This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many of these companies are structured as master limited partnerships (MLPs), which pass through their profits to their unitholders and as such don't pay corporate taxes. This portion is tax deferred until the stock is sold and reduces the owner's cost basis. This is a nice benefit, although it does add some paperwork come tax time.

21, 2016, and it rallied more than 6,100% to a record closing price of $139.51 From 2016 to 2024, its revenue grew at a compound annual growth rate (CAGR) of 36% as its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) increased at a CAGR of 41%. million today.

The investor first accumulated shares of the largest hotelier in the world in 2016, but it wasn't until 2018 that he had an opportunity to establish a significant position in the stock during the market downturn. He saw an opportunity for the chain to double its store count from approximately 2,200 at the end of 2016. He gobbled up 2.9

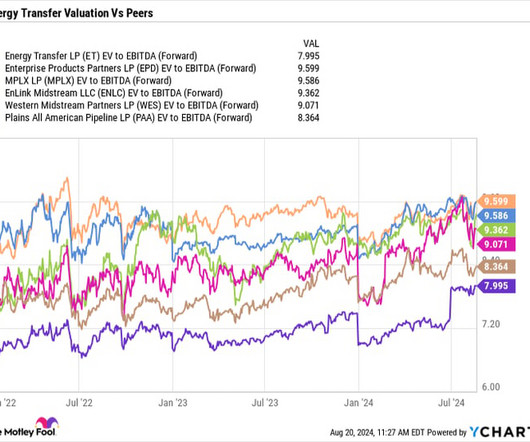

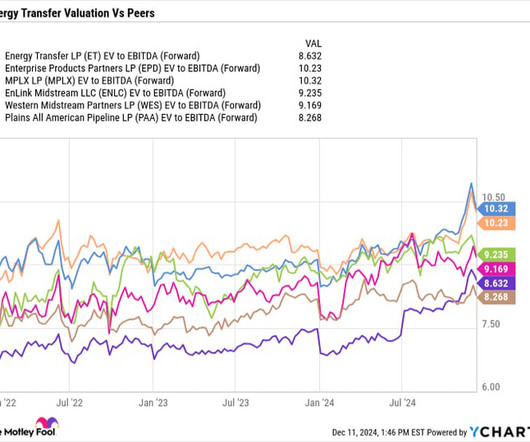

million in EBITDA (earnings before interest, taxes, depreciation, and amortization) a year. Multiple expansion opportunities From a valuation perspective, Energy Transfer is the cheapest stock among its master limited partnership (MLP) midstream peers, trading at 8x on a forward enterprisevalue -to-adjusted EBITDA basis.

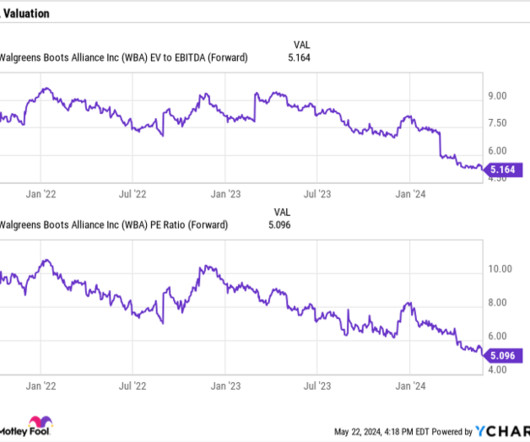

The company has consistently talked about this issue since at least the start of 2016. billion after-tax goodwill write-down of its VillageMD investment in an admission that it greatly overpaid for the business. During its most recent quarter, Walgreens took a $5.8 For a company with $8.8 For the quarter, the company's U.S.

The Singapore-based chipmaker Avago bought the original Broadcom in 2016, inherited its brand, and relocated its headquarters to the U.S. The "new" Broadcom subsequently expanded into the infrastructure software market by acquiring CA Technologies, cloud software giant VMware, and Symantec's enterprise security division.

