This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The LP has delivered an average return on invested capital (ROIC) of 12% over the last 10 years. Its ROIC has also been in the double digits every year since 2005 -- a period that included the Great Recession, the oil price collapse of 2014 to 2017, and the COVID-19 pandemic. The company manages its debt well.

Airlines aren't productive (at least for shareholders) The ultimate test of whether a company is allocating capital productively for shareholders is the comparison between its return on invested capita l (ROIC) and its weighted average cost of capital (WACC).

Lower interest rates lower the cost of capital and can increase the return on investment for capital-intensive projects. Room for further balance-sheet improvements Since the oil and gas downturn of 2014 and 2015, Kinder Morgan has worked hard to restore its balance sheet and rebuild investor confidence in its dividend.

Yet, on the other hand, inflation and higher interest rates are a big counterweight to the bull case, as all major cruise companies are now loaded with debt -- a result of the emergency borrowing during the pandemic -- while also battling higher labor costs. Those ratios are about in line with the average during the 2014 to 2019 period.

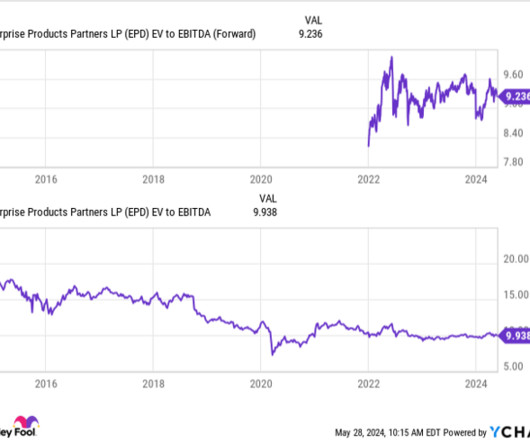

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

With a 34% return on invested capital (ROIC) , Home Depot generates outsize profitability compared to its debt and equity. HD Return on Invested Capital data by YCharts Historically, high-and-rising ROICs such as this have led to outperforming stocks. while only using 57% of its net income to fund these payments.

Exceptional profitability Best yet for investors, the company's high and rising return on invested capital (ROIC) makes these expansion plans even more promising. SFM Return on Invested Capital data by YCharts ROIC measures a company's ability to generate net income from its debt and equity.

Currently generating a return on invested capital (ROIC) of 15% versus a weighted-average cost of capital (WACC) of 10%, the company is creating value for shareholders, generating outsize profits compared to its debt and equity.

What makes these expansion plans look so promising for investors is that O'Reilly's return on invested capital (ROIC) of 67% is one of the highest on the market. Since 2014, Snap-on's net profit margin has risen from 11% to 20%, highlighting the company's robust pricing power and improving operational efficiency.

Actively consolidating its fragmented industry, Rollins has delivered a cash return on invested capital (ROIC) of 33%, highlighting how incredibly well it drives FCF creation via its many acquisitions. dividend yield is its highest since 2014, indicating that now may be a great time to dollar-cost average (DCA) into this steady-Eddie.

times net debt to EBITDA. And I just expect more and more -- and more importantly, we're seeing return on investment. We are still not at our high that was 97.1%, if I remember right, in 2014. Last thing I would mention, you just mentioned bad debt. We recasted our $3.5 billion in the year and ended the year at 5.2

So, they were granted in 2014, and I plan to exercise and hold while selling just enough to pay the cost of exercising and the taxes. Everett's done a really nice job of leading this team, but we see such strong return on investment there that we are going to raise some investment there. Over to you, Jeff.

Our primary goal was to smooth and extend existing debt maturities. In return, we have reduced our 2028 notes by $360 million and received $260 million in cash net of fees, bringing first-quarter pro forma cash to $912 million. Or is there something different here that can give you a quicker return on investment?

Over time, we expect this to drive greater returns on invested capital in both our mobility and broadband businesses that either would be expected to achieve as stand-alone operations. Our commitment to our investment-led strategy has played a pivotal role in our success and made AT&T the largest capital investor in the U.S.

Growing its return on invested capital (ROIC) from 10% in 2014 to 22% today, the company's ability to generate net income from its debt and equity is top-tier and improving with time. That's the beauty behind Cintas -- it does the ugly, behind-the-scenes work for businesses so they can focus on their actual operations.

John Graham, president and chief executive officer of the Canada Pension Plan (CPP) Investment Board, told BNN Bloomberg in an interview that he expects the U.S. to resolve its debt ceiling debacle and is looking to raise liquidity to take advantage of “opportunities” the fund sees in equity and fixed-income markets. Is it still 80%?

Most importantly for investors, Cintas' long-tenured management has a lengthy history of delivering profitable growth , as evidenced by the company's high and rising return on invested capital (ROIC) and improved cash generation. annually since 2014, further boosting shareholder returns.

But I really like these characters who are willing to take like crazy risks and they operate in gray areas like loan sharks, pump and dump schemers, debt collectors. How, 00:15:40 [Speaker Changed] How hard is it to show those audited returns? The, it’s not even return on investment, here’s our $50 billion.

Down 35% from its all-time high, the company trades at 18 times cash from operations (CFO) and has a dividend yield of 3.3%, both of which are near their most attractive levels since 2014. Both of these marks are near their most favorable levels since 2014. But don't just take my word on these valuation metrics being appealing.

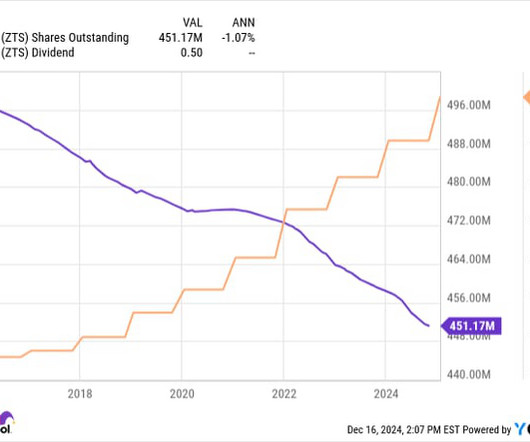

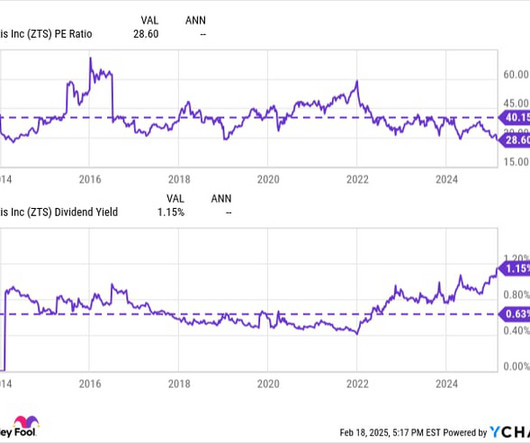

The company has been growing faster than the overall animal healthcare industry every year since 2014 thanks to its penchant for continuous innovation. Stocks with high and rising ROICs have historically outperformed their lower-ranked peers since they generate outsize profits compared to their debt and equity.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content