This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By and large, this structure has been eliminated, and MLPs are generally in better financial shape as a result, carrying less leverage and being able to grow their business through free cash flow. Between 2011 and 2016, MLPs traded at an average multiple of 13.7

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6

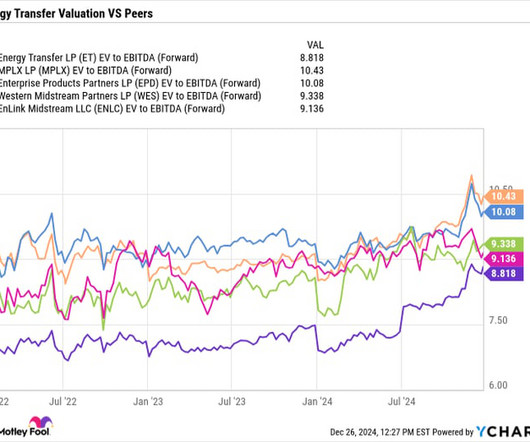

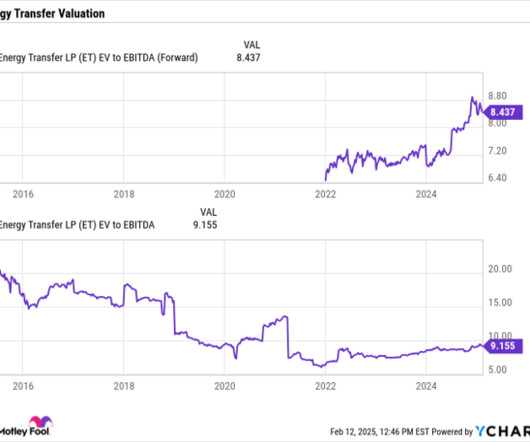

At the same time, Energy Transfer continues to trade at a forward enterprise-value -to- EBITDA multiple of 8 times based on 2025 estimates, which is well below historical levels, not to mention one of the lowest valuations in the MLP space. times EV/EBITDA average multiple between 2011 and 2016.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower.

The company's balance sheet is currently in good shape, with leverage (as used by rating agencies) toward the low end of its 4x to 4.5x Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. times average EV/EBITDA multiple between 2011 and 2016. target range.

The company generates a lot of cash flow, and has historically taken a conservative posture with leverage , which is also why it has been able to consistently increase its distribution. Leverage currently stand at 3, which is low for the midstream industry. Enterprise currently has a robust forward yield of 7.2%

The company generates a lot of cash flow, and has historically taken a conservative posture with leverage , which is also why it has been able to consistently increase its distribution. Leverage currently stand at 3, which is low for the midstream industry. Enterprise currently has a robust forward yield of 7.2%

It ended the quarter with leverage of 3 times. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. This leverage is considered low in the midstream space given the strong cash flow these companies generate. The stock now has a forward yield of about 7.2%

times average enterprisevalue (EV) -to- EBITDA multiple between 2011 and 2016, while today most midstream stocks trade at under a 10 times multiple. EV/EBITDA tends to be the most used metric to value midstream companies, as it takes into consideration their debt positions and takes out non-cash expenses.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

Enterprise's consistency stems from its largely fee-based model, where the company only takes on minimal commodity or spread risk. Meanwhile, it has historically been conservative with its leverage, distribution coverage ratio, and growth capital expenditure (capex) spending. on average, between 2011 and 2016.

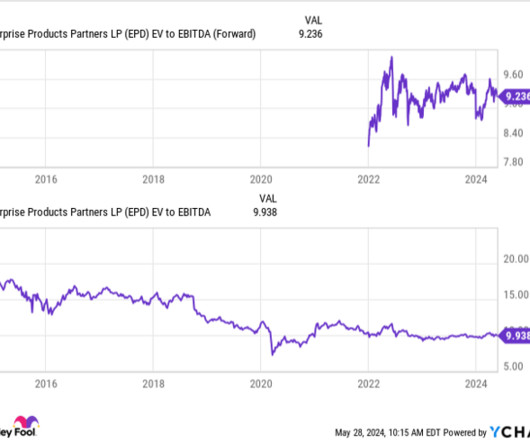

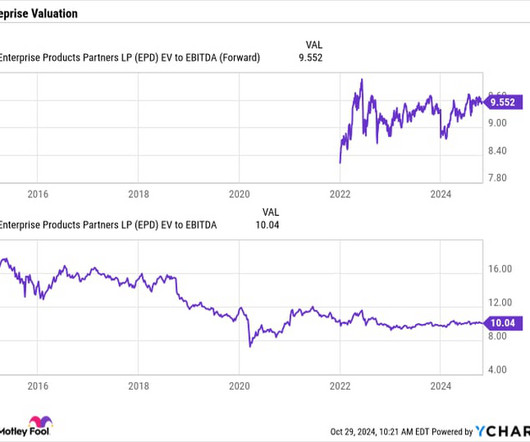

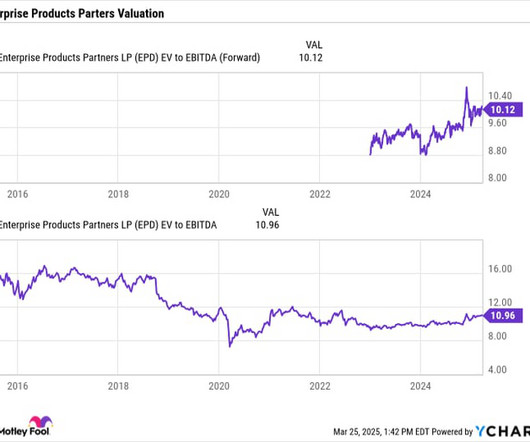

Based on its DCF, Enterprise's distribution coverage ratio was 1.7x. It ended the quarter with leverage of 3x, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. On that front, Enterprise trades at a forward EV/EBITDA multiple of 9.5

We continue to leverage Genworth's substantial LTC expertise to develop innovative aging care services and solutions and a new CareScout services business. They operate as a closed system, leveraging existing reserves and capital, earn premiums, as well as future new premiums, under the LTC multiyear rate action plan to cover liabilities.

