This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

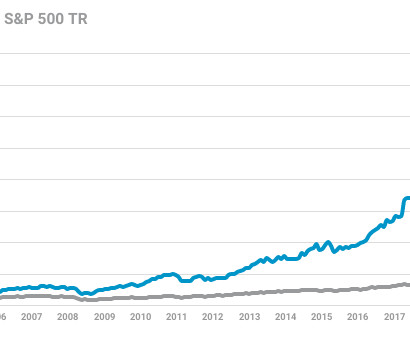

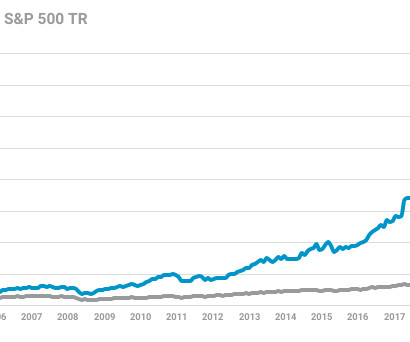

In 2013, J.P. Morgan Asset Management, a division of money-center bank JPMorgan Chase , released a study that compared the performance of publicly traded companies that initiated and grew their payouts between 1972 and 2012 to publiccompanies that didn't offer a payout over the same timeline. Every cent of its $1.01

A report issued by JPMorgan Chase 's wealth management division in 2013 found that publicly traded companies initiating and growing their payouts between 1972 and 2012 delivered an annualized return of 9.5%. annualized return for the publiccompanies that didn't offer a dividend over the same 40-year stretch. All but $0.1

Furthermore, dividend stocks have a rich history of outperforming companies that don't offer a payout. annualized return between 1972 and 2012, according to a 2013 report from the wealth management division of JPMorgan Chase , publiccompanies that initiated and grew their payouts produced an annualized return of 9.5%

Publiccompanies that pay a regular dividend are almost always time-tested, have clear long-term growth outlooks, and most importantly are profitable on a recurring basis. It's no secret that Occidental buried itself in debt when it acquired Anadarko in 2019. billion in net debt, which works out to a net-debt ratio of just 7%.

A services-driven operating model should further boost the company's operating margin, improve customer loyalty, and reduce the revenue swings observed during major iPhone replacement cycles. I'd be remiss if I didn't also mention that Apple's capital-return program is unmatched among publiccompanies.

More specifically, the company is lugging around $14.6 billion in long-term debt, compared to just $2.46 Apple's physical product innovation has led the way for more than a decade, with the company now also emphasizing high-margin subscription services. billion in cash and cash equivalents, as of the end of 2023.

Apple's capital-return program is also unmatched among publicly traded companies. The world's largest publiccompany by market cap is doling out $15 billion annually in dividend payments, and has repurchased over $600 billion of its common stock since the start of 2013. billion in net debt, as of Sept.

The second-longest yield-curve inversion on record will end The yield curve , which is a chart depicting the yields of various Treasury debt securities relative to their maturity dates, has often been a tell of what's to come for the U.S. This is to say that shorter-dated debt securities (i.e., economy and stock market.

This compares to a modest 3.95% average annual return for publiccompanies that don't offer a payout. Companies that regularly share a percentage of their earnings with their investors are almost always time-tested and able to offer transparent long-term growth outlooks. It closed out 2023 with a net debt ratio of just 7.3%.

Very few publiccompanies offer monthly dividends, and the ones that do are typically real estate investment trusts (REITs) because they are legally required to pay out 90% of their taxable earnings to shareholders. The company first issued a quarterly payment in 1998 and transitioned to a monthly distribution in 2013.

However, from the year 2000 until 2013, the business languished, and the stock dropped roughly 75% in value. Finally, the company's founder, Michael Dell, worked out a deal to take the company private again. The public history for Dell seemed to be over. At one point, Dell was valued at around $100 billion.

billion in long-term debt ($12.2 billion in net debt). Unless the company can substantially lessen its streaming losses, it's going to be difficult to silence critics. billion in dividends to its shareholders this year, and has repurchased $674 billion worth of its common stock since initiating a buyback program in 2013.

