This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Image source: Getty Images Filing taxes isn't always a smooth process. But if you struggled with your tax return in 2023, Mark Steber, Chief Tax Information Officer at Jackson Hewitt , warns, "The upcoming tax-filing season will be yet another complex year." One thing you can do if you haven't already is max out your IRA.

Image source: The Motley Fool/Unsplash Building an emergency fund is a cornerstone of personal finance -- and once you've got that money saved, it's crucial to find the best place to keep it (and no, keeping it in your checking account isn't usually your best move). So what kind of account is best for this crucial cash?

Image source: Getty Images HSAs (health savings accounts) are the unsung hero of personal finances. These accounts allow people with qualifying high-deductible insurance plans to set aside $4,150 for single plans and $8,300 for families out of pre-tax dollars. Once you hit age 55, you can add another $1,000 per year.

Image source: Getty Images Savings account rates have gone up quite a bit over the last two years. Some of the top high-yield savings accounts are currently offering APYs of over 5%, and there's no risk involved. Believe it or not, it's possible to keep too much money in a savings account. That won't last forever, though.

Bonus offer: unlock best-in-class perks with this brokerage account Read more: best online stock brokers for beginners But I also use a regular old brokerage account to save and invest for retirement. Although that account doesn't give me any tax breaks, it allows me to access my money when I want.

With over 60 million people participating in a 401(k) plan, it's the most popular retirement account in the country. An IRA, both traditional and Roth , can be a better retirement account option in many situations. You contribute after-tax dollars to a Roth IRA, but withdrawals are free in retirement if you meet other requirements.

Image source: Getty Images Your trusty savings account is an important piece of your financial puzzle. Unfortunately, many of your fellow Americans are not so fortunate -- research from The Motley Fool Ascent found that just 45% of us can afford a $400 expense with the money in our checking or savings accounts.

Image source: Getty Images Getting a tax refund isn't a given. Some people submit their taxes only to see that they owe money to the IRS rather than the other way around. Read more: we researched free tax software and put together a list of the best options here 1. So don't just stick that refund into savings and call it a day.

Open a retirement account There's a retirement account for everyone. Bonus offer: unlock best-in-class perks with this brokerage account Read more: best online stock brokers for beginners 401(k) If your company offers a 401(k) plan , you're in luck. Your investment funds are withdrawn from your check pre-tax.

Since it's not possible to know what the future holds, fears of a recession shouldn't stop you from making periodic deposits to your investment accounts. As we'll discuss, if you're a long-term investor, the best thing you can do is to continue to invest -- even if the stockmarket tumbles in the short term.

Image source: The Motley Fool/Upsplash As of late February, the average tax refund issued by the IRS this filing season was $3,213. But no matter what refund you get on your taxes , it's important to make the most of that money. Rather than risk that scenario, add your refund to your savings account.

By the time the stockmarket next opens, April will be here. income taxes. Although in most cases, a refund simply represents a repayment of previously overpaid taxes, it still feels nice to get that cash back. That makes it worthy of consideration for folks looking for a place to invest their tax refund windfall.

This rate helps determine important aspects of your everyday financial life, such as the cost of home mortgages and auto loans, the interest rates on credit cards and personal loans, and the annual percentage yield (APY) on your savings account. Keep putting more cash into your savings account until you have a bigger safety net.

Buffett's Q1 buys and sells Given his success, reputation, and willingness to share his wisdom, Buffett's moves are closely followed by investors big and small, and Berkshire reports the stocks it buys and sells each quarter in its 13-F filings. In the first quarter, Berkshire bought three stocks.

Anyone who looks at their 401(k) accounts or investment portfolios knows the stockmarket is sizzling hot. There have been stronger market performances in the past. What does history say the stockmarket will do in 2025? What does history say the stockmarket will do in 2025?