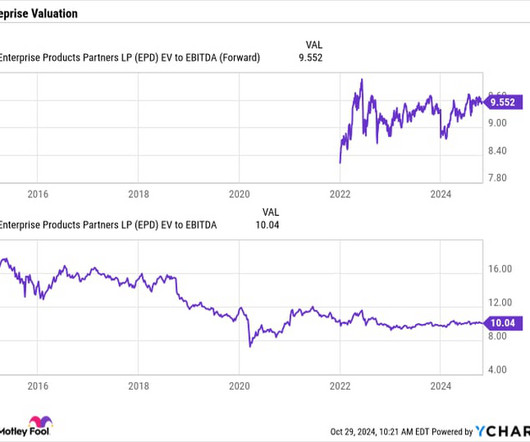

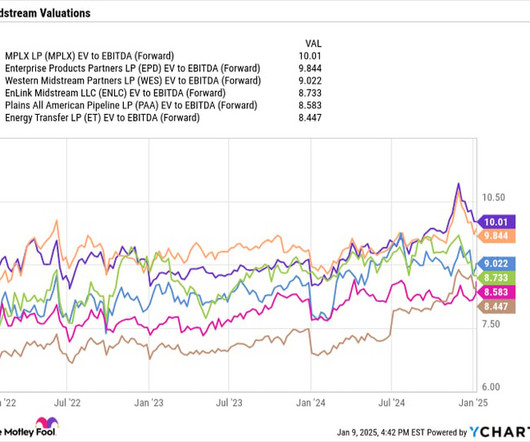

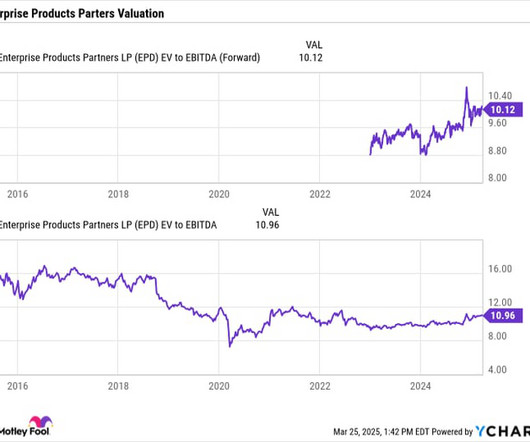

< Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprisevalue (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6 times multiple the sector traded at between 2011 to 2016.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5

Enterprise-value-to-EBIT ratio 714 12.3 EBIT = earnings before interest and taxes. The company has offered high-performance processors for the data analytics and AI markets since 2016. The stock is also far more affordable as measured by several key metrics. Metric AMD TSMC Price-to-forward-earnings ratio 38.9

He clarified his position in his 2016 letter to shareholders: “It is true that we own some stocks that I have no intention of selling for as far as the eye can see (and we’re talking 20/20 vision). If Hollub’s thesis on oil prices plays out over the next couple of years, it could turn out to be a great value.

While similar, distributions include a return on capital that is untaxed until the units are typically sold, making them tax-deferred. However, investors do receive what is called a K-1 and must fill out some extra tax forms. Typically, investors value midstream companies using an enterprise-value -to-EBITDA (EV/EBITDA) multiple.

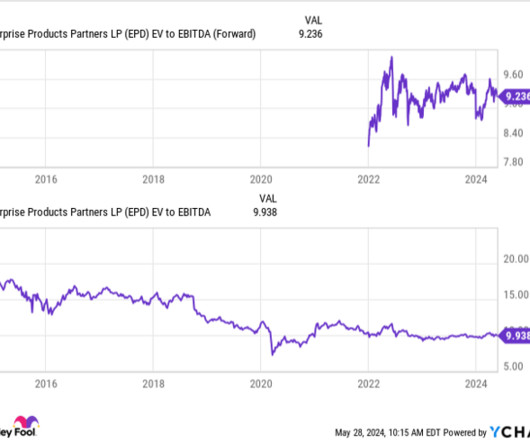

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

Enterprise has increased its distribution annually for 26 consecutive years; Enbridge's streak is 29 years and counting. Kinder's streak is pretty meager in comparison, and it follows a dividend cut in 2016. That's hardly true, noting that even the 2016 dividend cut was made with the goal of best positioning the company for the future.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

Reimbursement pressures have been the company's biggest issue The biggest issue facing Walgreens has been consistent prescription drug reimbursement pressure, which it has called out since at least the start of 2016. Enterprisevalue takes into consideration its net debt. It trades at a forward P/E of less than 4.5

We also got some commentary from Shopify President Harvey Finkelstein, about just how the company is helping its merchants with taxes, how wonderful what are your highlights from the quarter? I remember Tom Gardner was up in Canada in summer of 2016 and Ian Butler and I said, hey, let's introduce you to something.

It shed more than 98% of its value as it lost the smartphone market to Apple 's iPhones and Alphabet 's Google Android devices. It stopped producing its own smartphones in 2016 and tried to expand its software and licensing divisions, but those efforts failed to revive its stock. Based on those estimates and its enterprisevalue of $1.5

A consistent performer The key to Enterprise's success over the years has been consistency, which has helped the pipeline company increase its distribution for 26 straight years through various ups and downs in the energy markets. For Q2, the Enterprise saw its total gross-operating margin increase nearly 11% to $2.4

These growth opportunities should lead to continued earnings before interest, taxes, depreciation, and amortization ( EBITDA ) and cash flow growth, which should also help lead to increased distributions in the coming years. Enterprisevalue (EV) to EBITDA is typically the preferred metric investors use when valuing midstream companies.

In its third quarter, Enterprise's total gross operating profit increased 5% to $2.45 Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) also rose 5% to nearly $2.44 After the current period of outsized spending on growth projects, Enterprise does expect to settle back into a lower range thereafter.

billion (€7 billion) and that's because Cubico has been growing its operations nicely, expanding its enterprisevalue. Last year I noted that according to sources, the reported sale price of USD $6 billion is about 10 times its earnings before interest, taxes, depreciation, and amortization (EBITDA) of $641 million in 2022.

billion in enterprisevalue to be funded by cash on hand. Since we put the world's first quantum system on the cloud in 2016, we have deployed over 80 quantum systems, and our users have run over 3 trillion programs to date. billion of operating pre-tax income, and $1.68 Let me start with the details of the transaction.

