This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many of these companies are structured as master limited partnerships (MLPs), which pass through their profits to their unitholders and as such don't pay corporate taxes. This portion is tax deferred until the stock is sold and reduces the owner's cost basis. This is a nice benefit, although it does add some paperwork come tax time.

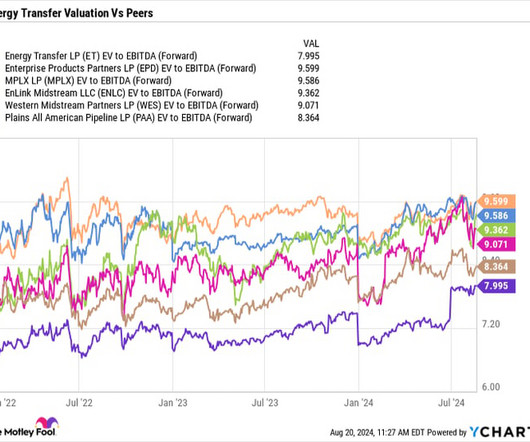

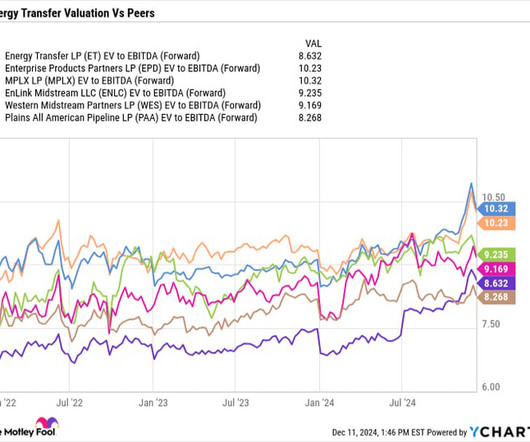

million in EBITDA (earnings before interest, taxes, depreciation, and amortization) a year. Multiple expansion opportunities From a valuation perspective, Energy Transfer is the cheapest stock among its master limited partnership (MLP) midstream peers, trading at 8x on a forward enterprisevalue -to-adjusted EBITDA basis.

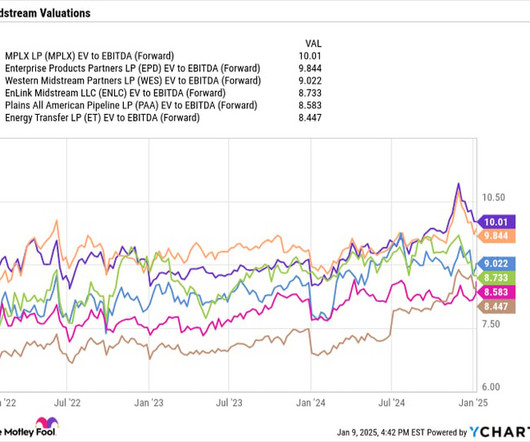

< Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6 times multiple the sector traded at between 2011 to 2016.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5

While similar, distributions include a return on capital that is untaxed until the units are typically sold, making them tax-deferred. However, investors do receive what is called a K-1 and must fill out some extra tax forms. Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple.

