This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As a result, most pay out very generous distributions, which are similar to dividends, but much of the payout is considered a return of capital. Between 2011 and 2016, MLPs traded at an average multiple of 13.7 The 10 stocks that made the cut could produce monster returns in the coming years. billion to $4 billion in 2024.

Cheap stocks Energy Transfer, Enterprise Products Partners, and Williams all have strong growth ahead from increasing natural gas demand. Midstream master limited partnerships (MLPs) traded at an average enterprisevalue to EBITDA multiple of 13.7 between 2011 and 2016. Data by YCharts.

For example, a $100 million project with an 8x multiple would generate an average return of $12.5 Based on that type of return on growth projects, Energy Transfer should be about able to see its adjusted EBITDA rise from $15.5 EV/EBITDA multiple between 2011 and 2016, so the industry as a whole has seen its multiple come down.

Here's how the numbers break down: Average EnterpriseValue-to-Sales Ratio (EV/S) From: 2004-2013 2014-2023 2003-2023 Boeing 0.9 Here's how the numbers break down: Average EnterpriseValue-to-Sales Ratio (EV/S) From: 2004-2013 2014-2023 2003-2023 Boeing 0.9 General Dynamics 1.0 Huntington Ingalls 0.5* Lockheed Martin 0.8

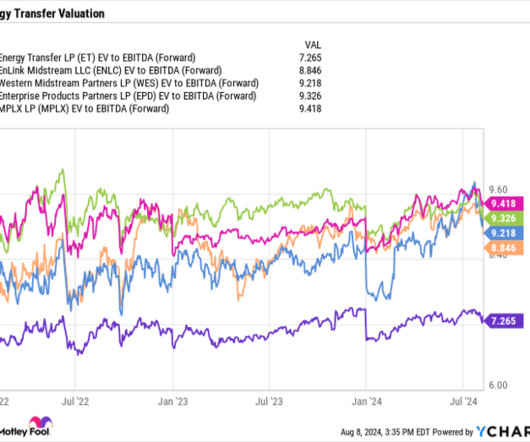

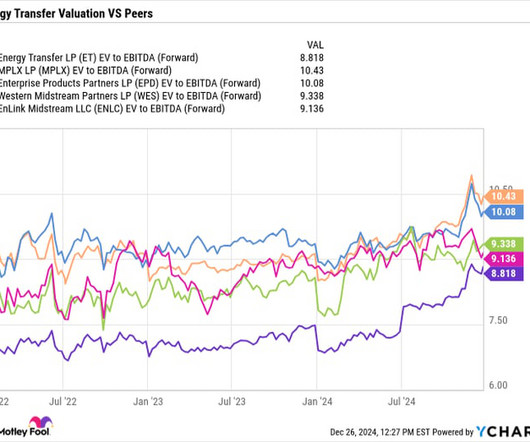

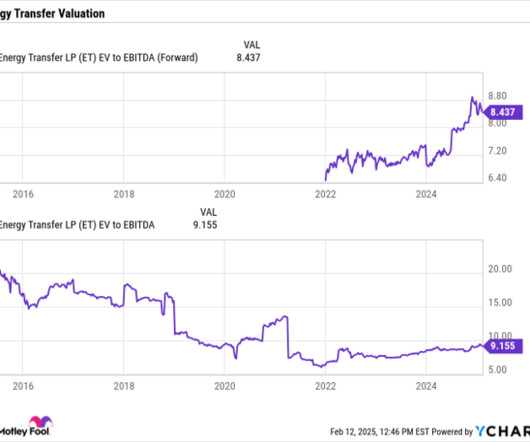

At the same time, Energy Transfer continues to trade at a forward enterprise-value -to- EBITDA multiple of 8 times based on 2025 estimates, which is well below historical levels, not to mention one of the lowest valuations in the MLP space. times EV/EBITDA average multiple between 2011 and 2016. Image source: Getty Images.

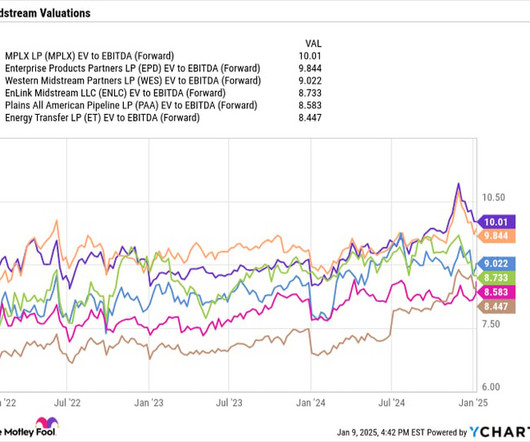

< Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6 times (one of the most common ways to value midstream stocks) is attractive and well below the 13.7

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 The 10 stocks that made the cut could produce monster returns in the coming years.

