This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

But in 2018, it went public once again at about $23 per share (adjusted for subsequent stock splits ). 28, 2018, Dell returned to the stock market as a publicly traded company, but it wasn't a no-brainer buy. 3, 2018, Dell had a pro forma net loss of $1.2 The public history for Dell seemed to be over. Why Dell 2.0

In fact, Microsoft and Nvidia have more cash and equivalents like marketable securities than long-term debt, hence the negative figures. NVDA net total long-term debt (quarterly) data by YCharts. Oil and gas is capital intensive, and so is investing in AI. Microsoft pays more dividends than any other U.S.-based

It currently trades 75% below its all-time high from January 2018. 31, the company still carried almost $29 billion in long-term debt on its balance sheet. This is evidenced by the company's extremely low return on invested capital (ROIC). That gain is well ahead of the S&P 500 index's rise over the same period.

Best-in-class profitability In addition to this advantage from monetizing the by-product of its core collections business, Waste Management has historically held higher return on invested capital (ROIC) figures than its two most prominent peers. ROIC shows that it is the best in its industry at reinvesting in its business.

Running a backtest from 1991 to 2018, Research Affiliates found that stocks removed from the major indexes went on to outperform the broader market by five percentage points annually over the next five years. As counterintuitive as this sounds, it makes some sense.

However, one goal may be even more important than all of these : reducing debt. Carnival's debt load remains alarming While Carnival's revenue and operating income have exceeded pre-pandemic levels, the cruise company's stock is still 68% below its all-time high of $66 , reached in early 2018. billion in long-term debt.

You have a lot of high-interest debt If you have a lot of debt you're paying a lot of interest for, investing may not be the right move to make. You may want to focus on taking care of those loans first if doing so would give you a better return. You'll want to do this before you begin investing though.

The company's balance sheet also remains in good shape, with net debt (adjusted for equity credit in junior subordinated notes) standing at three times adjusted EBITDA. It has an investment-grade rating on its debt and its weighted average cost of debt is only 4.7%, which is attractive in the current high interest rate environment.

On the bottom line, Carnival continued to move in the right direction though the company is still facing stiff headwinds from its heavy debt burden, which jumped during the pandemic. The company is making progress on easing its debt burden as it prepaid more than $1 billion in short-term, variable-rate debt, though it still has about $7.5

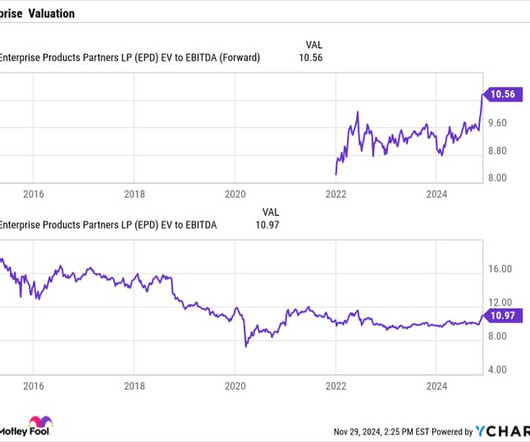

It has averaged a return on invested capital (ROIC) of about 12% over the past decade. Enterprise value takes into consideration a stock's net debt, while EBITDA removes non-cash expenses. The company currently plans to spend between $3.25 billion to $3.75 On that basis, Enterprise is trading at just over a 9x multiple.

If you followed our company for the last several years, you'll remember that since 2018, 3D Systems has been in a terrific partnership with United Therapeutics, with a goal of developing the world's first 3D-printed biocompatible human lung. If you followed our -- let me give you a little more color on what that means in layman terms.

Iron ore production reached 328 million tons, the highest level since 2018 and above our original guidance. This resulted in higher realized iron ore premiums, but more importantly, higher margins and returns on invested capital. They should rather be treated as a type of debt amortization. billion in the quarter.