Many people have been forced to prioritize their spending and saving habits, and while some have seen their retirement accounts take a hit due to market fluctuation, others have actually managed to save at record levels. Despite high inflation and a volatile stockmarket, Americans saved and invested more than ever last year.

But for all their benefits, CDs aren't the most advantageous bank account for everyone. The stockmarket could make more financial sense Generally speaking, if you're investing for a future that's still a few decades away, you're going to get better long-term returns from the stockmarket than CDs.

See our expert picks for the best FDIC-insured high-yield savings accounts available today - enjoy peace of mind with competitive rates. That means investing as much as possible and using retirement accounts that offer big tax breaks. Yet millions of American workers don't use one of the best retirement accounts out there.

I'd rather put my money in the stockmarket CDs are a relatively safe investment. They're FDIC-insured, meaning the federal government guarantees your deposit amount, just like a savings or checking account. Despite these benefits of CDs, I'd rather invest my extra cash in the stockmarket using a brokerage account.

The stockmarket is very good at building wealth in the long run. The stockmarket comes with a bewildering number of choices, including several thousand individual stocks and a similar number of exchange-traded funds (ETFs). Tax-efficient moves Uncle Sam will want a share of your gains at some point.

While the variety of CDs on the market ensures that most people can find a deposit requirement they can meet, some investors might find these requirements a barrier to opening an account. If you don't have enough savings to meet minimum requirements, you might be better served by a high-yield savings account.

You don't need an MBA or to work 80 hours a week studying the markets. And in an ironic twist, the less competitive you are, the better you'll be able to stick with a strategy that can lead you to after-tax returns that beat 98% of professionally managed mutual funds. In real life, investors have to pay taxes.

You probably know that an IRA account can help you save for retirement. A traditional IRA gives you an upfront tax break, lowering your taxable income by the amount of your contribution. A Roth IRA saves your tax break for when you withdraw money from the account, potentially decades later.

See our expert picks for the best FDIC-insured high-yield savings accounts available today - enjoy peace of mind with competitive rates. One of the best ways to combat inflation is to keep a portion of investments in the stockmarket, which has historically provided higher returns than bonds or cash.

It is not tied to your employer, is often offered both fee- and commission-free by brokers, and allows tax-free compounding throughout the original owner's life. Of course, stockmarket returns are never guaranteed. Have an investment in a taxable account that gets bought out? Image source: Getty Images. Get a bonus?

Most of us are lucky enough to be able to save for retirement via an IRA account and/or a 401(k) account. IRAs are wonderful, with many benefits, but let's take a closer look at 401(k) accounts, because they may get you to millionairehood faster. These accounts are offered by employers. Image source: Getty Images.

The strategy will produce after-tax returns better than about 98% of actively managed mutual funds over the long run. Here's why it's so hard to consistently beat the market average S&P Global publishes a report called the S&P Indexes Versus Active (SPIVA) Scorecard twice a year. Image source: Getty Images.

Image source: Getty Images High-yield savings accounts (HYSAs) are the best place for your emergency fund. See our expert picks for the best FDIC-insured high-yield savings accounts available today - enjoy peace of mind with competitive rates. Check out our list of the best high-yield savings accounts and start earning more today.

Putting money in savings accounts or CDs is important for any cash you might need in the next couple of years. It carries more risk, because markets can rise or fall and the returns are not predictable. However, historically, stockmarket investments generate higher returns than savings. That's where investing comes in.

Image source: Getty Images If you have a money marketaccount, or are keeping extra cash in money market funds in your brokerage cash management account, you're not alone. Money market funds recently reached a new all-time high of $6.46 There are many good reasons to keep your cash in a money marketaccount.

Have much of your nest egg in stocks The stockmarket is one of the best ways to build wealth over the long run, and just because you're in or near retirement doesn't mean you should shed all your stocks. Your taxable earnings shrink by $7,000, shrinking your tax bill. Earn $80,000 and contribute $7,000?

