This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many of these companies are structured as master limited partnerships (MLPs), which pass through their profits to their unitholders and as such don't pay corporate taxes. This portion is tax deferred until the stock is sold and reduces the owner's cost basis. This is a nice benefit, although it does add some paperwork come tax time.

The sector has gone through a transformation in the past decade, with midstream companies reducing leverage and being more disciplined when it comes to funding growth projects. multiple that midstream MLPs traded at between 2011 and 2016. All three stocks trade well below the MLP average multiple from that 2011-to-2016 period.

This was the case for Kinder Morgan in 2016, when it cut its dividend by roughly 75%. KMI Financial Debt to EBITDA (TTM) data by YCharts That said, a part of the problem was Kinder Morgan's more aggressive use of leverage than its peers'. Kinder Morgan's leverage is lower today, but it still tends to use more leverage than Enterprise.

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprise value (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6

The Trade Desk also continues to expand its ecosystem with Solimar, an AI-powered platform that leverages its first-party data to place ads without relying on third-party data; Unified ID 2.0, The Trade Desk went public in September 2016. How much larger could The Trade Desk grow?

Interestingly enough, it wasn't Warren Buffett who initiated his company's position in the $3 trillion company back in 2016; rather, it was his two investing managers, Todd Combs and Ted Weschler. For comparison, Kroger's net leverage ratio at the end of its fiscal first quarter 2023 was a much-healthier 1.3 times EBITDA.

billion in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and $1.2 Sirius XM initiated quarterly distributions in late 2016, and the rate has gone up every year. Sirius XM is also starting to pay down its long-term debt since that bearish leverage peaked in 2022. The model works.

For example, its ratio of debt to EBITDA ( earnings before interest, taxes, depreciation, and amortization ) is generally among the lowest of its closest peer group. Acquisitions are partly to blame for that trend, but investors need to understand that leverage increases risk. Trust The next big issue here is less tangible.

The company is paying about 10 times estimated 2024 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) for these assets. times leverage ratio , down significantly from 4.8 That implies they will supply it with about $200 million of incremental earnings next year. billion to $6.8 times in 2018.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. How about tax-deferred distributions.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. How about tax-deferred distributions.

However, a crucial part of being an industrial conglomerate is using cash flow and financial leverage to acquire or internally develop new businesses. billion in net debt compared to earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of about $9.5

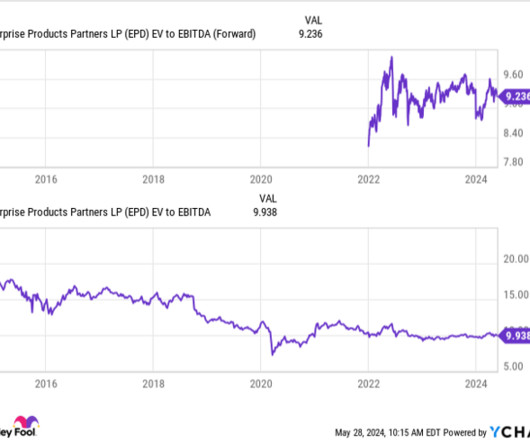

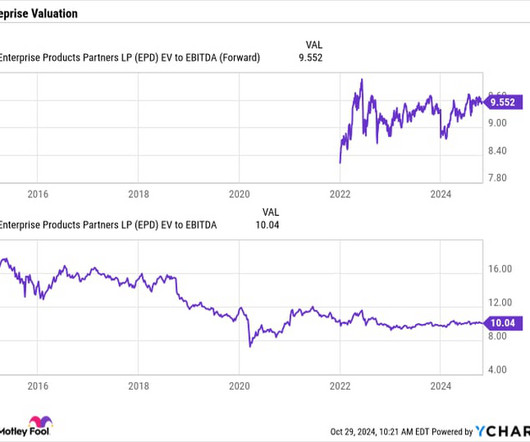

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprise value (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower.

As the chart below highlights, Energy Transfer's debt-to- EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio has come down materially over the past decade. In fact, Enterprise's leverage is generally at the low end of the industry relative to similarly sized peers. No company is perfect, but why settle?

In fact, the company's debt-to-EBITDA ( earnings before interest, taxes, depreciation, and amortization ) is actually lower today than it was at the start of 2023. What's interesting is that Enbridge's leverage is right in line with some of the largest utilities, and its business has a notable utility component to it. Data by YCharts.

That's going to be something that gives it a lot more leverage and plenty of leverage now, just not as much as it used to have. I'd like to put my gross stocks in my Roth IRA because their growth in value won't be taxed. Some of the investments you mentioned, you're right, REITs are the most tax inefficient.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, climbed 10% to nearly $2.4 It ended the quarter with leverage of 3 times. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA.

While similar, distributions include a return on capital that is untaxed until the units are typically sold, making them tax-deferred. However, investors do receive what is called a K-1 and must fill out some extra tax forms. EV to EBITDA = enterprise-value-to-EBITDA (earnings before interest, taxes, depreciation, and amortization).

We also got some commentary from Shopify President Harvey Finkelstein, about just how the company is helping its merchants with taxes, how wonderful what are your highlights from the quarter? I remember Tom Gardner was up in Canada in summer of 2016 and Ian Butler and I said, hey, let's introduce you to something.

Meanwhile, Kinder Morgan has been working to reduce leverage, with its debt-to-EBITDA ( earnings before interest, taxes, depreciation, and amortization ) ratio falling 30% from its peak levels in 2018. Kinder Morgan cut its dividend by 75% in 2016. But here's where a bit of a complication comes in. Sell Kinder Morgan?

