This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The company claimed it could deliver a compound annual growth rate (CAGR) of 40%, taking revenue from $140 million in 2020 to $388 million in 2023 while expanding its gross margin from 30% to 50% and keeping its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margins in the high teens. on April 6, 2022.

A key inflection point took place in 2021. In the years leading up to 2021 discretionary cash flow per unit was negative. In 2021, it turned positive. In 2021, it was positive $0.43 The distribution was increased just modestly in 2020 and 2021. The numbers are fairly large, as well. per unit in 2020.

Shares skyrocketed 530% from their March 2020 low to their all-time high in July 2021, driven by monster success fueled by consumers spending more time at home. Revenue jumped more than 55% in both 2020 and 2021. This tells me that the content publishers have the negotiating leverage. Investors need to be aware of these risks.

in late 2021. With a recovery in sight, is it possible for Sea to reach its 2021 highs ever again? billion in the third quarter of 2021 to a trough of just $443 million in the second quarter of 2023. To be sure, Garena's adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) is down from $2.8

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. Looking back at Carnival's slowdown and recovery In fiscal 2020 and fiscal 2021 (which ended in November 2021), Carnival's revenue and number of passengers plummeted.

The chart below shows how each company raised full-year guidance on every earnings call since 2021 and beat the third-quarter guidance in the full-year results in 2021 and 2022. billion at the start of 2021 and still stands at just $8.9 For reference, I've taken the midpoint of the guidance ranges to simplify matters.

From its initial public offering in April 2017 to its all-time high in August 2021, the stock skyrocketed an eye-watering 3,230%. After revenue growth decelerated slightly at the onset of the pandemic, Carvana saw its sales surge throughout 2021. Investors would struggle to find a return like this elsewhere in the market.

ChargePoint (NYSE: CHPT) became the world's first publicly traded electric vehicle (EV) charging network company after it merged with a special purpose acquisition company (SPAC) on March 1, 2021. That stock offering won't increase its leverage, but it will cause significant dilution for a company with an enterprise value of only $1.4

For Berkshire, that meant its position in Apple grew from 5.39% in 2020 to 5.55% in 2021 without purchasing a single share. For comparison, Kroger's net leverage ratio at the end of its fiscal first quarter 2023 was a much-healthier 1.3 at the end of its first quarter of 2023. times EBITDA. times EBITDA.

But Chewy shares are now down 74% from their early 2021 peak, unable to live up to the once-incredible hype. billion on their "fur babies" last year, up nearly 11% from 2021's tally. It's been a tough past couple of years for Chewy (NYSE: CHWY) shareholders. Investors are throwing in the towel. Image source: Getty Images. billon is 13.6%

The Trade Desk (NASDAQ: TTD) has been at the forefront in leveraging this opportunity by programmatically matching buyers and sellers of advertisements on the CTV (connected television, a device or software used to support video content streaming) platform. However, things may now be on the verge of improvement.

The company has been leveraging the power of contextual artificial intelligence (AI) to effectively target audiences by running appropriate advertisements that match the content shown on the Roku Channel. TV households had at least one internet-connected television (CTV) device in 2022, up from 82% in 2021. billion in 2024.

billion in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and $1.2 It's telling that revenue declined in 2023, and not 2020 or 2021. Sirius XM is also starting to pay down its long-term debt since that bearish leverage peaked in 2022. It has posted an annual profit every year since 2010.

Buffett also served as a trustee until 2021. It's leveraging its AI investments to grow two businesses at scale. The stock currently trades at an enterprise value-to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple above 17. Gates isn't alone in his pledge to give away his wealth.

Battling a trio of challenges, including weaker consumer confidence, less snowfall at its North American ski resorts, and tough comparables after a post-COVID resurgence, Vail Resorts (NYSE: MTN) has seen its shares decline 50% since 2021. Image source: Getty Images.

The logistics services provider has come a long way since it was spun off from XPO in 2021. billion in adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). GXO Logistics (NYSE: GXO) just marked two full years as a publicly traded company. Image source: GXO Logistics. billion, edging out estimates at $2.38

Those include its third-party marketplace, digital payments business, lending business, and its fast-growing advertising business, which leverages the company's position at the bottom of the marketing funnel, making it attractive to the businesses that sell on the platform.