Chevron's capital discipline shone through in 2022, when its return on capital employed (ROCE) hit 20%, a level last seen in 2011. While that reveals Chevron's capital efficiency, it also means large potential returns for shareholders. Chevron's ROCE has grown at a faster clip than rivals since Wirth took over.

With interest rates likely headed lower over the next few years as the Fed embarks on a rate-cutting cycle, income-oriented investors may be looking for places to invest that can offer higher yields and attractive returns. Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple.

Charterhouse Capital Partners (Charterhouse), a private equity firm focused on investments in mid-market European companies in the services and healthcare sectors with an enterprisevalue of between €150m and €1bn, has invested in sports marketing company Two Circles.

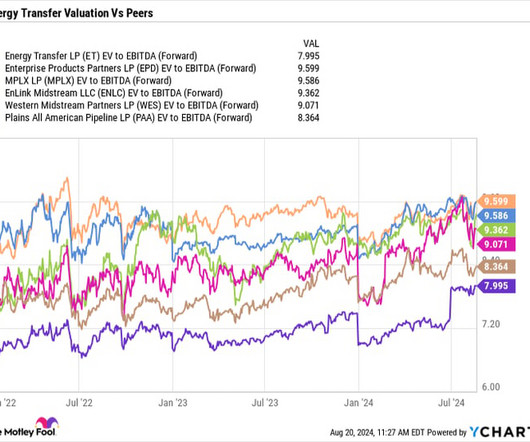

The stock has performed well this year with an over 20% return, including distributions. An attractively valued stock Energy Transfer trades at an attractive forward enterprisevalue (EV) -to-EBITDA multiple of just 7.3x. EV/EBITDA multiple the stocks averaged between 2011 and 2016. It has paid $2.3

At its peak, Zoom's enterprisevalue reached $160 billion -- or 60 times the revenue it would generate in fiscal 2021. That's why Zoom now trades at about $68 with an enterprisevalue of $14 billion, or just three times the $4.5 When Cisco rejected that idea, Yuan left and founded Zoom in 2011.

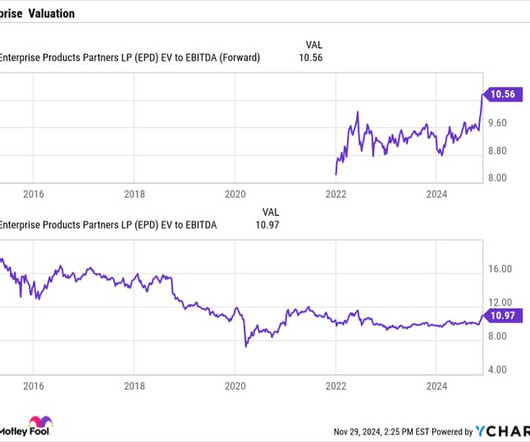

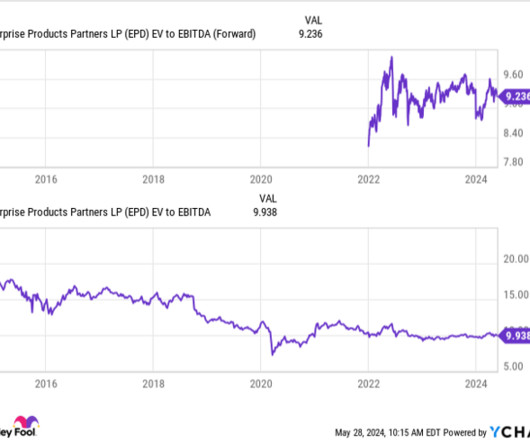

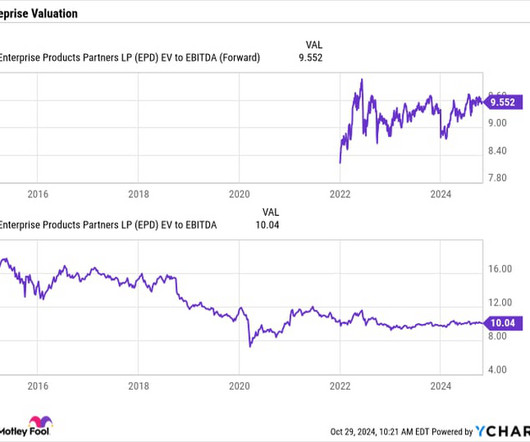

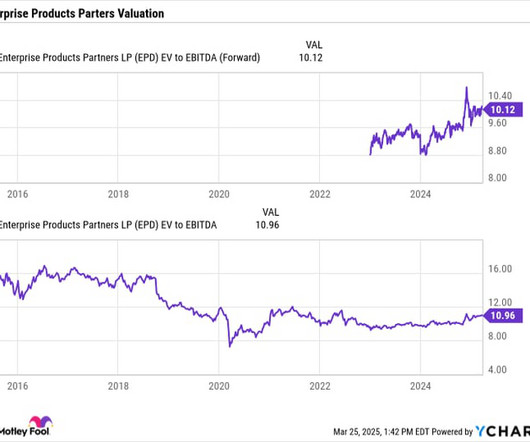

Since 2018, Enterprise has averaged an approximately 13% return on invested capital (ROIC) on its growth projects. Attractive valuation Despite its strong performance this year, Enterprise's stock still trades at an attractive valuation from a historical perspective. on average, between 2011 and 2016. It currently has $6.9

