This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

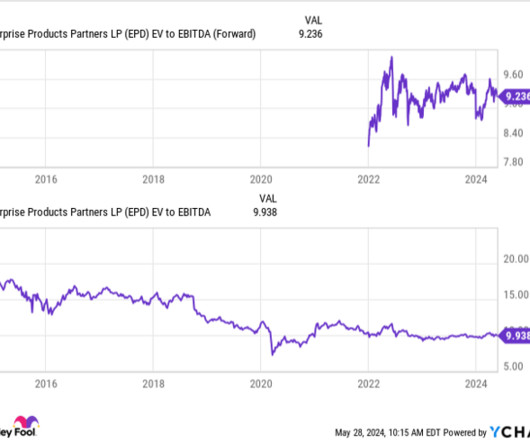

Between 2011 and 2016, MLPs traded at an average multiple of 13.7 in enterprise-value- to- EBITDA (earnings before interest, taxes, depreciation, and amortization), the most common way to value these stocks.

Battery Ventures established PST in 2016 through the acquisition of UK-based Michell Instruments. Battery was instrumental in laying the foundations for PST when the platform was established in 2016 and has continued to play a valuable role ever since. The company is led by CEO Adam Markin. billion fund closure in January 2021.

Cheap stocks Energy Transfer, Enterprise Products Partners, and Williams all have strong growth ahead from increasing natural gas demand. Midstream master limited partnerships (MLPs) traded at an average enterprisevalue to EBITDA multiple of 13.7 between 2011 and 2016. Data by YCharts.

This transaction marks the eighth and final portfolio company exit from CenterOak Equity Fund I LP , a 2016 vintage buyout fund. The firms second fund closed at its $690 million hard cap in April 2021, while its first fund closed in 2016 with $420 million of capital. billion hard cap.

Hilton (14%) Ackman's position in Hilton (NYSE: HLT) had a false start in 2016. Shortly after acquiring shares, the stock moved significantly higher in value, prompting Ackman to sell. Hilton's stock price performance has led shares to trade for an enterprisevalue -to- EBITDA ratio of about 30 times as of this writing.

21, 2016, and it rallied more than 6,100% to a record closing price of $139.51 From 2016 to 2024, its revenue grew at a compound annual growth rate (CAGR) of 36% as its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) increased at a CAGR of 41%. It went public at a split-adjusted price of $1.80

When Twilio (NYSE: TWLO) went public in 2016, it initially impressed investors with the disruptive potential of its cloud-based services. Twilio's first-mover advantage in this space, along with the expansion of the mobile app market, boosted its annual revenue at a whopping compound annual growth rate (CAGR) of 55% between 2016 and 2022.

The investor first accumulated shares of the largest hotelier in the world in 2016, but it wasn't until 2018 that he had an opportunity to establish a significant position in the stock during the market downturn. He saw an opportunity for the chain to double its store count from approximately 2,200 at the end of 2016. He gobbled up 2.9

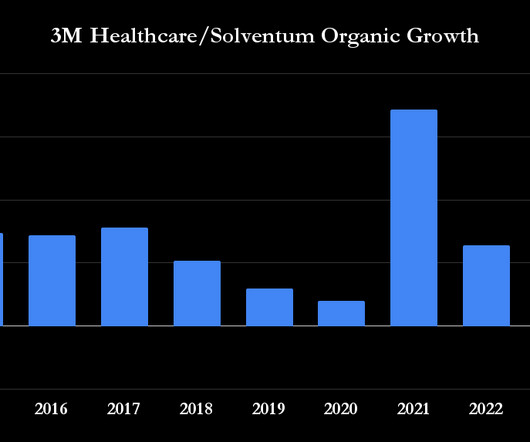

As for the 4%-6% expected end market growth, the figure looks familiar enough because it's what 3M's management told investors to expect from its healthcare end market on 3M's investor day in 2016 and 2019. However, whether it's 3M's healthcare business or Solventum, the company simply isn't growing near its estimate for end-market growth.