On a statutory accounting basis, pre-tax income for the U.S. life insurance companies is estimated at 30 million, driven by 21 million of pre-tax earnings in LTC. Looking ahead, Genworth's enterprisevalue and future potential are rooted in our 81.6% Complete statutory results for our U.S. life insurance companies.

With deep-rooted backgrounds in private equity, encompassing roles as investors and trusted advisors, we have actively contributed to transactions exceeding $2 billion in enterprisevalue.” To do that, you need a succession plan that fulfills your desires and addresses all the issues of estate planning and taxes.

So it's clearly higher than it was in the 2019, 2018, 2017 level, and it kind of goes back to where we were in the 2014, 2015, 2016 level. The after-tax gain is associated with the ABG raising of primary capital, which we get diluted down. So it's a – we have a dilution gain after tax, it was $0.07. So it's a good sign for sure.

In order to do that, you need a succession plan that fulfills your desires and addresses all the issues of estate planning and taxes. With deep-rooted backgrounds in private equity, encompassing roles as investors and trusted advisors, we have actively contributed to transactions exceeding $2 billion in enterprisevalue.”

Coke is probably other than around the panic in 2020 at the beginning of March, about as good a price on enterprisevalue to bit, or sales price to earnings as it's been since about 2016, early 2017. Unless we have some sort of terminal illness, you don't know when you're going to pass on to that great tax shelter in the sky.

In the history of our private equity effort, we’ve generated over $70 billion of enterprisevalue gains without one missed interest payment, and added over 61,000 jobs without one missed interest payment. My firm has never had a bankruptcy, never missed an interest payment. We’re working with all sorts of people.

Broadcom, which was known as Avago before it acquired the original Broadcom and inherited its brand in 2016, is more diversified. Its infrastructure software business -- which it expanded through its acquisitions of CA Technologies, Symantec's enterprise security division, and VMware -- provides a mix of on-premises and cloud-based software.

The difference between the two is tax-related, as distributions have a return of capital component that is tax-deferred. While it involves a little extra paperwork come tax time, this part of the distribution reduces an investment's cost basis and is not taxed until the stock is sold, which is a nice added bonus.

One of those winners is Broadcom (NASDAQ: AVGO) , which still has a bright future after nearly doubling in value over the past 12 months. Understanding Broadcom's business Back in 2016, the Singapore-based chipmaker Avago acquired the original Broadcom. Here's why Broadcom is still a great place to park a modest $1,000 investment.

The company is structured as a master limited partnership (MLP) , which is not taxed at the corporate level and thus passes through much of its income to investors in the form of distributions. Distributions are similar to dividends but are more favorably taxed. Where to invest $1,000 right now?

A consistent performer When it comes to its earnings reports, Enterprise Products Partners typically doesn't have too many surprises up its sleeve, as it operates a steady, fee-based midstream business. Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, increased by 4% to nearly $2.6

This gives the company solid visibility into future cash flows and EBITDA (earnings before interest, taxes, depreciation, and amortization), the two metrics by which midstream companies are most commonly evaluated. times EV/EBITDA multiple on average that midstream MLPs traded at between 2011 and 2016.

Given that most of these projects won't be complete until later 2025 or 2026, the increased capex should have a larger impact on the growth of earnings before interest, taxes, depreciation, and amortization (EBITDA) in 2026 and 2027. between 2011 and 2016. Energy Transfer is projecting mid-teens returns on its growth projects.

In addition to these growth opportunities in front of it, Energy Transfer is cheap compared to its peers and from a historical level, trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just 8.4 times between 2011 and 2016.

That top-line miss was minor, but it had also predicted its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) would turn positive by 2023. But with an enterprisevalue of $375 million, it looks cheap at 1 time next year's sales.

At the same time, it also has one of the cheapest stocks in the space, with it trading at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of just over 8 times. times that midstream master limited partnerships (MLPs) averaged between 2011 and 2016.

Midstream companies are typically valued using an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) metric. times EV/EBITDA multiple between 2011 and 2016. Image source: Getty Images. An attractive valuation At under $20, Energy Transfer's stock is cheap.

Approximately 90% of Energy Transfer's adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) comes from fee-based businesses, while Enterprise has said that about 80% of its cash flow is fee-based. times enterprisevalue -to-EBITDA (EV/EBITDA) multiple the group traded at between 2011 and 2016.

Our total debt to enterprisevalue was approximately 27%, while our fixed charge coverage ratio, which includes principal amortization and the preferred dividend, is very healthy at 4.4 Pro forma for the settlement of our outstanding forward equity, net debt to recurring EBITDA was approximately 3.3

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content