This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Highly profitable, but watch debt levels Portillo's is not only a high-volume restaurant concept but also highly profitable. With minimal cash on the balance sheet and over $600 million in debt and tax receivable liabilities with its old private equity owners, the stock has an enterprisevalue of approximately $1.5

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. billion in long-term debt, but that figure hit a whopping $29.5 billion in long-term debt, but that figure hit a whopping $29.5 NYSE: CCL).

MicroStrategy's Bitcoin holdings now account for 30% of its enterprisevalue of $46.9 That rally would boost the value of its current Bitcoin holdings to $2.94 That's 35% of its enterprisevalue of $4.83 It ended its latest quarter with a seemingly low debt-to-equity ratio of 0.1,

For example, in the first quarter of 2024, its car wash division accounted for 25% of revenue, but revenue in this segment was down about 8% year over year. Driven Brands has an enterprisevalue of $5 billion (for the record, this is technically a mid-cap stock, not a small-cap stock). Driven Brands has $2.9

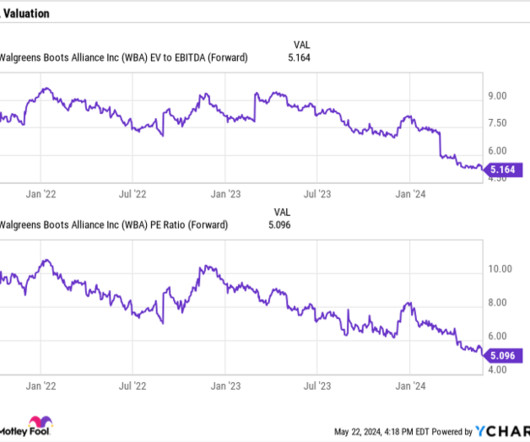

billion in net debt, not including operating leases, an ill-advised investment was not a good use of cash. At a forward price-to-earnings (P/E) ratio of about 5 and enterprisevalue (EV)- to-EBITDA ratio of 5, Walgreens stock is inexpensive. The latter metric takes into account its net debt and takes out non-cash items.

First, the company's enterprise-grade Zoom Phone product has quickly grown to account for more than 10% of overall sales. Building on this success, Zoom's 215,000 enterprise customers now account for 57% of its revenue and have spearheaded the company's shift to a more comprehensive communications platform.

billion and a market value of $24.5 MicroStrategy's Bitcoin portfolio is equal to about a third of the company's enterprisevalue of $73.3 From 2023 to 2026, analysts expect its revenue to only grow at a compound annual rate of 1% as it stays unprofitable on a generally accepted accounting principles ( GAAP ) basis.

With so much cash pouring in, the company's balance sheet is rock-solid: over $58 billion in cash and equivalents with only $38 billion in debt, for a net cash position of about $20 billion. billion in cash and no debt, and it is profitable under generally accepted accounting principles ( GAAP) over the past few quarters.

That marked the first time its total cash and BTC holdings exceeded its total debt. Marathon's revenues are soaring, but it isn't consistently profitable on a generally accepted accounting principles ( GAAP ) basis, and it's taking on a lot of debt to expand its mining operations. With an enterprisevalue of $6.1

The dot-com crash and some accounting problems from 2018 to 2020 exacerbated its decline. But with its stock trading at about $2, Plug Power's enterprisevalue of $2.6 billion values the company at just two times next year's estimated sales. That deal could help it tread water and avoid taking on too much debt.

billion -- which is more than half of its enterprisevalue of $25.3 The company is also taking on more debt to fund its Bitcoin purchases, and analysts expect it to turn unprofitable again on a generally accepted accounting principles ( GAAP ) basis this year as it racks up more impairment costs from its Bitcoin buys.

However, at the end of the second quarter, the value of the average funded account on Robinhood Markets was only $5,773, so smaller retail investors are still scooping up a lot of stocks. That's 37% of the company's enterprisevalue of $37.2 As of July 31, MicroStrategy held a whopping 226,500 Bitcoins.

And if you weigh the companies by the accountingvalue of assets such as theme parks and giant digital spheres, Sphere Entertainment's enterprisevalue to assets (EV/A) lands at 0.4. billion in long-term debt is due for repayment in the next year. Its price to sales (P/S) ratio stands at 1.7, EV/A ratio.

But based on those expectations and its enterprisevalue of $2.2 It's also unprofitable on a generally accepted accounting principles ( GAAP ) basis, and it doesn't even expect its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) to turn positive until 2025. Its high debt-to-equity ratio of 4.3

This is important for investors because it allows the company to pay out its distribution while still being able to pay down debt. When Energy Transfer cut its distribution in 2020, it was because its leverage became too high, and it needed to pay down debt. cents is now higher than the 30.5 cents it was before the distribution cut.

commercial revenue soar 70% for the quarter, now accounting for more than one-fifth of its top-line results. billion market cap, with an enterprisevalue that shrinks to $1.5 billion once you factor in its cash-rich and debt-light balance sheet. It saw its U.S. Guidance was also encouraging.

