This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Importantly, this strong performance flows through to our bottom line as we reach an inflection point in our operating leverage earlier than anticipated. We made a strong start into leveraging our existing partnerships with global operators entering the market while expanding ties with local operators seeking additional capabilities.

By and large, this structure has been eliminated, and MLPs are generally in better financial shape as a result, carrying less leverage and being able to grow their business through free cash flow. in enterprise-value- to- EBITDA (earnings before interest, taxes, depreciation, and amortization), the most common way to value these stocks.

The sector has gone through a transformation in the past decade, with midstream companies reducing leverage and being more disciplined when it comes to funding growth projects. Even better, the company has said it could pay excess distributions once its leverage is below 3 times and it has excess free cash flow.

Enbridge currently gets 98% of its earnings before interest, taxes, depreciation, and amortization (EBITDA) from stable cost-of-service or contracted assets. The company currently boasts an investment-grade credit rating backed by a leverage ratio toward the low end of its 4.5-5.0 times target range.

It repaid debt, which steadily drove down its leverage ratio. Today, Energy Transfer has a strong investment-grade balance sheet with a leverage ratio in the lower half of its 4.0-to-4.5x That improving leverage ratio has provided Energy Transfer with increased financial flexibility. The MLP also has a well-balanced asset mix.

Further, its distributable cash flow payout ratio is well within management's target range of 60% to 70% The balance sheet is also healthy: Leverage is well within management's target range of 4.5 to 5 times debt to EBITDA (earnings before interest, taxes, deprecation, and amortization). ENB Dividend Yield data by YCharts.

billion Canadian ($3 billion) of adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) in the period. Fueling that growth was strong utilization across its existing assets, recently completed expansion projects, and the impact of acquisitions. The pipeline and utility operator produced $4.2 target range.

The move will expand Home Depot's addressable market by an estimated $50 billion, but the company said it would suspend share buybacks until it returns to its target-debt leverage of two times earnings before interest, taxes, depreciation, and amortization ( EBITDA ).

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 < Situated in the right basins, MPLX looks in good shape to continue growing its distributions, while its forward enterprise value (EV) -to-EBITDA (earnings before interest, taxes, depreciation, and amortization) valuation of 9.6

That makes logical sense, given that, historically, around 57% of its earnings before interest, taxes, depreciation, and amortization ( EBITDA ) came from oil pipelines, with another 28% from natural gas pipelines. Most of its assets, however, have similar revenue dynamics since they are either regulated, fee-based, or contract-driven.

It operates pipelines, storage assets, a marine business, and export terminals. It also operates crude oil and refined products logistics and storage assets, as well as natural gas G&P operations. billion of adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) and $5.3 billion while DCF was $7.5

A digital collaboration Enbridge recently unveiled a collaboration with Microsoft and will use AI to drive significant advancements in safety, emissions reduction, and asset optimization across its pipeline and utility platforms. That will enhance safety, reduce complexity, and maintain the health of its assets. million-$219.9

That's a concerning number when the company's current assets total less than $10 billion. The company is targeting a gross leverage ratio of 3.0. Gross leverage compares gross to debt to adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ).

Drilling down into the deal Williams has agreed to buy a portfolio of natural gas storage assets from Hartree Partners for nearly $2 billion. The company is paying about 10 times estimated 2024 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) for these assets. billion to $6.8 times in 2018.

These are vital assets, like pipelines and storage, that help move oil, natural gas, and the products into which they get turned around the world. For the most part, the partnership charges fees for the use of its assets, which creates fairly reliable cash flows over time. This is important. Image source: Getty Images.

Thanks to fast portfolio growth and impressive operating leverage, servicing income reached $273 million. during the first quarter, minimizing our amortization expense. Finally, we did an outstanding job generating positive operating leverage, with expenses up only $6 million sequentially, despite our rapid growth.

After its 2022 merger with Kirkland Lake Gold and its acquisition of Yamana's Canadian assets, Agnico has emerged as a leading producer of gold -- and profits. This helps provide the ability to acquire more assets or to advance growth projects that will expand its mineral resources and strengthen the company's future.

This business segment is also enormously profitable, generating 189 billion yuan ($26 billion) in earnings before interest, taxes, and amortization (EBITA) in the fiscal year 2024. With so many valuable assets under its umbrella, Alibaba needs to do just one thing: execute well to unlock the value of these assets.

But it's not bad news for debt providers because they have been rewarded for putting up capital, with their investment backed up by a relatively liquid asset, the airplanes themselves. I've also included its adjusted debt to earnings before interest, taxation, depreciation, amortization, and rent ( EBITDAR ) multiple.

Since our last earnings call on April 30, I am pleased to announce that we are making solid progress on our path forward of one, simplifying the business; two, operational performance improvement and three, reducing leverage. On asset sales, in the second quarter we sold an outparcel deal for $7.1 On to balance sheet matters.

To be sure, Garena's adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) is down from $2.8 This segment is also showing really high operating leverage, with Q4 adjusted EBITDA of $148.5 return on assets last year, even while growing very fast. billion in 2021 to just $921 million in 2023.

These deals are expected to be completed by the end of the year and will increase the Enbridge's exposure to natural gas utilities from 12% of earnings before interest, taxes, depreciation, and amortization (EBITDA) to 22%. That aside, Brookfield Renewable also sells mature assets opportunistically and expects to generate roughly $1.3

The midstream sector of the energy industry While the companies in the midstream space are best known for their pipeline assets, they perform a variety of tasks in the energy complex. Let's take a look at the dynamics of the industry and some stocks in the sector that look poised to outperform over the next several years.

Gates has donated much of his wealth to the foundation over the past 25 years, and he plans to contribute almost the entirety of his assets to charitable causes over the course of his life. It's leveraging its AI investments to grow two businesses at scale. Gates isn't alone in his pledge to give away his wealth. as of this writing.

