This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By and large, this structure has been eliminated, and MLPs are generally in better financial shape as a result, carrying less leverage and being able to grow their business through free cash flow. Between 2011 and 2016, MLPs traded at an average multiple of 13.7 The stock currently yields 6.4%

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6

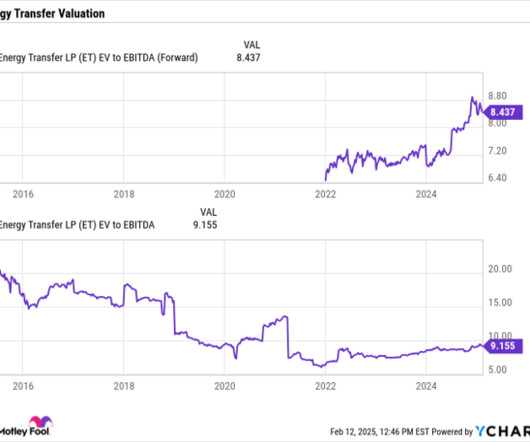

At the same time, Energy Transfer continues to trade at a forward enterprise-value -to- EBITDA multiple of 8 times based on 2025 estimates, which is well below historical levels, not to mention one of the lowest valuations in the MLP space. times EV/EBITDA average multiple between 2011 and 2016.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

The company's balance sheet is currently in good shape, with leverage (as used by rating agencies) toward the low end of its 4x to 4.5x Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple. times average EV/EBITDA multiple between 2011 and 2016. target range.

It ended the quarter with leverage of 3 times. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. This leverage is considered low in the midstream space given the strong cash flow these companies generate. The stock now has a forward yield of about 7.2%

times average enterprisevalue (EV) -to- EBITDA multiple between 2011 and 2016, while today most midstream stocks trade at under a 10 times multiple. EV/EBITDA tends to be the most used metric to value midstream companies, as it takes into consideration their debt positions and takes out non-cash expenses.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

Enterprise's consistency stems from its largely fee-based model, where the company only takes on minimal commodity or spread risk. Meanwhile, it has historically been conservative with its leverage, distribution coverage ratio, and growth capital expenditure (capex) spending. on average, between 2011 and 2016.

In a world where traditional media companies are struggling to stay afloat, spending money they don't have on digital initiatives, or leveraged to the point of unprofitability in a sluggish ad market, Sirius XM is cheap. The earnings multiple is a still reasonable 16 if you go by Sirius XM's bloated enterprisevalue.

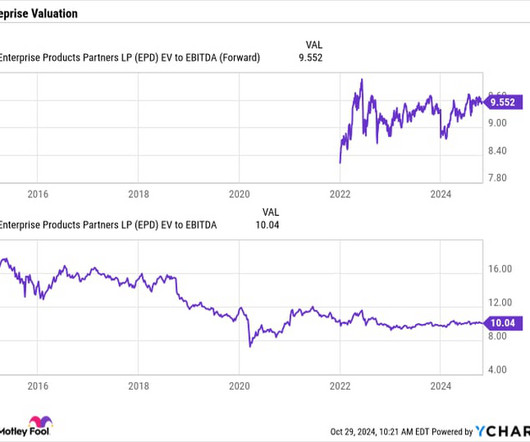

Based on its DCF, Enterprise's distribution coverage ratio was 1.7x. It ended the quarter with leverage of 3x, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. On that front, Enterprise trades at a forward EV/EBITDA multiple of 9.5

On and Lululemon both leverage their proprietary technologies to sell pricier products than most of their competitors. billion in revenue in fiscal 2015 (which ended in January 2016). Its enterprisevalue of 7 billion Swiss francs ($8.3 YOY = Year over year. By comparison, Lululemon generated $2.1 billion) or Nike ($167.9

I remember Tom Gardner was up in Canada in summer of 2016 and Ian Butler and I said, hey, let's introduce you to something. Even on a discounted cash flow basis, which you can now value Shopify at, which you couldn't back in 2016 when we bought it the first time, I've got a reasonable DCF. It's your time to speak.