Looking ahead, management also gave new long-term guidance, calling for adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) per available passenger berth day (ALBD/APBD) to increase by 50% by 2026, reaching its highest level in almost two decades.

Block faced rising scrutiny for these increasing costs, and as a result, its stock dropped 87% from its peak price of $289 per share in August 2021 to October 2023. Block has reorganized its Square team and is taking steps to leverage artificial intelligence (AI) to help sellers manage more of their business and grow their customer base.

This ratio measures a company's financial leverage. The company has maintained excellent double-digit revenue growth since it went public in March 2021, as seen in the chart below. Why the stock scares off some investors The debt-to-equity (D/E) ratio of DigitalOcean is a negative 675% due to total debt of $1.47

OIBDA = operating income before depreciation and amortization. And it's not just the market saying so (though it is, as reflected in the stock's steady decline since early 2021). The only unit that can be counted on for profits is the TV media arm. Data source: Paramount Global. Chart by author. Figures in millions.

The company went public on March 11, 2021, at $35 per share and closed at an all-time high of about $50 later that month. Revenue jumped by 90% in 2020, and by 54% in 2021. billion in 2021. billion in 2021 to $92 million in 2022. in 2021 to 4.4% As its revenue rose, losses expanded sharply, too. billion net profit.

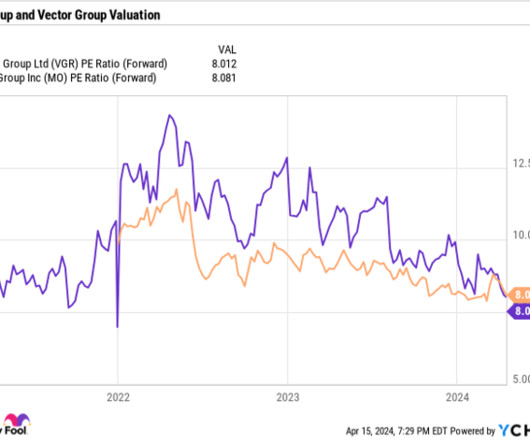

The other important aspect to look at when it comes to the safety of a company's dividend is its leverage, which is its net debt divided by its earnings before interest, taxes, depreciation, and amortization (EBITDA). Altria ended 2023 with leverage of 2.2 Looking at its balance sheet, Vector ended 2023 with leverage of 2.6

million and marked its fastest revenue growth since 2021, as demand is accelerating after a post-pandemic slowdown. It also gained leverage on selling, general, and administrative expenses, and adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) rose from $17.8 million to $22.4

billion in total earnings for the Guild's 5,951 screenwriters in 2021. billion in production fees for 319,000 members in the first four months of 2021. It seems like the actors and writers have plenty of leverage in these negotiations. The WGA (West) reported $1.55 Warner Bros.

In 2024, we set ambitious goals for ourselves, and we're proud to report that our team delivered, punctuated by a strong Q4, our highest revenue growth quarter since 2021. In 2025, we plan to leverage and enhance data-driven media mix model to make real-time optimizations. On a full-year basis, revenue was $771.3 million, up 15.2%

Its revenue plunged 73% in fiscal 2020 and declined 66% in fiscal 2021. That rising leverage made Carnival a risky stock to hold as interest rates rose, and its stock sank to a 30-year low of $6.38 Carnival's core business is recovering The pandemic severely disrupted Carnival's growth in fiscal 2020 and fiscal 2021.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017. billion to $3.75

These capital market levers allow us to deploy intelligent leverage to increase our Bitcoin holdings in a manner which we believe has created shareholder value. Leverage provides the opportunity to generate higher returns if the price increases. billion in current market value, which are held at MacroStrategy.

If that prediction holds true, and considering Unity is already comfortably free-cash-flow-positive (free cash flow was $104 million last quarter), it should be poised to enjoy significant additional operating leverage as it scales.