It also abandoned its original goal of achieving profitability on a non-GAAP ( generally accepted accounting principles ) basis in fiscal 2024 as it ramped up its research and development spending as well as marketing budgets for new generative AI applications. With an enterprisevalue of $3.1 What will happen to C3.ai

per share under generally accepted accounting principles ( GAAP ), and sales of only $193.1 billion in net debt, that works out to an enterprisevalue -to-free cash flow ratio of about 22.8 Analysts had forecast Iridium would earn $0.04 per share (pro forma) on sales of $198.4 million for the quarter. on the stock.

But its high debt-to-equity ratio of 2.9, steep losses on a generally accepted accounting principles ( GAAP ) basis, and overwhelming dependence on the housing market will keep the bulls at bay in this high interest rate environment. With an enterprisevalue of $3.5 Where will Opendoor's stock be in a year?

But it still racked up a net loss of $205 million in the first half of fiscal 2024 on a generally accepted accounting principles ( GAAP ) basis. However, its high debt-to-equity ratio of 2.9 That stock offering won't increase its leverage, but it will cause significant dilution for a company with an enterprisevalue of only $1.4

Thinning margins and high levels of debt Management brags about Sirius XM's subscriber churn, which stood at just 1.5% And this doesn't include expenses from Sirius XM's huge debt load, which stands at around $9 billion. Add back its $9 billion in debt and you have an enterprisevalue of $18 billion.

Those two businesses generate billions in revenue just by making sure money moves from one account to another. billion last quarter, up 4% year over year, accounting for more than half of total revenue. As its own network operator, American Express gets to keep all of those swipe fees. They amounted to $8.8

That might seem odd because Honeywell raised the midpoint of its full-year sales and earnings guidance on account of raising the low end of their ranges. That said, alongside Apple and Rockwell, it's hard to argue that Honeywell is an outstanding value stock. HON data by YCharts. Data source: Honeywell presentations.

With an enterprisevalue of $50 billion, Atlassian doesn't seem cheap at 13 times this year's sales. Investors should also recall that Atlassian is still unprofitable on the basis of generally accepted accounting principles ( GAAP ) and has an alarmingly high debt-to-equity ratio of 5.3.

The company will remain unprofitable on a generally accepted accounting principles ( GAAP ) basis, but it's still shouldering $194 million in long-term debt while holding just $33 million in cash and equivalents on its balance sheet at the end of 2023. Analysts expect revenue to rise 31% in 2024 only for it slow to 13% in 2025.

The macro situation has improved in calendar year 2024, so the company's net-dollar expansion rate for fiscal 2025 should give a clearer picture of how much enterprisesvalue Zoom's offerings. Income from operations under generally accepted accounting principles ( GAAP ) was $168.5 Adjusted operating income grew 9.6%

billion, which equals roughly a quarter of MicroStrategy's enterprisevalue of $30 billion. Its subscription revenue rose 33% year over year in 2023, but the business only accounted for 16% of its top line and couldn't offset its declining product license and support revenue. As a result, its revenue fell 1% for the full year.

It also turned unprofitable in both years and took on more debt to stay solvent. Carnival stayed unprofitable on a generally accepted accounting principles ( GAAP ) basis in fiscal 2022 and 2023, but it narrowed its losses in both years. With an enterprisevalue of $46.6 per share on Oct. billion for the full year.

Ginkgo stock has been trading at a steeply negative enterprisevalue. It's a debt-free company that finished June with $730 million in cash and cash equivalents. Then again, stocks generally don't trade at negative enterprisevalues unless investors have a good reason to expect steep losses. A bargain now?

It took some of that cash and bought back about $150 million in debt. Without reducing debt any further, the company is on track to get to 3 times leverage (net debt/adjusted EBITDA) by year end. Image source: Getty Images.

That's because while growth and profitability are improving, management of its huge debt load remains an uphill battle. And the company has finally returned to profitability under generally accepted accounting principles ( GAAP ) with $1.07 As of the third quarter, long-term debt stands at $29.5 billion in net income.

million streaming households, up 14% year over year, and these accounts increased their engagement 23% with 30.8 billion in trailing-12-month revenue, but it's still not profitable on a generally accepted accounting principles ( GAAP ) basis. billion in cash against zero debt. As of the first quarter, the company had 81.6

In the third quarter, SG&A accounted for a whopping $97.8 billion in debt against $615 million in cash. So on an enterprisevalue of around $2.3 This is because as the Sphere becomes more of a well-known tourist destination, there may not be as much reason to spend so much on advertising.