Our increased participation in Cubico is aligned with PSP Investments’ long-term investment approach and strategy to leverage industry-specific platforms and develop strong partnerships with liked-minded investors and skilled operators,” commented Guthrie Stewart, Senior Vice President and Global Head of Private Investments at PSP Investments. “We

The company was acquired at a total enterprisevalue of $44 million, of which $8.3 And since that time, we've been an active contributor to its growth by leveraging our pharmaceutical grade cultivation and science driven approach to product innovation. They are a leading distributor of medical cannabis products in Australia.

billion in enterprisevalue to be funded by cash on hand. We are well-positioned to drive growth for HashiCorp by leveraging IBM's enterprise incumbency and global reach. We have leveraged watsonx to build AI assistance through our software portfolio. Clients value the flexibility of our approach.

Turning to the next strategic priority, we continue to leverage Genworth's LTC expertise to develop innovative agent care solutions. They operate as a closed system, leveraging existing reserves and capital current premiums, as well as future new premiums under the LTC multiyear rate action plan to cover liabilities.

With deep-rooted backgrounds in private equity, encompassing roles as investors and trusted advisors, we have actively contributed to transactions exceeding $2 billion in enterprisevalue.” Corum is also the leading industry educator with its popular conferences and publishes the most widely distributed software M&A research.”

As we all know, we've done it in a way where others have done it in a way to generate the quickest short-term returns through a lot of leverage. So it's clearly higher than it was in the 2019, 2018, 2017 level, and it kind of goes back to where we were in the 2014, 2015, 2016 level. At the same time, we've done it. Operator Thank you.

And what was interesting was the first leveraged buyout of a public company happened when I was in graduate school. KLINSKY: In 1979, it was the first leveraged buyout of a public company. We had sold the family business, maybe buy another family business one day through a leveraged buyout. KLINSKY: Yeah.

Playing the next track Sirius XM itself has been a Berkshire Hathaway position only since early last year, but Buffett has had some skin in the satellite radio game since 2016. The company has boosted its payout every year since initiating a distribution policy in 2016. Like most media stocks, Sirius XM is also highly leveraged.

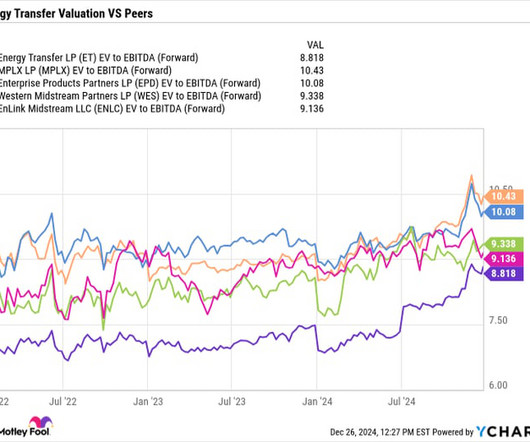

Despite Energy Transfer's strong position to benefit from the increasing power needs associated with AI, it is one of the cheapest MLP midstream stocks, trading at a forward enterprisevalue (EV)- to- EBITDA ratio of 8.8 The EV-to-EBITDA ratio is one of the most common ways to value pipeline stocks given their debt and growth capex.

It's also nicely improved its balance sheet over the past few years so that its leverage is now in the lower half of its targeted 4 times to 4.5 Meanwhile, it plans to buy back stock once its leverage target is achieved. times range. It is looking to grow its distribution by 3% to 5% a year moving forward. Image source: Getty Images.

With its balance sheet and leverage in good shape, it appears well positioned to tackle this growth opportunity. From a valuation perspective, the stock trades at an enterprisevalue (EV) -to-EBITDA multiple of about 8.5 times between 2011 and 2016. billion in distributions with its DCF given its projected EBITDA growth.

Hilton Worldwide (14.3%) Ackman started building a significant position in Hilton Worldwide (NYSE: HLT) in 2018 after holding shares for a short period in 2016. If anything, Hilton's ability to leverage its brand and loyalty program has become even stronger since then. in the third quarter.

BlackBerry is running out of good options After years of declining sales, BlackBerry stopped manufacturing its own phones in 2016 to focus on expanding its cybersecurity, IoT, and licensing businesses. But with an enterprisevalue of $2.7 With an enterprisevalue of $9.5 billion to $853 million.