Chipotle Mexican Grill (19.5%) Ackman initially invested in Chipotle Mexican Grill (NYSE: CMG) in 2016 following food safety concerns, which left many customers seeking alternatives. Ackman has followed the company for a long time, briefly accumulating shares in 2016. Hilton's scale gives it several advantages.

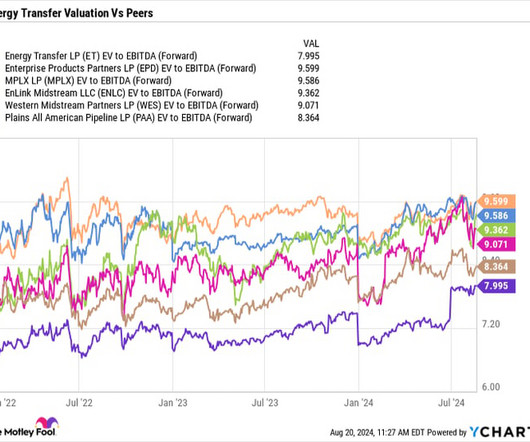

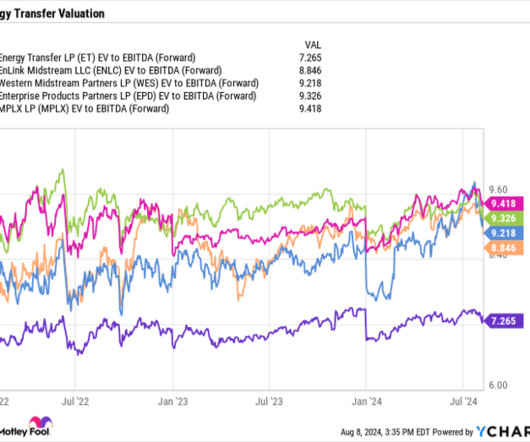

Multiple expansion opportunities From a valuation perspective, Energy Transfer is the cheapest stock among its master limited partnership (MLP) midstream peers, trading at 8x on a forward enterprisevalue -to-adjusted EBITDA basis. EV/EBITDA multiple between 2011 and 2016, so the industry as a whole has seen its multiple come down.

For example, in 2016 it posted an operating margin of 17.5%. This brings its enterprisevalue up to around $37 billion compared to its market cap of $24 billion. I think a better earnings ratio for Delta is enterprisevalue-to-free cash flow (EV/FCF) instead of the traditional P/E. in 2023, which equates to $5.5

Twilio went public at $15 in June 2016, and the share price skyrocketed to its all-time high of $443.49 The valuations and verdict With an enterprisevalue of $3.5 Twilio's enterprisevalue of $8.5 SentinelOne went public at $35 a share in June 2021, and its share prices more than doubled to a record high of $76.30

It's gone on a wild ride since its public debut Twilio went public at $15 per share on June 23, 2016, and it closed at its all-time high of $443.49 At its peak, its enterprisevalue reached $70 billion -- or 25 times the revenue it would go on to generate in 2021.

At the same time, Energy Transfer continues to trade at a forward enterprise-value -to- EBITDA multiple of 8 times based on 2025 estimates, which is well below historical levels, not to mention one of the lowest valuations in the MLP space. times EV/EBITDA average multiple between 2011 and 2016.

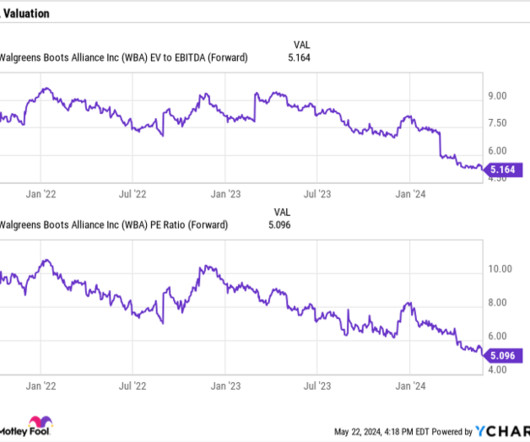

The company has consistently talked about this issue since at least the start of 2016. At a forward price-to-earnings (P/E) ratio of about 5 and enterprisevalue (EV)- to-EBITDA ratio of 5, Walgreens stock is inexpensive. So, there are, at the very least, signs that the segment will no longer be a drag on the company's results.