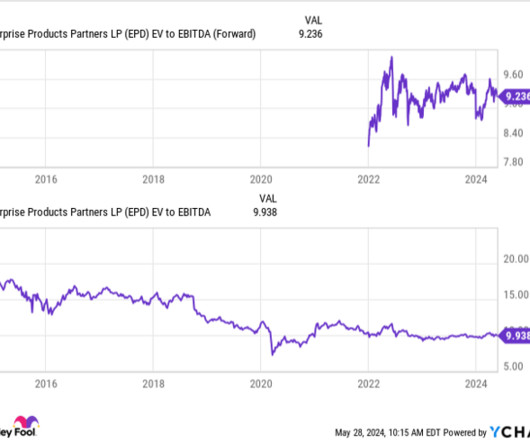

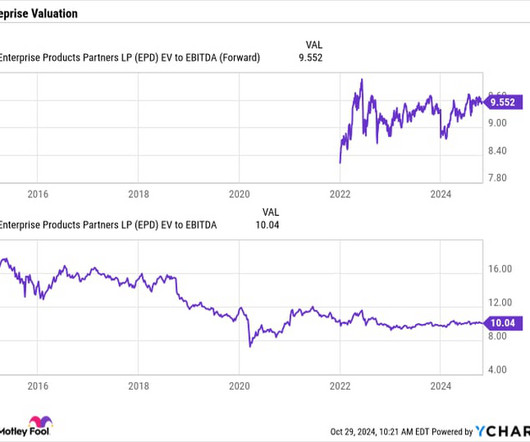

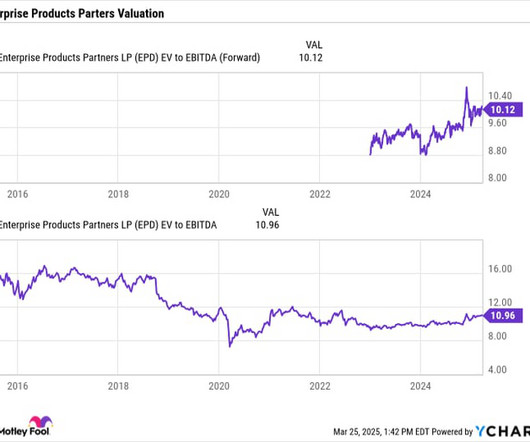

Inexpensive valuation Despite its high yield and growth opportunities, Enterprise is still trading at an inexpensive valuation of a 9.3 forward enterprisevalue (EV) -to- EBITDA multiple. This is one of the most common ways to value midstream stocks, as it takes into account their net debt while taking out non-cash expenses.

Inexpensive valuation Despite its high yield and growth opportunities, Enterprise is still trading at an inexpensive valuation of a 9.3 forward enterprisevalue (EV) -to- EBITDA multiple. This is one of the most common ways to value midstream stocks, as it takes into account their net debt while taking out non-cash expenses.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

A consistent performer The key to Enterprise's success over the years has been consistency, which has helped the pipeline company increase its distribution for 26 straight years through various ups and downs in the energy markets. For Q2, the Enterprise saw its total gross-operating margin increase nearly 11% to $2.4

These growth opportunities should lead to continued earnings before interest, taxes, depreciation, and amortization ( EBITDA ) and cash flow growth, which should also help lead to increased distributions in the coming years. Enterprisevalue (EV) to EBITDA is typically the preferred metric investors use when valuing midstream companies.

In its third quarter, Enterprise's total gross operating profit increased 5% to $2.45 Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) also rose 5% to nearly $2.44 After the current period of outsized spending on growth projects, Enterprise does expect to settle back into a lower range thereafter.

Free cash flow to the holding company remained strong, driven by Enact's return of capital and tax payments in 2023 from Enact and the U.S. Total pre-tax statutory income for the U.S. Total pre-tax statutory income for the U.S. GAAP tax rate. life insurance companies. Complete statutory results for our U.S.

The difference between the two is tax-related, as distributions have a return of capital component that is tax-deferred. While it involves a little extra paperwork come tax time, this part of the distribution reduces an investment's cost basis and is not taxed until the stock is sold, which is a nice added bonus.

An early mover in the direct banking market SoFi, which is short for Social Finance, was founded in 2011. Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) turned positive in 2021 at $30 million, and that figure grew at a CAGR of 279% to $432 million in 2023. million to 13.65 respectively.

The company is structured as a master limited partnership (MLP) , which is not taxed at the corporate level and thus passes through much of its income to investors in the form of distributions. Distributions are similar to dividends but are more favorably taxed. Where to invest $1,000 right now?

A consistent performer When it comes to its earnings reports, Enterprise Products Partners typically doesn't have too many surprises up its sleeve, as it operates a steady, fee-based midstream business. Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, increased by 4% to nearly $2.6

This gives the company solid visibility into future cash flows and EBITDA (earnings before interest, taxes, depreciation, and amortization), the two metrics by which midstream companies are most commonly evaluated. times EV/EBITDA multiple on average that midstream MLPs traded at between 2011 and 2016.

Given that most of these projects won't be complete until later 2025 or 2026, the increased capex should have a larger impact on the growth of earnings before interest, taxes, depreciation, and amortization (EBITDA) in 2026 and 2027. between 2011 and 2016. Energy Transfer is projecting mid-teens returns on its growth projects.

In addition to these growth opportunities in front of it, Energy Transfer is cheap compared to its peers and from a historical level, trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just 8.4 times between 2011 and 2016.

At the same time, it also has one of the cheapest stocks in the space, with it trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just over 8 times. times that midstream master limited partnerships (MLPs) averaged between 2011 and 2016.

Midstream companies are typically valued using an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) metric. times EV/EBITDA multiple between 2011 and 2016. Image source: Getty Images. An attractive valuation At under $20, Energy Transfer's stock is cheap.

For this reason, it might be surprising to suggest that companies that were only founded in 2011 and 2012 could be worth more than Pepsi and Starbucks within five years. Consider that Coinbase's enterprisevalue is roughly 30 times its EBITDA right now, which is a reasonable valuation. COIN EBITDA (TTM) data by YCharts.

Approximately 90% of Energy Transfer's adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) comes from fee-based businesses, while Enterprise has said that about 80% of its cash flow is fee-based. times enterprisevalue -to-EBITDA (EV/EBITDA) multiple the group traded at between 2011 and 2016.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content