last year, we also exceeded our industry-leading shore power capability goal.

Acacia makes control and minority investments in family-owned and/or owner-operated companies that have enterprisevalues from $50 million to $300 million and EBITDA of more than $5 million. The firm was founded in 2011 by Partner Brad Johl and is headquartered in Austin, Texas.

Despite Energy Transfer's strong position to benefit from the increasing power needs associated with AI, it is one of the cheapest MLP midstream stocks, trading at a forward enterprisevalue (EV)- to- EBITDA ratio of 8.8 The EV-to-EBITDA ratio is one of the most common ways to value pipeline stocks given their debt and growth capex.

Enterprisevalue (EV) -to- EBITDA is typically the most common way to value pipeline stocks, as EV takes into account net debt used to build out the asset base, while EBITDA removes the non-cash depreciation costs of those assets since the project costs are already captured in the net debt.

An early mover in the direct banking market SoFi, which is short for Social Finance, was founded in 2011. At $16, it has an enterprisevalue of $16.2 billion -- which values it at 5 times next year's sales and 18 times its adjusted EBITDA. Should investors buy SoFi today and expect it to hit those Street-high estimates?

From a valuation perspective, the stock trades at an enterprisevalue (EV) -to-EBITDA multiple of about 8.5 times between 2011 and 2016. times the high end of its 2025 guidance. While its valuation has risen, it's still well below where it traded before the pandemic. Meanwhile, midstream MLPs traded at an average multiple of 13.7

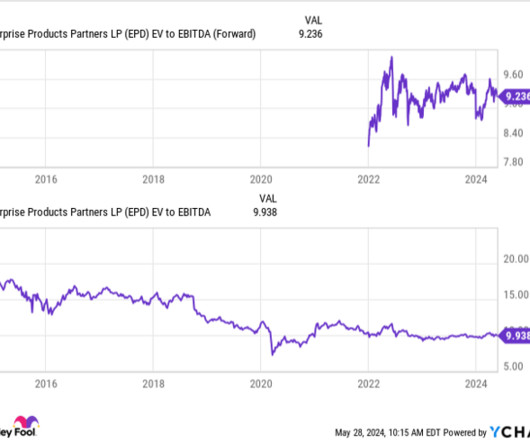

An attractive valuation Enterprise Products Partners trades at a forward enterprisevalue -to-EBITDA (EV/EBITDA) multiple of 9.8 EV/EBITDA is the most common metric used to value midstream companies because they spend a lot of money on building long-lived assets such as pipelines. based on analysts' 2025 estimates.

An attractive valuation In addition to its consistent track record and the emerging opportunities in front of it from a more favorable midstream and energy environment, Enterprise's stock is also attractively valued from a historical perspective. times EV/EBITDA multiple on average that midstream MLPs traded at between 2011 and 2016.

An attractive value Despite its strong performance and burgeoning growth opportunities, Energy Transfer continues to trade at both a relative and a historical discount. between 2011 and 2016. Meanwhile, the midstream MLP group as a whole traded at an average EV/EBITDA multiple of 13.7

The most common way to value midstream companies is using an enterprise-value-(EV)- to-EBITDA multiple, which takes into account its debt while removing the noncash costs associated with depreciation , since these costs have already been captured in its debt.

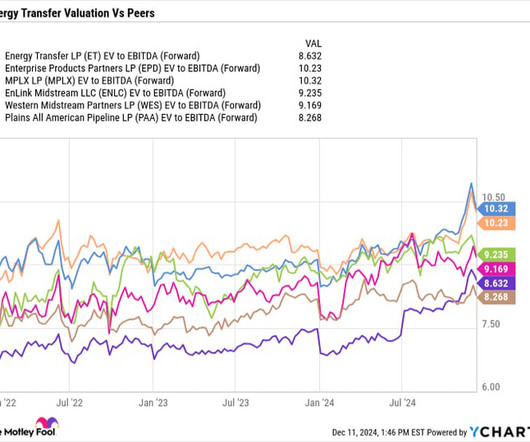

In addition to these growth opportunities in front of it, Energy Transfer is cheap compared to its peers and from a historical level, trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just 8.4 times between 2011 and 2016.

If somebody else is buying them out, technically, the enterprisevalue, the actual amount being exchanged, is not 10 billion because you're buying a company with three billion just sitting in the bank. The enterprisevalue, you subtract the cash from the market cap to get the enterprisevalue, which would be $7 billion.

Meanwhile, the stock trades at an attractive enterprisevalue (EV) -to-EBITDA multiple of just 8.3 multiple that midstream MLPs traded at between 2011 and 2016. While that has risen recently, the multiple is well below where Energy Transfer traded at before the COVID-19 pandemic, and well below the average 13.7

At the same time, it also has one of the cheapest stocks in the space, with it trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just over 8 times. times that midstream master limited partnerships (MLPs) averaged between 2011 and 2016.

The total enterprisevalue of the transaction totalled 1.53 Ontario Teachers has been an investor in CPH since 2011, when it acquired a joint control stake in the airports. The Public Sector Pension Investment Boards wholly owned subsidiary AviAlliance has completed its acquisition of AGS Airports, the operator of U.K.-based

Midstream companies are typically valued using an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) metric. times EV/EBITDA multiple between 2011 and 2016. Lake Charles would allow Energy Transfer a new outlet into international markets. Image source: Getty Images.

For this reason, it might be surprising to suggest that companies that were only founded in 2011 and 2012 could be worth more than Pepsi and Starbucks within five years. Consider that Coinbase's enterprisevalue is roughly 30 times its EBITDA right now, which is a reasonable valuation.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content