Over the past five years, Enterprise has averaged about a 13% return on invested capital, so these growth projects should provide meaningful growth to the company in the years ahead. At a similar return, the approximately $10.5 plus multiple between 2011 and 2016 when the companies were generally in worse financial shape.

Enterprise Products has growth opportunities After reducing its growth capex during the early stages of the pandemic, Enterprise is beginning to ramp it back up. That's good news for investors, as the company consistently generated a return of about 13% on its growth projects over the past six years.

The company typically has gotten a 13% return on invested capital over the past several years. Inexpensive valuation Despite its high yield and growth opportunities, Enterprise is still trading at an inexpensive valuation of a 9.3 forward enterprisevalue (EV) -to- EBITDA multiple. It's also well below the 13.7

The company typically has gotten a 13% return on invested capital over the past several years. Inexpensive valuation Despite its high yield and growth opportunities, Enterprise is still trading at an inexpensive valuation of a 9.3 forward enterprisevalue (EV) -to- EBITDA multiple. It's also well below the 13.7

Enterprise currently has $6.9 It noted that it has produced about a 12% return on invested capital over the past decade. After the current period of outsized spending on growth projects, Enterprise does expect to settle back into a lower range thereafter. On that front, Enterprise trades at a forward EV/EBITDA multiple of 9.5

times average enterprisevalue (EV) -to- EBITDA multiple between 2011 and 2016, while today most midstream stocks trade at under a 10 times multiple. EV/EBITDA tends to be the most used metric to value midstream companies, as it takes into consideration their debt positions and takes out non-cash expenses.

The stock has had a strong 2024 with a total return, including distributions, of about 50% as of this writing. Attractive valuation Besides having some of the best growth opportunities in the pipeline space, Energy Transfer is also one of the most attractively valued MLPs. Image source: Getty Images.

In fact, this analyst sees a potential 50% return for small caps in 2024, as the market rally broadens out and dirt cheap small caps "catch-up" in valuation to large caps as the economy improves. Between 1999 and 2011, the small-cap Russell 2000 index outperformed the S&P 500 index by a whopping 6.5 While the IJR's 15.9%

See the 10 stocks *Stock Advisor returns as of August 1, 2023 life insurance business; and Kelly Saltzgaber, chief investment officer, will also be available to take your questions. Free cash flow to the holding company remained strong, driven by Enact's return of capital and tax payments in 2023 from Enact and the U.S. life companies.

Since 2011, KKR portfolio companies have awarded billions of dollars in equity to over 100,000 non-senior management employees across more than 40 portfolio companies. This strategy is based on the belief that employee engagement is a key driver in building stronger companies. For more information, visit www.jmi.com.

The 10 stocks that made the cut could produce monster returns in the coming years. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*. Our absolute emissions are over 10% lower than the 2011 peak, and that's despite capacity growth of 30% since then. In 2023, we captured over 3.5

However, the US investor has been involved in the Costa Group journey for much longer than that, having been a majority owner of the company prior to its 2015 initial public offering (IPO) on the ASX with its first equity stake acquired in 2011, back when its name was Paine + Partners. per share 1. For more information, visit BCI.ca

Learn More A history of outperformance Since taking the helm of Berkshire Hathaway in 1965, Warren Buffett has delivered a compound annual gain of 19.9%, nearly doubling the market benchmark S&P 500 's total return of 10.4% through 2024. Is Berkshire Hathaway stock a buy, hold, or sell?

The difference between the two is tax-related, as distributions have a return of capital component that is tax-deferred. With numerous natural gas opportunities now emerging, Energy Transfer not only has a nice growth runway, but it should also be able to get very good returns on its projects given the strong demand environment.