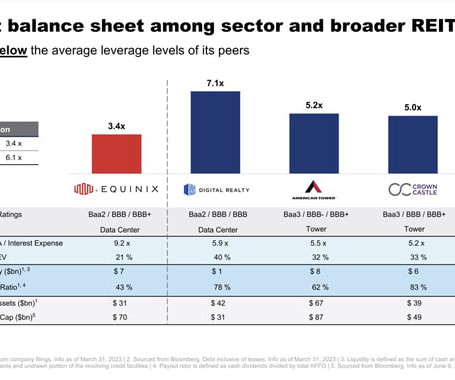

Meanwhile, many data infrastructure REITs allowed their leverage ratios to rise to relatively high levels. EBITDA = earnings before interest, taxes, depreciation, and amortization. As the slide shows, it has much lower leverage ratios than its peers. Meanwhile, its lower leverage ratio gives it more borrowing capacity.

Metric 2020 2021 2022 Bank partner loans growth 40% 338% (5%) Conversion rate 15% 24% 14% Contribution margin 46% 50% 49% Revenue growth 42% 264% (1%) Adjusted EBITDA margin 13% 27% 4% Data source: Upstart. at the end of 2021 to 2.15 Those transfers didn't happen as planned and, as a result, its debt-to-equity ratio jumped from 1.26

leveraging its talent across brands to help share unique learnings and experiences. This second phase will focus on maximizing the value creation potential of our platforms through the acceleration of AI capabilities in combination with fully leveraging the immense data assets we now own. Consumer Data Insights system.

However, the company said excluding Safelink, which catered to this program, it added 80,000 prepaid customers, its first quarter of net additions since acquiring TracFone in 2021. Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) rose 2.5% Wireless equipment revenue, meanwhile, sank 8.1% billion to $18.5

As you can see from the chart below, both revenue and adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) have risen solidly since then. will give GXO an opportunity to leverage its expertise and expand into industrial verticals across Europe. and gaining Wincanton's assets and customer base in the U.K.

2021, and increased 13% in fiscal 2021; yet, only grew 2% in fiscal 2022 as its post-pandemic slowdown was exacerbated by inflation, higher freight costs, and supply chain disruptions. 2021) and rose 24% in fiscal 2021 as pet owners bought more products online during the pandemic.

Shares of the online home-furnishings leader plunged in 2022 and have been down for the count since then as revenue growth has been negative almost every quarter since mid-2021. It also launched a new rewards program that costs $29 a year, hoping to leverage the same dynamics that have made Amazon Prime so successful.

Revenue in Q1 2024 (ended March 31) was up 19% year over year and 54% higher than in the first quarter of 2021. The company was able to post positive adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) and free cash flow in three straight quarters, a streak that's still active. These are positive trends.

GXO Logistics (NYSE: GXO) was created in 2021 in a spinoff from XPO with a simple value proposition for investors. However, its PFS Operations' adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) were $23.2 In 2022, PFSweb's revenue rose 6.4% What's next for GXO?

The stock had soared to a sky-high valuation in early 2021 with the help of a short squeeze , but that proved to be unsustainable. Shares are now down 84% from their peak in early 2021. If Appian can leverage its AI products into meaningful revenue growth, the upside potential for the stock looks significant.

The company has also leveraged the strength of core businesses like e-commerce to add on higher-margin businesses like advertising, consumer financing, its third-party marketplace, and digital payments. That explains why its operating margin reached a record of 18.2% in the third quarter. million in EBITDA, compared to a loss of $3.7

The company is nearly two years old now, spun off from XPO Logistics in August 2021 to streamline both businesses so the market could value them accordingly, rather than as a combined conglomerate. The company expects to generate $17 billion in revenue, or a compound annual growth rate (CAGR) of 8% to 12% from 2021 to 2027.

ServiceNow (NYSE: NOW) and AppLovin (NASDAQ: APP) are both high-growth tech companies that leverage artificial intelligence (AI) to simplify tasks for companies. AppLovin is overcoming its macro headwinds AppLovin's revenue surged 92% in 2021. If it maintains that momentum, it could generate even bigger multibagger gains in the future.

Another positive sign for investors is that Celsius continues to leverage costs to grow profits at high rates. Chewy's annual sales growth decelerated from 25% in fiscal 2021 to just 7% over the last year. Celsius is seeing green shoots in e-commerce, where sales through Amazon were up 41% year over year, making Celsius the No.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content