Becoming a publiccompany, while a milestone event, was not the destination but the beginning of the next chapter of our journey. Our general and administrative expense for the quarter, excluding stock-based compensation and certain nonrecurring publiccompany costs, was 20.4 Shifting to overall performance.

The company closed out June with $53.4 billion in long-term debt. billion the company has generated in net cash from operating activities since 2023 began. The metaverse remains an opportunity that could provide significant revenue for the company later this decade. Competitive advantages are what fuel the FAANG stocks.

The size, scale, diversification, and consistency of performance from our global real estate portfolio continues to provide us with excellent visibility to revenue and is a key reason why we have not had a single year of negative operational return in our 30 years as a publiccompany. Cineworld reduced its debt by $4.5

More details regarding our guidance assumptions can be found on Page 15 of the Company's Form 8-K supplemental that was filed early this morning. Over the past few months, we have made considerable progress addressing our debt maturities. million and the assumption of our partner share of debt. On to the balance sheet.

Anthony Schiavone: When a company generates free cash flow, there's a couple of ways that they can allocate that capital. They can either reinvest in the business, they can make acquisitions, they can pay back debt, repurchase shares, or the last one, which we like, they can pay a dividend. They're still investing heavily to grow.

Bill, IBM shares up eight percent post earnings, sending the stock to its highest level since 2013. Bill Mann: IBM is like the nickelback of AI companies. Like nobody wants to admit that they like it because, I mean, it's a company that's disappointed for so long. What has the market so excited about IBM?

Adjusted EPS increased more than $2, supported by strong profit growth and lower interest from debt reduction. With over $100 billion in debt reduction behind us and $7 billion return to shareholders in 2023, we remain fully focused day-in and day-out on using lean to improve how we serve our customers and deliver value for shareholders.

At the time of our initial public offering in 2013, we were operating just eight markets across four states. As of December 31st, our total debt was $1.25 billion, resulting in a debt-to-capital ratio of 40.2% and a net debt-to-capital ratio of 39.3%. In 2023, our geographic footprint continue to grow.

2023 marked our 25th anniversary as a publiccompany. Our total debt principal outstanding was approximately 29 billion as of December 31, 2023. Assuming the final maturity date of our hybrids, the weighted average life of our debt portfolio was approximately 19 years. Our weighted average cost of debt is 4.6%.

Note: This post was originally published on October 18, 2013, on the MarketingProfs blog , but it remains relevant today. To do so, the ECB would have to affirm its intent via language or stepped up daily purchases of peripheral debt on the order of five billion Euros or more. I have made some updates and additions.

Improvements to NOI guidance are fairly broad-based and are primarily driven by increases in base rent, tenant recovery revenues, increase in temporary tenant revenues, and, to a lesser extent, improvements in bad debt expense driven by collections of previously reserved receivables. The expected increases in core NOI guidance totaling $0.05

If you look back in history in just a little bit, taking you backwards, company was started in 2013 with $1 billion of equity capital. I would encourage you to look at some of the publiccompanies that trade out there. There are publiccompany peers out there who have done a great job. So now to Page 3.

We've continued to expand our asset portfolio, increasing our extensive pipeline network to more than 50,000 miles from approximately 30,000 miles in 2013 and adding nearly two Bcf per day of natural gas processing capacity and three fractionators. Another example, you know, publiccompany costs have been eliminated for the Magellan company.

They did not believe me, the stock price did not go 60 X because they had to raise money, they had to issue more equity than to take on debt. I was being told that I could divert up to 10% of my paycheck into my company's discounted stock purchase plan. That company was Schlumberger. They were 60 acts. It was a roll-up.