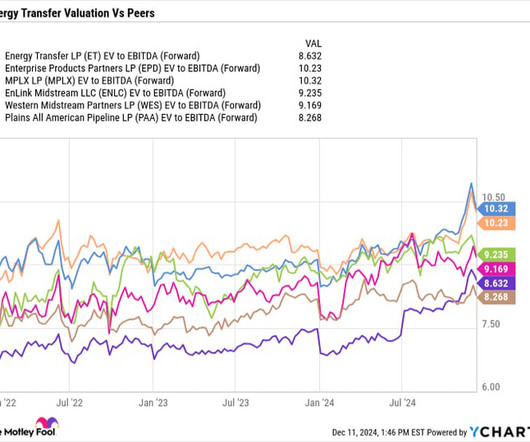

Despite Energy Transfer's strong position to benefit from the increasing power needs associated with AI, it is one of the cheapest MLP midstream stocks, trading at a forward enterprisevalue (EV)- to- EBITDA ratio of 8.8 The EV-to-EBITDA ratio is one of the most common ways to value pipeline stocks given their debt and growth capex.

That was a disappointing three-year return, but some Wall Street analysts are still bullish on the stock. An early mover in the direct banking market SoFi, which is short for Social Finance, was founded in 2011. At $16, it has an enterprisevalue of $16.2 Start Your Mornings Smarter! SoFi has a price-to-book ratio of 2.8,

There are currently a lot of attractive projects in the midstream space, with both Energy Transfer and Enterprise Products Partners among the companies announcing they are boosting their growth capex. From a valuation perspective, the stock trades at an enterprisevalue (EV) -to-EBITDA multiple of about 8.5

The company has typically gotten about a 13% annual return on its projects in recent years, so it could see about a $780 million boost to its EBITDA in 2026 as these projects ramp up. An attractive valuation Enterprise Products Partners trades at a forward enterprisevalue -to-EBITDA (EV/EBITDA) multiple of 9.8

An attractive valuation In addition to its consistent track record and the emerging opportunities in front of it from a more favorable midstream and energy environment, Enterprise's stock is also attractively valued from a historical perspective. times EV/EBITDA multiple on average that midstream MLPs traded at between 2011 and 2016.

The Alerian MLP Infrastructure Index, which tracks the sector, generated a total return of 26.7% Energy Transfer is projecting mid-teens returns on its growth projects. An attractive value Despite its strong performance and burgeoning growth opportunities, Energy Transfer continues to trade at both a relative and a historical discount.

Typically, a large percentage of distributions are treated as a return of capital. In the recent past, Enterprise has been getting about a 13% average return on its projects once they have fully ramped up. On that basis, Enterprise trades at an EV/EBITDA multiple of 10 times 2024 estimates. billion to $3.75

In addition to these growth opportunities in front of it, Energy Transfer is cheap compared to its peers and from a historical level, trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just 8.4 times between 2011 and 2016.

After all, Stock Advisors total average return is 815% a market-crushing outperformance compared to 162% for the S&P 500.* See the 10 stocks *Stock Advisor returns as of March 24, 2025 This video was recorded on March 20, 2025 David Gardner: It's that time of the month for Rule Breaker Investing.

Meanwhile, the stock trades at an attractive enterprisevalue (EV) -to-EBITDA multiple of just 8.3 multiple that midstream MLPs traded at between 2011 and 2016. See 3 “Double Down” stocks » *Stock Advisor returns as of November 11, 2024 Geoffrey Seiler has positions in Energy Transfer.

At the same time, it also has one of the cheapest stocks in the space, with it trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just over 8 times. times that midstream master limited partnerships (MLPs) averaged between 2011 and 2016.

Midstream companies are typically valued using an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) metric. times EV/EBITDA multiple between 2011 and 2016. The 10 stocks that made the cut could produce monster returns in the coming years. Image source: Getty Images.

For this reason, it might be surprising to suggest that companies that were only founded in 2011 and 2012 could be worth more than Pepsi and Starbucks within five years. Consider that Coinbase's enterprisevalue is roughly 30 times its EBITDA right now, which is a reasonable valuation.

Among the worst-hit Nasdaq stocks so far in 2025 are the " Magnificent Seven ," each of which has posted negative returns on the year. EV = enterprisevalue. The chart above illustrates Amazon's enterprisevalue to cash flow from operations (EV/CFO) over the last 20 years. AMZN EV to CFO (Annual) data by YCharts.

To do this, I mined data on the stocks' average enterprise-value-to-sales ratio from my favorite financial data provider, S&P Global Market Intelligence. Huntington Ingalls data begins in 2011, the year when Northrop Grumman spun off Huntington Ingalls as a separate company. General Dynamics (NYSE: GD) 1.04

Palantir was backed by the CIA's venture capital arm, In-Q-Tel, and it was reportedly used to track down Osama Bin Laden in 2011. Its enterprisevalue of $172.3 The 10 stocks that made the cut could produce monster returns in the coming years. government agencies and supported smarter, data-driven decisions.

Inexpensive stocks Companies organized as master limited partnerships , like Enterprise and Energy Transfer, currently trade at historically attractive valuations, well below the average 13.7 times enterprisevalue -to-EBITDA (EV/EBITDA) multiple the group traded at between 2011 and 2016.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content