Stocks tend to deliver strong long-term return on investment (ROI) When you invest in stocks, you're (ideally) doing it because you want your money to grow as much as possible in the long run. average annual returns for the past 30 years. Here's what that looks like in real life: the S&P 500 Index has delivered 10.7%

Growing private label sales Sprouts brand private label sales have risen from 14% of revenue in 2018 to 20% in 2023. Exceptional profitability Best yet for investors, the company's high and rising return on invested capital (ROIC) makes these expansion plans even more promising.

Meanwhile, its fledgling (2018 launch) medical unit has seen a rapid uptake -- even being used at temporary hospitals in Central Park during the pandemic. Steady profits and history of returning it all to shareholders Making the investment case all the more alluring for Omega Flex is its stellar return on invested capital (ROIC) of 30%.

Its wide moat means that as long as the company operates efficiently, it could generate market-beating returns over the long haul. And historically, it has done just that, generating a 12% cash return on invested capital over the last decade. MTN Cash Return on Capital Invested (CROCI) (TTM) data by YCharts.

My favorite example of the species is Q4 of 2018. 2018 was a dismal year for the market. The marijuana stock sector, which was big in Canada in 2018, it was down. The marijuana stock sector, which was big in Canada in 2018, it was down. But like every major asset class, nothing made money in 2018. Bitcoin was down.

Whether it's due to their frustration that Enbridge didn't allocate capital in a way that would be more directly beneficial to them, or they're fretful of the company's more debt-laden balance sheet, investors have clicked the sell button in response to the deal. In Kinder Morgan's favor is a strong U.S.

Better yet, the company has averaged a cash return on invested capital (ROIC) of 61% since 2018. This metric measures a company's FCF-generating abilities compared to its debt and equity -- the higher, the better.

However, as of the beginning of August, lemon pricing has steadily been increasing for all grades and sizes with prices up compared to the last few years and at the highest level since 2018. Debt less cash on hand as of July 31, 2023, was $30.2 Long-term debt as of July 31, 2023 was $40.7 million compared to $104.1

In line with our stated financial strategy after funding our dividend, Core continued to dedicate free cash to paying down debt. During the quarter, Core's net debt was reduced by $15.8 This reduction in our outstanding debt also decreased our leverage ratio to 1.66, down from 1.76 million, net debt was $132.3 million.

In line with our stated financial strategy, after funding our dividend, Core continued to dedicate free cash to paying down debt. During the third quarter, Core's net debt was reduced by nearly $12 million or 9%. This reduction in our outstanding debt also decreased our leverage ratio to 1.47, down from 1.66 last quarter.

All of these actions have positioned our company to be in a stronger financial position, with our balance sheet rightsized and our net debt position at the lowest level since becoming a publicly traded company. Debt less cash on hand as of October 31, 2023 was $37.4 Long-term debt as of October 31, 2023 was $40.6

For a healthcare customer who has been with us since 2018. billion in cash, cash equivalents, and marketable securities and no debt. Where we're really focused now is where to really prioritize our dollars where you have the highest return on investment, especially as we're planning for next year.

At the midpoint of our guidance this year, we anticipate savings of over $40 million of SG&A, including bad debt relative to 2023. For 2018 and at the midpoint of our 2024 outlook, we expect to reduce cash SG&A, excluding bad debt as a percentage of revenue by roughly 210 basis points in Europe, Africa, and LatAm in aggregate.

Last month, we completed a very successful $16 billion debt exchange offer and consent solicitation. That all said, our investments are focused on return on invested capital, right, which is now also included in our executives long-term incentive compensation. We're making progress on all. I did a little homework.

When fully mature, investment income is expected to represent about 70% of the additional CPP’s total revenues (investment income plus contributions). The base CPP is a “partially funded” plan. At the same time, we seek to maintain a stable contribution rate for current and future contributors.

It's also doing well operating income of around $2 billion and a very solid return on invested capital above 30%. You can't borrow your way out of debt, Ricky. It trades at about 35 times forward earnings. That's about triple the price tag of competitor Expedia. What does that word salad mean to you?