We typically invest between $5 million and $30 million in businesses generating between $2 million and $15 million in EBITDA through majority recap, minority growth capital, and debt/equity solutions. Zucker (“Zucker”), who serves as Managing Partner, and made his first private company investment in 1994.

We also made our largest direct, private equity commitment to date with Maxar Technologies, a global space technology and intelligence company whose customers include SiriusXM and NASA. This is an exciting opportunity which also involved an investment by our private debt team. million to just over $5 million which is close to the $5.3

After another strong year as a publiccompany, I'd like to start today by revisiting the algorithm we use to achieve sustained long-term growth. With respect to capitalization, as of December 31, 2023, we had $655 million in cash and cash equivalents, no long-term debt, and 122.5 Good afternoon, everyone. million over the $1.0

Cognex reported a strong cash position at the end of Q3 with $846 million in cash and investments and no debt. On the buyback front, our stated goal is to offset dilution from our employee equity programs, and we've been well ahead of that goal for quite some time right now since we pronounced it in the 2012, 2013 time frame.

So, yeah, I had a career in investment banking with Jefferies, and it was a really good professional experience because I do have the opportunity to work in M&A, equity and debt financing. I did in 2013 the largest banking transaction that the market had seen since the financial crisis, it was a $2.4 billion deal.

Carnival 's plans to pay off its heavy debt load. The company's really struggling to pay off a lot of debt. Most of their debt, fixed debt also good, so it's not subject to crazy interest rates. But with a company like this and with companies that carry heavy debt, how should we think about this?

Discovery 's debt-ridden saga, these stories aren't just tales of companies; they are lessons for life and investing. This could be a very important year in investing, given what this tech company has gone on to do. Fast forward to 2013. From 2013-2020, sales increased from about $8 billion to $86 billion.

We've paid out $5 billion of dividends since the company was started in 2013, and our total shareholder return for 2023 was 43%. We have the large REIT, and then we have our operating companies as well. Hey, you mentioned some unsecured debt being raised in the sector and possibly looking into some unsecured yourself.

Consumer debt servicing burdens are stable, near pre-pandemic levels. Still, high interest rates will probably remain a source of pressure for some consumers, especially those with higher debt servicing burdens. Credit cards are, you know, one of the two largest classes of floating rate consumer debt.

I know there’s been a big rush into private credit and private debt over the past few years. I think they have about $10 billion out of the 400 and change billion that’s in, in public equities. Most of what they do are, are real assets, credit debt, middle market banking. What they do is really fascinating.

They invest primarily in private and publiccompanies. That’s why I think being in Silicon Valley investing, in talking every day with venture capital companies, founders, et cetera, is a huge competitive advantage to us because we see the disruption coming years in advance. How do you think about that? Is it a bubble?

And then I don’t know what God smiled on me, but I got hired by the Wall Street Journal in 2013. RITHOLTZ: So you start in 2013, and then you proceed to get some major news stories that you either covered intimately or broke. You know, when I got hired in 2013, M&A was dead. And like, to some degree they kind of won.

RITHOLTZ: Whereas all the other publiccompanies had access to capital and managed to get into trouble. RITHOLTZ: So, you go from Lazard to Merrill to JPMorgan, tell us about those other experiences, how do they compare to Lazard which seems much more unique, being in a publiccompany versus a partnership. RITHOLTZ: Sure.

The national debt now sits around $35 trillion, with the annual cost to service this debt coming in at roughly $1.05 As an example, the world's largest publicly traded company by market cap, Apple (NASDAQ: AAPL) , has repurchased $700.6 trillion as of August 2024, per the U.S. Department of the Treasury. in the process.

For example, Harris has proposed tackling America's rapidly rising national debt by increasing taxation on select groups. Buybacks have been an especially useful tool America's biggest publicly traded companies have used to reward investors and boost their earnings per share (EPS). Meanwhile, Trump wants to impose tariffs on U.S.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content