Roth IRAs have a unique tax break you don't receive from popular accounts like 401(k) or traditional IRAs. They allow you to contribute money that's already been taxed and then take tax-free withdrawals in retirement, as long as you're 59 1/2 years old and made your first contribution at least five years ago.

Don't wait any longer to begin putting your money into the stockmarket. There are a few big reasons why it is important to open a brokerage account and begin investing ASAP. Bonus offer: score up to $600 when you open this brokerage account Read more: best online stock brokers for beginners 1. each month.

And the nice thing about a CD is that your principal deposits are protected provided that you bank at an FDIC-insured institution and you limit your deposit to $250,000 (or $500,000 if there's a joint owner on your account). See, in the long run, the stockmarket is likely to deliver a much higher return on your money than CDs.

There are a few factors that make CDs a compelling investment: The APYs are often better than what you get in a high-yield savings account. If you're saving for retirement and you're willing to forgo a tax break for the current year, you could invest in an S&P 500 ETF using a Roth IRA. CDs vs. S&P 500 ETFs: How does each work?

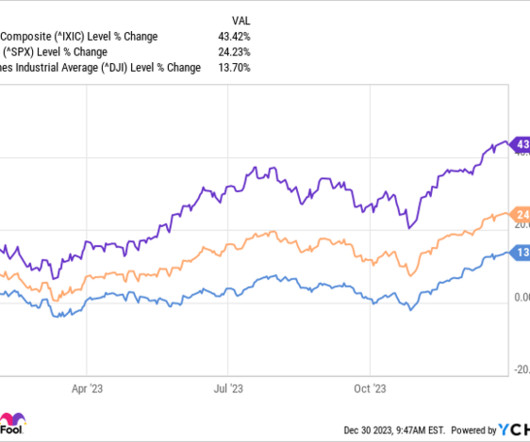

Heading into 2023, the sentiment surrounding the stockmarket wasn't the most positive, as many Wall Street analysts and economists anticipated a potential recession and continued downturn from 2022. Thankfully, that wasn't the case, and the stockmarket had one of its better years in recent times.

stockmarket, recently hit a fresh all-time high. If you don't currently invest in an individual retirement account, or IRA, it might seem like a bad time to start. Isn't investing when the stockmarket is at an all-time high literally the exact opposite? Don't have an IRA yet? New to investing altogether?

Savings accounts Workers are advised to maintain an emergency fund at all times for unplanned expenses, like home or car repairs, as well as for periods of unemployment. For this reason, it's important to keep some of your nest egg in a regular savings account. CD rates tend to be higher than savings account rates.

While 67% of Americans have a retirement account, only 34% believe their retirement savings is on track, according to recent Federal Reserve data gathered by The Motley Fool. Read more: unlock best-in-class perks with one of these brokerage accounts The average U.S. You'll save the most on taxes this way.

Start where you are Before you start dumping money into various accounts, it's important to assess your current financial situation. Here are a few moves to consider: Calculate your net worth : Jot down all your assets, including savings accounts, certificates of deposit, and retirement accounts.

How to start building your retirement savings The best way to get started with your retirement savings is through tax-advantaged accounts. Individual retirement accounts (IRAs) are another option. These are available for almost any individual, and you open them on your own through a stock broker.

Rather, you may be more focused on the balance in your checking account so you can pay your near-term bills. And to that end, it pays to do a few key things: Live below your means Follow a detailed budget Invest in a tax-advantaged retirement account Let's break each action item down.

That is why it's generally a good idea to load your retirement plan with stocks -- either individual companies, if you're comfortable choosing them, or S&P 500 index funds. You might also choose the wrong account in which to save for retirement and forgo tax savings in the process. Image source: Getty Images.

of Americans reported that they had at least some assets in a retirement account, according to the Federal Reserve. While it's good news that just over half of Americans have money in a 401(k) or another retirement plan like an IRA, that also means close to half don't have this type of account to help save for their futures.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content