As we have demonstrated many times before, we expect to generate leverage on these investments as we scale and OG&A will decline over time as a percentage of revenue. We are exploring strategies to reduce the capital intensity of our real estate operations while also maintaining operational control over these strategic assets.

Two additional key performance indicators that management will be discussing on this call are net asset value or NAV and return on equity or ROE. NAV is defined as total assets minus total liabilities and is also reported on a per-share basis. We've also continued to produce favorable results in our asset management business.

Management plans to divest non-core assets to accelerate the paydown of that debt. Shares currently trade for an enterprise value/earnings before interest, taxes, depreciation, and amortization (EV/ EBITDA ) multiple of just 5x. Occidental's big investments in the Permian Basin have put pressure on its balance sheet.

It locks in the spreads with hedges and then uses leverage to increase its returns. The BDC typically likes to invest in companies with revenue between $10 million to $150 million and EBITDA (earnings before interest, taxes, depreciation, and amortization) between $3 million to $20 million. Image source: Getty Images.

Kinder Morgan continues to deliver Over the last few years, Kinder Morgan has posted solid results and made multiple small- to medium-sized acquisitions in legacy oil and gas infrastructure assets, liquefied natural gas (LNG), and renewable natural gas (RNG). LNG is natural gas that is cooled and condensed so that it can be shipped overseas.

The brand is set to launch and begin delivery in April, leveraging NIO's [Inaudible] network for rapid market expansion. billion RMB, primarily due to the loss from the revaluation of overseas RMB-related assets caused by the depreciation of RMB against the U.S. Interest and investment loss was 0.2 billion in 2023 Q4 and 0.3

He wrote, "[We] believe [The Trade Desk] could rapidly scale its [operating system] ambitions via Roku's 85 million+ global streaming household footprint, while Roku could quickly leverage its first-party viewer data and expanding CTV inventory to match with growing advertiser demand." What does this mean for investors?

Selling debt increases leverage, adds to operating expenses (specifically interest expense), and can lead to credit downgrades. But the stream only ate up 23% of the earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of the mine. Selling stock dilutes shareholders and can lead to stock price weakness.

This ratio measures a company's financial leverage. When a company shows a negative D/E ratio, its liabilities exceed its assets -- a sign of potential problems. Why the stock scares off some investors The debt-to-equity (D/E) ratio of DigitalOcean is a negative 675% due to total debt of $1.47

In addition to the opportunity to increase sales and ultimately realize further growth in the pOpshelf banner, we are also able to leverage learnings from this banner and apply them in our non-consumable categories in our Dollar General stores to further strengthen that offering for our DG customers.

Approximately 90% of Energy Transfer's 2024 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) is projected to come from fee-based activities. Its assets also allow it to find the best times and places to sell the hydrocarbons it transports. Image source: Getty Images. cents is now higher than the 30.5

Unity only expects its revenue to rise 5% to 9% on a pro forma basis (including ironSource) this year, but its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) are quickly rising. In other words, it could leverage its early-mover's advantage in the RPA market to build its own AI ecosystem.

Management expects to generate about $80 billion in additional capacity for investments and shareholder returns through 2027 by maintaining its current leverage ratio and growing its earnings before interest, taxes, depreciation, and amortization (EBITDA).

That said, only around 75% of Enbridge's business is tied to midstream assets. The rest comes from regulated natural gas utilities and renewable power assets backed by long-term contracts. It seems like Enbridge's leverage is reasonable overall, which should help assuage dividend concerns. Data by YCharts.

The natural gas pipeline giant recently showcased its commitment to maintaining a conservative financial profile by adjusting its targeted- leverage ratio. Adjusting the target Kinder Morgan unveiled in its first-quarter earnings report that it's adjusting its long-term leverage target. times to its leverage ratio this year.

Annaly has also diversified into other assets, such as mortgage servicing rights, which, as the name suggests, give it the right to collect mortgage payments and handle customer accounts. Treasuries are considered essentially risk-free, and other fixed-income assets tend to have higher yields. per share, up from $19.25 a year ago.

There are clearly differences in the underlying assets each of these MLP's owns, but it would be understandable if an investor viewed them as somewhat interchangeable from a business perspective. In fact, Enterprise's leverage is generally at the low end of the industry relative to similarly sized peers.

They own things like pipelines, storage, transportation, and processing assets. Enbridge and other midstream companies generally charge fees for the use of their assets, sort of like charging a toll for the use of a bridge. Enbridge has more leverage than some of its closest peers, as the chart below shows.

The two biggest areas to look at when it comes to dividend safety are its distribution coverage ratio and leverage ratio. Meanwhile, the company ended last year with leverage of 3x, which is near the low end of companies in the midstream space. When the leverage at companies gets too high, there's a risk they may cut their dividend.

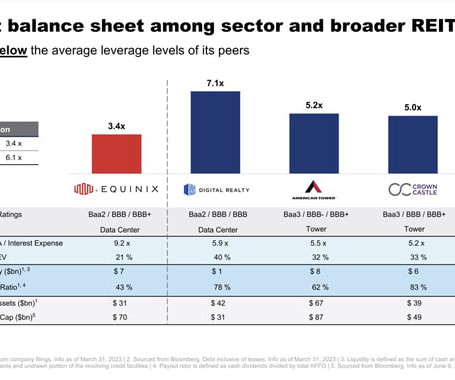

Meanwhile, many data infrastructure REITs allowed their leverage ratios to rise to relatively high levels. EBITDA = earnings before interest, taxes, depreciation, and amortization. As the slide shows, it has much lower leverage ratios than its peers. Meanwhile, its lower leverage ratio gives it more borrowing capacity.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content