This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Delta Air Lines 2022 2023 Long-Term Target Return on invested capital 8.40% 13.40% Mid-teens Weighted average cost of capital 8% 8% 8% Data source: Delta Air Lines. I've also included its adjusted debt to earnings before interest, taxation, depreciation, amortization, and rent ( EBITDAR ) multiple.

The launch of OpenAI's ChatGPT in November 2022 has put the spotlight on the huge investment potential of artificial intelligence (AI). In fact, according to Ark Investment Management's Big Ideas 2023 report, AI software will rake in revenue of up to $14 trillion in 2030. billion in 2022.

Rocking the boat Royal Caribbean unveiled its Trifecta performance program in late 2022, which outlined three financial goals it was hoping to achieve by 2025. in return on invested capital. The three Trifecta goals seemed ambitious at the time with the industry recovery far from certain.

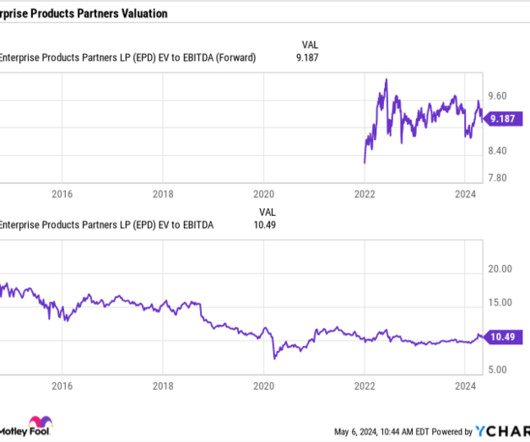

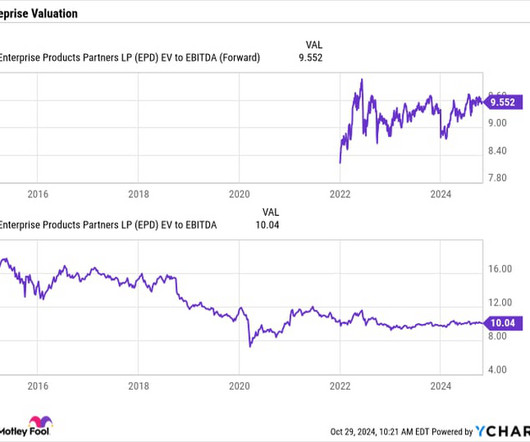

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, rose 6% to nearly $2.5 billion in 2022. Enterprise has averaged about a 13% return on invested capital over the past five years. It generated distributable cash flow of $1.9 cents per unit. billion on growth projects.

In the fourth quarter, Broadcom reported a 65% margin based on adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). After a lull during the 2022 bear market, there are signs that digital ad spending is starting to spring back to life.

After a disappointing year for stocks in 2022, the markets have rebounded this year. It reported a better-than-expected adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) profit of $681 million, though it's still losing money on a generally accepted accounting principles ( GAAP ) basis. billion-$4.25

From 2014 to 2019, Paycom's annual revenue grew at a compound annual growth rate (CAGR) of 37% while its adjusted earnings before taxes, depreciation, and amortization ( EBITDA ) rose at a CAGR of 64%. Its revenue then increased 25% in 2021 and 30% in 2022 as the pandemic passed. Why did the bulls love Paycom?

Its revenue rose 14% in 2020, even as the pandemic curbed the market's demand for its services, but grew 25% in 2021 and 30% in 2022 as those headwinds dissipated. Paycom's adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margin rose from 39.3% in 2020 to 42.2%

Generating positive free cash flow (FCF) every year since the turn of the century, the stock has delivered total returns of 3,600% over that time -- or seven times the S&P 500 index's return. is down 40% from its high. Here's why this drop could be a once-in-a-decade opportunity for investors. percentage points.