In Europe, we similarly see over 80% of property revenue supported by Telefonica, Orange, Vodafone, and Deutsche Telekom versus less than 60% at the same time in 2018. billion in fixed rate debt through a combination of Euro and U.S. Good updates on the floating rate debt and the leverage. Good morning.

Working closely with our account executives and global systems integrators, their journey started in 2018 with core RPA. To date, they have achieved a return on investment of over $250 million. billion in cash, cash equivalents, and marketable securities and no debt. million hours to date. As of October 31st, we had $1.8

We delivered earnings of almost $8 billion, two times higher than what we earned in the second quarter of 2018 under comparable industry commodity prices. First, our work to structurally improve earnings power is paying off, demonstrated this quarter as we doubled earnings versus a comparable price environment in the second quarter of 2018.

First, as I have gone deeper into the operational side of the business, I am committed to continuing to sharpen our focus on operational rigor while learning into areas where the return on investment is the strongest. billion in cash, cash equivalents and marketable securities and no debt. We hope to see many of you there.

In addition to this, our team has been closely analyzing recent restaurant openings to identify key success factors and maximize our return on investment. And as such, we will return to building our new restaurant pipeline with more restaurants to come in 2026. We ended the fourth quarter with net debt of $40.4

Most of the increase relates to product produced before 2018. During the quarter, we completed our inaugural investment-grade public senior notes offering by issuing long five-year bonds. This brings our mix of variable to fixed rate debt to 68% fixed and 32% variable. We repurchased 1.6 I think the rest of the pieces play out.

Additionally, since 2018, we have invested over $3.5 Since 2018, we have added over 10,000 new department supervisors and over 2,500 new assistant store managers. Capital expenditures totaled $620 million in Q4 as we continue to invest in strategic initiatives to drive growth and profitability.

We took the company public with an amazing shareholder base, and we finished the year with a very strong balance sheet, including $168 million of cash and short-term investments with zero debt. Our asset light model and strong returns on capital once again supported very strong cash generation. It was launched in 2018, I think.

per cent return in the first six months of 2023, outpacing the benchmark of 3.2 per cent, with the help of recovering bond markets as interest rates rose and additional contributions from corporate credit and emerging country sovereign debt. per cent return in the first six months of the year compared to the benchmark of -2.1

At the end of the quarter, we remained in a healthy financial position with a strong balance sheet, including no debt, no drawings on our $75 million revolver, and $58 million in cash. We are a growth company and we will return to industry standard return on investment new store growth. Now turning to the balance sheet.

The challenges we have faced since 2018 have made planning difficult, so smoothing out fluctuations is a must, and the best way to do that is with smooth and predictable capacity growth. airline with an investment-grade rating by all three rating agencies. We ended second quarter with cash and short-term investments of $12.2

Third, we're intensifying our focus on financial discipline and shareholder returns. We're implementing a rigorous capital allocation framework centered on free cash flow generation and return on investment metrics with clear hurdle rates. The review process is ongoing, and an update will be provided later this year.

per-cent return on investments in 2023 as stocks soared but missed its internal benchmark by about one percentage point as real estate assets struggled. On Credit and specifically private debt, here's what Michael notes: We put private credit in our policy portfolio in 2023. per cent and 15.9

Carnival 's plans to pay off its heavy debt load. The company's really struggling to pay off a lot of debt. Most of their debt, fixed debt also good, so it's not subject to crazy interest rates. But with a company like this and with companies that carry heavy debt, how should we think about this? Higher is better.

Another thing and this might be fairly Canada focused, but I know it's happening a lot more in your fine country is, you may have heard that cannabis was legalized in Canada across Canada in 2018. What it might be going on here is a bit of investment. When we look at the stock though it's a different story.

Systems built 20 years ago to power digital advertising, including third-party cookies are losing effectiveness and ineffective ad spending is creating more opportunities for those who use first-party data to connect the right content to the right customers while clearly measuring return on investment. Turning to health and wellness.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content