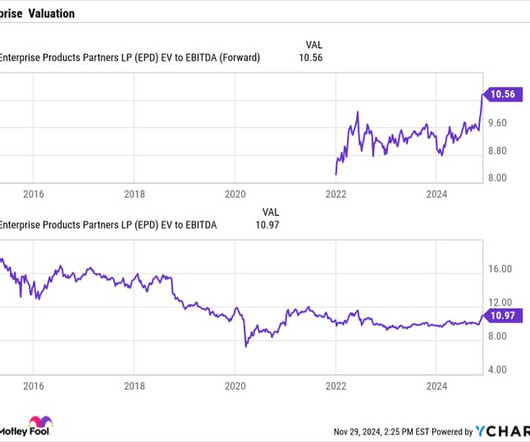

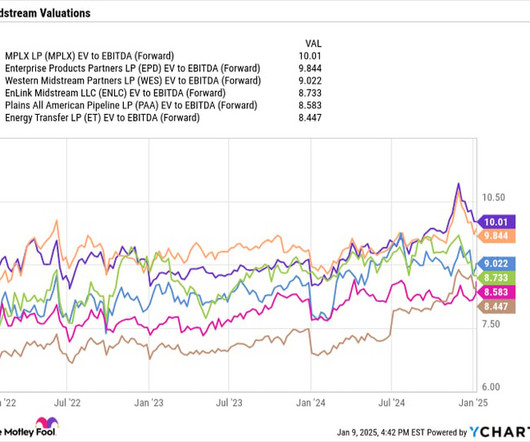

Enterprise Products Partners had a distribution coverage ratio of 1.8 It ended 2024 with a leverage ratio of 3.1 (It This is generally considered a low leverage ratio for the midstream industry, where levels between 3.5 that the average midstream master limited partnership (MLP) traded at between 2011 and 2016.

In addition, the company has a solid balance sheet with low leverage for the industry. Enterprise's distribution coverage ratio came in at a robust 1.7 Meanwhile, it ended the quarter with leverage of 3 times. Midstream companies typically carry leverage from 3x to 4.5x

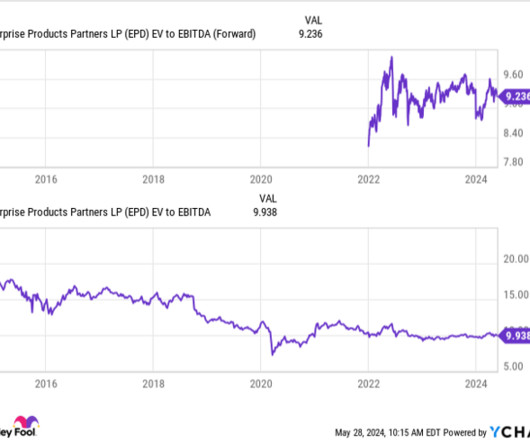

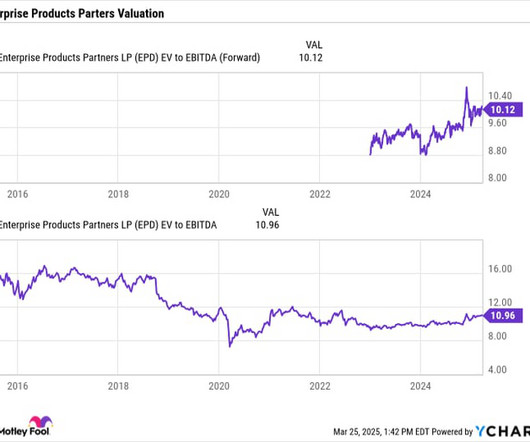

Enterprise currently carries leverage (net debt adjusted for equity credit in junior subordinated notes/EBITDA) of around 3.1 It currently trades at an enterprisevalue (EV) -to-EBITDA multiple of 10, which is the most common metric used to value midstream companies.

That said, the company has really improved its balance sheet and leverage over the past few years, so it is in good shape to pursue these additional opportunities. An attractive value Despite its strong performance and burgeoning growth opportunities, Energy Transfer continues to trade at both a relative and a historical discount.

In addition to these growth opportunities in front of it, Energy Transfer is cheap compared to its peers and from a historical level, trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just 8.4 times between 2011 and 2016. billion.

Learn More Midstream companies, meanwhile, now operate with lower leverage and have more robust coverage for their distributions. times that midstream master limited partnerships (MLPs) averaged between 2011 and 2016. Western Midstream's balance sheet is in stellar shape, with leverage below 3x, and it generated $1.3

At year-end, leverage stood at just 3.3 billion this year, while staying within our target leverage range of four to five times net debt to EBITDA without raising any additional equity. times pro forma net debt to recurring EBITDA. We can deploy over $1.5 billion and $1.3 billion in 2025, across all three external growth platforms.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content