Agiloft is a leading provider of data-first CLM software, enabling legal, procurement, sales and other departments to streamline and leverage their contracting efforts. Since 2011, KKR portfolio companies have awarded billions of dollars in equity to over 100,000 non-senior management employees across more than 40 portfolio companies.

All of this leaves us firmly placed on our path back to achieve investment-grade leverage metrics by 2026. It's the biggest example yet of how we leverage our scale and will be doubling down when we bring over her sister ship, Carnival Firenze in 2024. And we welcomed Seabourn Pursuit, our second expedition ship.

However, the US investor has been involved in the Costa Group journey for much longer than that, having been a majority owner of the company prior to its 2015 initial public offering (IPO) on the ASX with its first equity stake acquired in 2011, back when its name was Paine + Partners. per share 1.

It's also nicely improved its balance sheet over the past few years so that its leverage is now in the lower half of its targeted 4 times to 4.5 Meanwhile, it plans to buy back stock once its leverage target is achieved. times range. It is looking to grow its distribution by 3% to 5% a year moving forward. Image source: Getty Images.

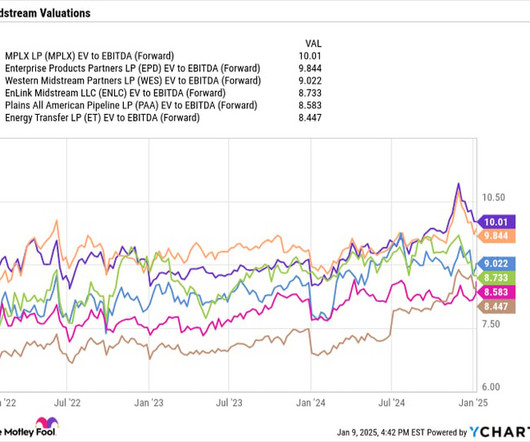

Despite Energy Transfer's strong position to benefit from the increasing power needs associated with AI, it is one of the cheapest MLP midstream stocks, trading at a forward enterprisevalue (EV)- to- EBITDA ratio of 8.8 The EV-to-EBITDA ratio is one of the most common ways to value pipeline stocks given their debt and growth capex.

An early mover in the direct banking market SoFi, which is short for Social Finance, was founded in 2011. That deal could enable SoFi to generate more fee-based revenue without increasing its leverage. At $16, it has an enterprisevalue of $16.2 Should investors buy SoFi's stock right now? respectively.

With its balance sheet and leverage in good shape, it appears well positioned to tackle this growth opportunity. From a valuation perspective, the stock trades at an enterprisevalue (EV) -to-EBITDA multiple of about 8.5 times between 2011 and 2016. billion in distributions with its DCF given its projected EBITDA growth.

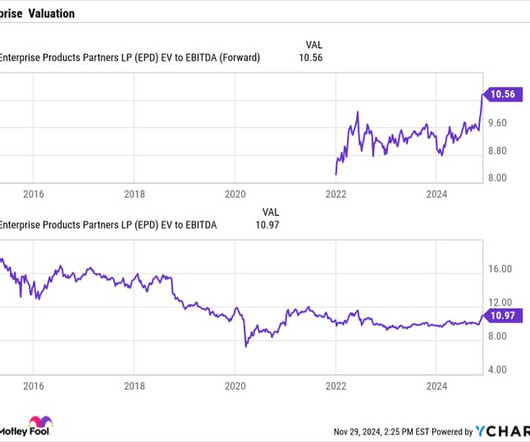

Enterprise Products Partners had a distribution coverage ratio of 1.8 It ended 2024 with a leverage ratio of 3.1 (It This is generally considered a low leverage ratio for the midstream industry, where levels between 3.5 that the average midstream master limited partnership (MLP) traded at between 2011 and 2016.

In addition, the company has a solid balance sheet with low leverage for the industry. Enterprise's distribution coverage ratio came in at a robust 1.7 Meanwhile, it ended the quarter with leverage of 3 times. Midstream companies typically carry leverage from 3x to 4.5x

Enterprise currently carries leverage (net debt adjusted for equity credit in junior subordinated notes/EBITDA) of around 3.1 It currently trades at an enterprisevalue (EV) -to-EBITDA multiple of 10, which is the most common metric used to value midstream companies.

That said, the company has really improved its balance sheet and leverage over the past few years, so it is in good shape to pursue these additional opportunities. An attractive value Despite its strong performance and burgeoning growth opportunities, Energy Transfer continues to trade at both a relative and a historical discount.

In addition to these growth opportunities in front of it, Energy Transfer is cheap compared to its peers and from a historical level, trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just 8.4 times between 2011 and 2016. billion.

Learn More Midstream companies, meanwhile, now operate with lower leverage and have more robust coverage for their distributions. times that midstream master limited partnerships (MLPs) averaged between 2011 and 2016. Western Midstream's balance sheet is in stellar shape, with leverage below 3x, and it generated $1.3

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content