Let's see why Workday held up so much better than Paycom -- and if it will remain the better HCM investment for 2024. Paycom faces severe cannibalization issues Paycom's revenue rose 25% in 2021 and 30% in 2022. Image source: Getty Images. However, it expects its revenue to rise just 22% in 2023 and 10% to 12% in 2024.

per share, driven by a two-percentage-point jump in its adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) margin to 39%. That's way higher than its price-to-sales ratio of 15 at the end of 2022. It is worth noting that The Trade Desk finished 2022 with a 32% jump in revenue to $1.58

Snap continues to focus on innovation Snap generated basically zero revenue growth in 2023 compared to 2022. The company says online jewelry retailer James Allen recently saw an 18% drop in cost per action (CPA) and a 67% increase in its return on investment thanks to the new Pixel model. Image source: Getty Images.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, climbed 10% to nearly $2.4 billion in 2022. Over the past five years, Enterprise has averaged about a 13% return on invested capital, so these growth projects should provide meaningful growth to the company in the years ahead.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) also rose 5% to nearly $2.44 billion spending in 2022. It noted that it has produced about a 12% return on invested capital over the past decade. This stayed true last quarter, as the company delivered solid growth. billion to $3.75

Shares of the visual-centric social media platform operator have stagnated since mid-2022, but may soon start posting impressive gains. The company also dramatically improved its adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) margin by 14 percentage points to 37% in the quarter.

The fourth quarter comes in ahead of plan Earlier this year, Carnival CEO Josh Weinstein unveiled a new three-year plan called SEA Change, which stands for Sustainability, EBITDA per available lower berth day (ALBD), and Adjusted return on invested capital (ROIC). Comparing apples to apples, net losses improved by about $1.55

Up 17% so far in 2023 on a total return basis, the S&P 500 is well on its way to posting a solid rebound year after struggling in 2022. With total returns of -15%, -4%, and 10% this year, American Tower (NYSE: AMT) , Canadian National Railway (NYSE: CNI) , and Casey's General Stores (NASDAQ: CASY) have lagged the index.

The company signed a first-of-its-kind carbon dioxide transportation agreement with ExxonMobil in 2022. The company estimates it could generate an additional $300 million of annual adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) from this business in the coming years.

We are working to pivot our business toward a model that will streamline our operations and sell nonstrategic assets, improve the consistency of our earnings, increase EBITDA and dividends per share, reduce debt, rightsize the balance sheet, and improve the return on invested capital. million during the same period of fiscal year 2022.

This resulted in higher realized iron ore premiums, but more importantly, higher margins and returns on invested capital. per ton, the lowest level since 2022. This is the lowest C1 cash cost since the first quarter of 2022. They should rather be treated as a type of debt amortization. per ton in the quarter.

Nexxen has built and developed an incredibly advanced tech and data stack that not only helps customers navigate these challenges but also enables them to drive enhanced return on investment and reach their target audiences regardless of where they consume content. million, reflecting a 12% decrease from Q4 2022.

with one less selling day in 2023 as compared to 2022. The decrease in GAAP gross profit was driven by the impacts of the NuVasive merger, namely step-up inventory amortization. Adjusted gross profit, which excludes the impacts of inventory step-up amortization, was 65.5%. on an as-reported and constant currency basis.

First, in 2022, we had $20 million of revenue shift from the third quarter into the fourth quarter due to the fire at our primary contract manufacturer in June of 2022. Non-GAAP operating margin was 15% in Q3, below Q3 of 2022, due primarily to our investment in emerging customers. Reported earnings were $0.11

As a result, we recorded accelerated amortization to fully amortize the remaining trade name intangible asset. The effect of this change in estimate for the third quarter was an increase in sales and marketing amortization expense of $10.1 million as of October 31st, 2022, with $627.6 million as of October 31st, 2022.

We will also offer some perspective on our strengthened balance sheet position with the recent divestiture of one of our noncore businesses, which underscores our focused product strategy and our commitment to driving a strong return on invested capital. million in the fourth quarter of 2022. million in Q4 of 2022.

The growth was primarily driven by a larger base of operating studios, which contribute to a higher number of franchise license revenue being amortized in addition to higher royalties generated by the increase in systemwide sales and positive same-store sales growth. Inventory levels have now reached their lowest levels since 2022.