Qualcomm's Snapdragon chips account for 31% of the mobile SoC market, according to Counterpoint Research, while MediaTek has a 32% share. The price tag is too high Intel still has an enterprisevalue of $124 billion. It was also shouldering $13 billion in long-term debt with a debt-to-equity ratio of 1.1.

And they paid for this growth with debt, promising to become profitable someday when necessary. For perspective, its enterprisevalue is just $6.2 In recent months, management lowered guidance, the company decreased its dividend, Advance was removed from the S&P 500 , and S&P Global Ratings downgraded its debt.

Fittingly for accountants, it seems love, like taxes, springs eternal. The math was pretty simple: Spin off the consulting practice in search of an eventual $100 billion enterprisevalue on the stock market, enriching partners and freeing both arms from pesky conflict-of-interest rules in the process.

It recently announced it was buying PFSweb for $181 million, or an enterprisevalue of $142 million, which includes the company's cash balance of $39 million. million, with an operating loss of $20 million on the basis of generally accepted accounting principles ( GAAP ). Now, GXO has made another promising deal.

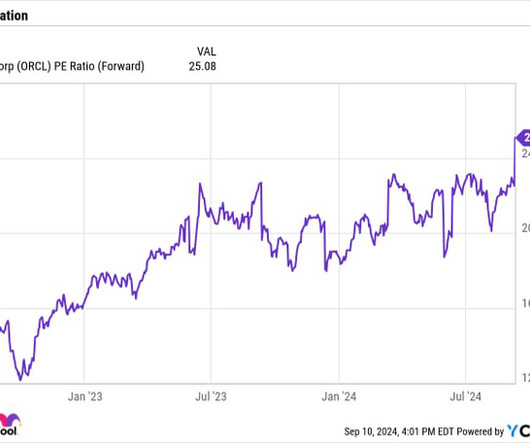

per share, of the improvement came from an accounting change increasing the useful life of its servers and networking equipment assets from five years to six. Unlike many large tech companies, Oracle also carries a lot of debt. Net debt stood at around $73.6 Meanwhile, although its earnings were strong, $157 million, or $0.06

8X8 is boosting its operating cash flow in order to facilitate debt repayments. CEO Sam Wilson certainly spun the debt payments as a positive trend for shareholders. "We With $274 million of long-term debt and $169.5 Unfortunately, I'm not terribly excited about the company's plans for that extra cash. Fair enough, I suppose.

It was also revealed that some deficiencies in DigitalOcean's accounting procedures were discovered. Moreover, the stock is much cheaper on an enterprisevalue basis , as K&S has more than $700 million in cash on its balance sheet and no debt. At $48 per share as of this writing, the stock trades at a paltry 6.8

That's nearly half of MicroStrategy's current enterprisevalue of $9.7 Second, the company's massive impairment costs from those purchases caused it to turn unprofitable on a generally accepted accounting principles ( GAAP ) basis over the past three years. billion in long-term debt and a debt-to-equity ratio of 3.

The macro headwinds also throttled the growth of its enterprise-facing services, while its widening losses and soaring debt forced it to eliminate its dividend last November. That slowdown was exacerbated by the macro headwinds and the divestments of several of its business units to stabilize its margins and debt. respectively.

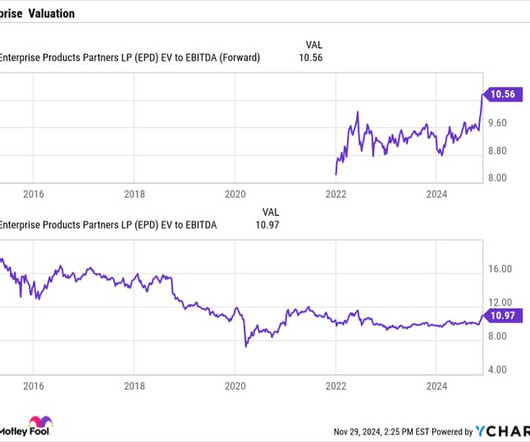

Last quarter, Enterprise Products Partners had a distribution coverage ratio of 1.7. The company's balance sheet also remains in good shape, with net debt (adjusted for equity credit in junior subordinated notes) standing at three times adjusted EBITDA. Its enterprise-value -to-EBITDA (EV/EBITDA) multiple stands at 10.5,

A recent change to the way it reports its annual recurring revenue (ARR) to correct some "historical inaccuracies" raises additional red flags regarding its accounting methods. At its all-time high in late 2021, its enterprisevalue soared to $18.7 At its all-time high in late 2021, its enterprisevalue soared to $18.7

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content