They can host websites or even build software without having to invest significant amounts of money in the infrastructure hardware; they can simply rent it from a company like Oracle, which officially launched Oracle Cloud Infrastructure in 2016 to better address its customers' needs.

The Singapore-based chipmaker Avago bought the original Broadcom in 2016, inherited its brand, and relocated its headquarters to the U.S. The "new" Broadcom subsequently expanded into the infrastructure software market by acquiring CA Technologies, cloud software giant VMware, and Symantec's enterprise security division.

Department of Defense (DOD) in 2016, and it currently holds a $131 million Agility Prime contract to deliver up to nine eVTOL aircraft to the U.S. Based on its current enterprisevalue of $3.08 billion, Joby is still richly valued at 30 times its projected sales for 2026. Joby started working with the U.S.

< Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6 times (one of the most common ways to value midstream stocks) is attractive and well below the 13.7

For example, on two separate investor day presentations (in 2016 and 2019), management forecasted 4% to 6% annual organic local currency sales growth. As previously articulated , the healthcare business has consistently failed to meet management's growth expectations over the last decade. at the end of 2022.

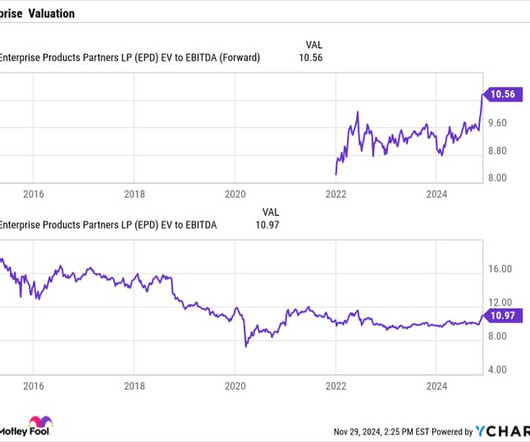

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5

He clarified his position in his 2016 letter to shareholders: “It is true that we own some stocks that I have no intention of selling for as far as the eye can see (and we’re talking 20/20 vision). If Hollub’s thesis on oil prices plays out over the next couple of years, it could turn out to be a great value.

Earthlite , a portfolio company of Branford Castle since July 2016, is a manufacturer of over 300 SKUs of massage tables, alternative beauty and wellness equipment, supplies and accessories, oils and creams, manicure and pedicure equipment, and medical exam equipment. We leave our partnership a much larger and stronger organization.”

It first bought Tesla shares in the fourth quarter of 2016. It forecasts robotaxis will account for an estimated 67% of Tesla's enterprisevalue by 2027. Tesla sells this as a software-as-a-service (SaaS) add-on that works toward powering a robotaxi business. per-share price range.

The company was founded in Boise, Idaho in 2016 by Evan Gines and today has two additional locations in Coeur d’Alene, Idaho and Seattle, Washington. The acquisition of Quick Dry and Spartan bring Guardian’s total acquisitions since platform launch to five. The firm invests across the United States, Canada, Europe and Australia.

Enterprise has increased its distribution annually for 26 consecutive years; Enbridge's streak is 29 years and counting. Kinder's streak is pretty meager in comparison, and it follows a dividend cut in 2016. That's hardly true, noting that even the 2016 dividend cut was made with the goal of best positioning the company for the future.