Excluding amortization, adjusted gross margin was 57.5%. It's important to consider a strong performance in the back half of 2022 as we improve service level over that period. The higher rate versus prior year is primarily driven by jurisdictional mix of earnings and less favorable discrete benefits in 2023 as compared to 2022.

These required significant investment and the markets have not seen the growth in profitability we had expected over the past several years. We see an opportunity to shift these resources toward strategic areas that have a higher potential return on investment, and we continue to drive toward our goal. No material changes there.

During the call, Jim, John, and Devina will discuss operating EBITDA, which is income from operations before depreciation and amortization. This is paid off in the form of lower repair and maintenance costs in both dollars and as a percentage of revenue compared to 2022. billion from 2022 through 2026. billion and $2.9

While we aggressively pursue growth opportunities, the company will remain focused on its three long-standing, long-term financial tenants, those being to maximize free cash flow, maximize return on invested capital, and returning excess free cash to our shareholders. Depreciation and amortization for the quarter was 3.9

In Q2, we released our 2022 Impact Report, highlighting our commitment to our values and our progress toward achieving our science-based targets and other sustainability goals. As these costs are now fully amortized, Q2 will be the last quarter we report on these headwinds. Total inventory was down 15.7% versus last year.

One important component of this strategy is innovation to solve customers' most pressing needs, aligned with market growth trends, and generate a strong return on investment. we achieved in fiscal 2022. First, we maintained a sharp focus on accelerating profitable growth.

Non-GAAP adjusted EPS is defined as adjusted net income or loss, which excludes the amortization of intangible assets, acquisition-related costs, estimated loss related to underperforming assets of subsidiary, changes in fair value related to consideration payable and onetime nonrecurring expenses divided by the weighted average shares outstanding.

Non-GAAP gross margin, excluding amortization of acquired intangibles, was 73%. We expect gross margins will improve over time as we realize the benefits from lab automation, leverage investments in a lab infrastructure, and see an increased mix of rescreened patients. And we're eating it up less than the 2022 spend.

Non-GAAP gross margin, excluding amortization of acquired intangibles, was 73%. Back in June, we guided to total company revenue growth of 15% about from the period of 2022 through 2027. We're highly focused on continuing to grow Cologuard, investing in Cologuard and Cologuard growth, and Oncotype DX growth internationally.

As of December 31, 2022, our contracted backlog totaled 61.4 Our third-quarter operating income was $273 million, which included depreciation and amortization and accretion of $78 million, round cost of $25 million, production stage expense of $12 million, and share-based compensation expense of $8 million. Moving on Slide 5.

See the 10 stocks *Stock Advisor returns as of July 17, 2023 Reconciliations between the two can be found in today's press release. Please note that when we discuss all of our expense figures, they will exclude stock-based compensation and related payroll taxes, as well as depreciation and amortization, and nonrecurring charges.

billion, up 6% compared to the fourth quarter of 2022. Our 2023 mark-to-market adjusted EPS also included significantly less pension income compared to 2022. This result was near the high end of our guidance range and represented free cash flow growth of 30% compared to 2022. In total, net pension costs generated a $4.07

For decades prior to the pandemic and since late 2022, we have been a consistent share winner through our unmatched expertise across marketing, merchandising, supply chain, and technology. We've been doing that since the fourth quarter of 2022. What is much more predictable is our own ability to outperform the competition.

During the call, Jim, John, and Devina will discuss operating EBITDA, which is income from operations before depreciation and amortization. We've automated more than 800 routes in our residential fleet since 2022, reducing our labor dependence, boosting efficiency, and improving safety performance.

While exiting this relationship in 2022 was a difficult decision, we are pleased to renew this relationship under a fair and more equitable contract, which enables us to operate on a sustainable basis and keep prices low for customers. Health and Wellness was also a strong driver of sales this year, led by growth in GLP-1s.

During the call, Jim, John, and Devina will discuss operating EBITDA, which is income from operations before depreciation and amortization. We also continue to execute well on sustainability, our sustainability growth investments. Any comparisons, unless otherwise stated, will be with the prior year.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content