If you had invested $25,000 in The Trade Desk 's (NASDAQ: TTD) initial public offering (IPO) in 2016, your investment would be worth $1.07 Its redesigned platform Solimar leverages artificial intelligence to gather more first-party data for targeted ads. million today. CTV ad spending in just the U.S. Its Unified ID 2.0

As shown in the chart above, the company adds leverage during weak patches to continue investing in its business and paying dividends. When the market recovers, it reduces leverage to prepare for the next downturn. That includes years like 2014-2016, when oil prices plunged, forcing some oil and gas companies to cut their dividends.

The key numbers Broadcom, which was known as Avago until it acquired the original Broadcom in 2016, previously generated most of its revenue by selling chips for the mobile device, data center, networking, wireless, storage, and industrial chip markets. Image source: Getty Images.

Enbridge is shifting the mix In 2016, nearly three-quarters of Enbridge's earnings before interest, taxes, depreciation, and amortization (EBITDA) was derived from its oil pipelines. That's not uncommon for acquisitions and will help the company maintain its leverage within management's target levels.

The company posted revenue growth of 23% to $464 million, and its margins improved from a year ago, with adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) improving from 37% to 39%. In a difficult environment in the digital advertising industry, The Trade Desk continues to deliver strong results.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) also rose 5% to nearly $2.44 It ended the quarter with leverage of 3x, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. It produced distributable cash flow (DCF) of $1.96

While Berkshire has owned the Liberty Media tracking stock since 2016, which tracked Liberty's large stake in Sirius, Berkshire has increased its bet on the satellite radio operator this year, ahead of the tracking stock's merger with publicly traded Sirius shares in a simplification merger in September.

Both represent the same entity, but they have slightly different tax considerations. And its steadily rising distribution, which has had a compound annual growth rate of 6% since 2016, is proof that investors will benefit as Brookfield Renewable grows. It expects its leverage ratio to be below 3.9 this year and fall toward 3.6

However, with $62 billion of non-cancellable leases on its books -- and generating over $5 billion annually in earnings before interest, taxes, depreciation, and amortization (EBITDA) -- the company should easily handle its debt obligations. Now trading with its highest-ever 3.5%

We leverage the Activate platform daily within our organization. And the most exciting part is that we're just getting started, and we have significant opportunity ahead of us to continue to leverage our partners and our learnings. Our adjusted tax rate for the quarter was approximately 19%, as compared to 19% in the prior year.

We are well-positioned to drive growth for HashiCorp by leveraging IBM's enterprise incumbency and global reach. We have leveraged watsonx to build AI assistance through our software portfolio. And finally, we are seeing our infrastructure segment play a larger role as clients leverage their hardware investments in their AI strategies.

First, we're expanding in payments by continuing to win deals with a diverse set of customers, powering growth and acceptance, capturing a prioritized set of new payment flows, and exploring new ways to ensure payment choice by leveraging multiple alternatives, including card rails, ACH, blockchain, and open banking. includes a $0.22

Where appropriate, we may refer to non-GAAP financial measures to evaluate our business, specifically adjusted EBITDA, a measure of earnings before interest, taxes, depreciation, amortization, and share-based compensation. And then as we look ahead in 2016, we'll layer on Medicine PANOVA there with those launches.

This activity is consistent with how customers are spending money in the 2016 to 2019 timeframe. billion in net income after tax. With NII now growing and complementing our fee growth along with our continued solid expense discipline, we expect to return to operating leverage as we move through the quarters in 2025. Alastair M.

On a statutory accounting basis, pre-tax income for the U.S. billion earnings -- pre-tax earnings benefits in 2023 from LTC in-force rate actions and settlements were offset by higher claims as the blocks age. Our second strategic priority is to leverage Genworth's LTC expertise to develop new, innovative aging services and solutions.

Across the world, we are leveraging our scale and local expertise to navigate varying local market dynamics. In Japan and South Korea, we had solid volume growth and won value share due to good traction on brand relaunches which leveraged enhanced taste and refreshed packaging and stepped-up performance in e-commerce channels.

Meanwhile, our leverage profile continues to improve as free cash flow grows, allowing us to increase the return of capital to shareholders through the recurring dividend and opportunistic share repurchases. Opex excluding gaming tax per day was $4.2 The opex excluding gaming tax was approximately $2.55 billion in the U.S.

From 2016 through 2020, Maravai acquired companies, including TriLink BioTechnologies and Cygnus Technologies in 2016, Glen Research in 2017. The capability and infrastructure additions that came from pandemic-era investments give us a foundation for exceptional operating leverage going forward. This was Maravai 1.0,

We are doing this by enhancing our innovation playbook, accelerating sustainability and software offerings, increasing penetration of our installed base, and leveraging our leadership position in high-growth regions. While tax was a bit lighter relative to our first-quarter guide, our full-year tax expectations have not changed.

Our increased participation in Cubico is aligned with PSP Investments’ long-term investment approach and strategy to leverage industry-specific platforms and develop strong partnerships with liked-minded investors and skilled operators,” commented Guthrie Stewart, Senior Vice President and Global Head of Private Investments at PSP Investments. “We

Average deposits also remained relatively stable while ending deposits declined modestly during the quarter, consistent with seasonal tax-related patterns. These declines in the second quarter reflect anticipated tax seasonality. years relative to the $50 million pre-tax loss recorded this quarter. That's helpful.

Over 50% of that revenue growth coming from our non-rates businesses with nearly 40% of the revenue growth coming from our international business, which has averaged 18% since 2016. Muni has produced high single-digit growth driven by a pickup in tax loss harvesting, while credit derivatives continued to see softer industry trends.

They started with Cloudflare back in 2016 as a free customer and today use nearly all our products, spanning use cases as diverse as remote application access, workers, serverless development, and bot management. We expect operating income in the range of $50 million to $51 million, and we expect an effective tax rate of 11%.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content