The cloud-based communications software provider went public at $15 in June 2016, and it reached its all-time high of $443.49 By the time its stock peaked in early 2021, its enterprisevalue hit $70 billion -- or 25 times the revenue it would generate in 2021. With an enterprisevalue of $7.8 in February 2021.

It has been growing rapidly, but as a relative newcomer that launched in 2016, it has yet to turn a profit. With an enterprisevalue-to-revenue multiple of 3, the analyst said the stock is expensive and investors can find better risk/reward trade-offs elsewhere.

In 2016, recognizing a clear need and opportunity, Thrust launched the Zero Time to Airline program and refocused its strategy on exclusively serving the professional pilot training market. Its sectors of interest include business and consumer services, light manufacturing, and value-added distribution.

Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. The first is that enterprisevalue takes into consideration the amount of net debt a company carries on its balance sheet. times average EV/EBITDA multiple between 2011 and 2016.

Global alternative asset manager Tikehau Capital has competed the sale of its stake in Preligens, a specialist leader in artificial intelligence for aerospace and defencem to Safran for an enterprisevalue of €220m. Completion of the deal follows an exclusive negotiation process that began in June 2024.

Mitchell Mayo , Dylan Mayo , and Steven Murff founded the company in 2016. ” LP First invests up to $10 million of equity in Southwest, Southeast, and Midwest-headquartered companies with enterprisevalues between $15 million and $75 million and EBITDA of $3 million to $10 million.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

The stock is down 62% since Greco took over as CEO in August 2016 while peers O'Reilly Automotive and AutoZone are up 222% and 202%, respectively, over the same time frame. For example, here's a look at enterprisevalue (market cap plus net debt), or EV, to earnings before interest, taxation, depreciation, and amortization ( EBITDA ).

Twilio's early mover advantage in this niche enabled it to grow like a weed after its public debut in 2016. Between 2016 and 2020, its annual revenue grew at a compound annual growth rate (CAGR) of 59%, from $277 million to $1.76 With an enterprisevalue of $8.3 Some of that growth was driven by acquisitions.

Reimbursement pressures have been the company's biggest issue The biggest issue facing Walgreens has been consistent prescription drug reimbursement pressure, which it has called out since at least the start of 2016. Enterprisevalue takes into consideration its net debt. It trades at a forward P/E of less than 4.5

The firm’s first fund closed in 2016 at its hard cap with $420 million of capital. “We The successful close of Fund III validates our active, clearly defined investment process and our team’s strategic focus on creating value for our investors and management teams.”

An attractively valued stock Energy Transfer trades at an attractive forward enterprisevalue (EV) -to-EBITDA multiple of just 7.3x. EV/EBITDA multiple the stocks averaged between 2011 and 2016. It has paid $2.3 billion in distributions thus far this year and should pay around $4.7 billion total for the year.

Attractive valuation Despite its strong performance this year, Enterprise's stock still trades at an attractive valuation from a historical perspective. Its enterprise-value -to-EBITDA (EV/EBITDA) multiple stands at 10.5, Before the pandemic, Enterprise would often carry an EV/EBITDA multiple of 15 or more.

The bears will argue that Supermicro is really just a legacy server maker that grew its revenue at a less impressive CAGR of 10% from fiscal 2016 and fiscal 2021 and then hitched a ride on Nvidia's coattails over the past two years. The valuations and verdict With a stock price of about $290 and an enterprisevalue of $14.1

It shed more than 98% of its value as it lost the smartphone market to Apple 's iPhones and Alphabet 's Google Android devices. It stopped producing its own smartphones in 2016 and tried to expand its software and licensing divisions, but those efforts failed to revive its stock. Based on those estimates and its enterprisevalue of $1.5

That equals nearly half of its enterprisevalue of $28 billion, and management plans to keep buying more Bitcoin. Arm was acquired by the Japanese conglomerate SoftBank in 2016 and spun off again last September. It ended its latest quarter with 226,500 Bitcoins on its balance sheet. It bought those for $8.3

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content