This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The move would take private Hersha at an approximately 60% premium to the real-estate investment trust’s closing stock price on Friday. The deal is slated to close by year-end after shareholders okay the move. Read more Bain CapitalInvests in Sales Tech Startup Apollo.io Source: SKIFT Can’t stop reading?

Avoiding the need to tap the capital markets The most prominent benefit for miners from working with Wheaton, or peers like Royal Gold (NASDAQ: RGLD) and Franco-Nevada (NYSE: FNV) , is that they don't have to sell stock or issue debt. Selling stock dilutes shareholders and can lead to stock price weakness.

These deals are expected to be completed by the end of the year and will increase the Enbridge's exposure to natural gas utilities from 12% of earnings before interest, taxes, depreciation, and amortization (EBITDA) to 22%. So, basically, it is baking in more slow and steady growth for the future.

Kinder Morgan has done a good job of balancing investments and financial discipline. It has continued to reduce its leverage and now plans to finish the year with a net debt-to-adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ratio of just 3.9.

The telecom giant expects to generate growing free cash flow during that period, much of which it plans to return to shareholders. AT&T expects to reinvest around $22 billion of its annual cash flow into capitalinvestments in the 2025 to 2027 time frame. That positions the company to generate robust and growing cash flow.

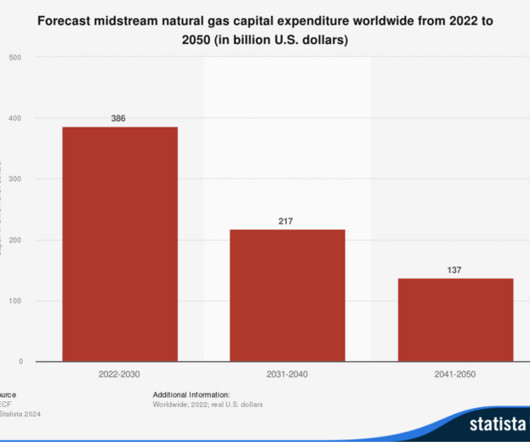

This capitalinvestment will pay off for investors for years with the majority of business underpinned by take-or-pay contracts and average contract lengths of over eight years. Importantly for investors, though, capital spending on midstream natural gas capacity is expected to be peaking this decade. Image source: Statista.

This provided much-needed liquidity for the company, but it dilutes existing shareholders. That's because there is so much capitalinvestment required to build out the nationwide logistics infrastructure. In the latest shareholder letter, management presented long-term financial targets for the company.

Adjusted operating earnings before interest, taxes, depreciation, and amortization ( EBITDA ) showed growth of 9.5% Nonetheless, noteworthy advancements continue in sustainability endeavors, a growth capitalinvestment area projected to yield fruitful returns. Notably, Waste Management saw cash flows of $2.32

ET EBITDA (Quarterly) data by YCharts The chart above illustrates that Energy Transfer has steadily increased its revenue, earnings before interest, taxes, depreciation, and amortization (EBITDA), and free cash flow over the last several years. Over the last two decades, investors have enjoyed a total return of over 2,500%.

The company estimates it could generate an additional $300 million of annual adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) from this business in the coming years. So, with dividends reinvested, Enterprise Products stock generated nearly 42% returns for shareholders in the past five years.

We are also laser-focused on optimizing our capital expenditures. billion, leveraging optimization initiatives in certain capitalinvestments. Looking ahead, we will remain highly focused on our disciplined capital allocation approach, balancing capex optimization, accretive growth, and strong shareholder returns.

We are making smart capitalinvestments in low-cost solar generation and battery storage. We have shouldered this additional growth through our reserve amortization mechanism, which enables FPL to absorb the cost for these capitalinvestments without increasing customer bills in the interim.

We are making smart capitalinvestments in low-cost solar generation and battery storage. We have shouldered this additional growth through our reserve amortization mechanism, which enables FPL to absorb the cost for these capitalinvestments without increasing customer bills in the interim.

We are deliberately allocating capital to expand and enhance our networks and improve financial flexibility to drive incremental shareholder returns. For the quarter, capital expenditures were 4.6 billion, with capitalinvestments of 5.6 Full year capitalinvestment was 23.6

Year to date, we've made capitalinvestments of 15.5 million, compared to a depreciation and amortization expense of 8.9 That depreciation and amortization expense represents 57% of capitalinvested. million for the same period. In addition to funding the 15.5 I need to get to Taft soon, and I will.

And as we start 2024, we remain steadfast in our continued focus on execution and creating long-term value for shareholders. Our two businesses are deploying capital in renewables and transmission for the benefit of customers, providing visible growth opportunities for shareholders. At NextEra Energy, the plan is simple.

We'd like to welcome all of our shareholders, analysts, and most importantly, our employees to Core Laboratories' second quarter 2024 earnings call. Chris will then give a detailed financial overview and have additional comments regarding shareholder value. Depreciation and amortization for the quarter was $3.8 Christopher S.

Subject to the evaluation and approval of our GCN Committee, we would aim to make an investment commitment in the second half of 2024 and to fund the investment by the end of 2025. in CAFD per share for our shareholders. I've had the good fortune to have dialogue with many of you in the investment community. CAFD yield.

Combined, we believe we are well positioned with strong visibility to deliver on our expectations and create long-term value for shareholders. billion for the quarter, and we now expect FPL's full year 2023 capitalinvestments to be between $8.5 With that, let's turn to the detailed results beginning FPL. year over year.

Combined, we believe we are well positioned with strong visibility to deliver on our expectations and create long-term value for shareholders. billion for the quarter, and we now expect FPL's full year 2023 capitalinvestments to be between $8.5 With that, let's turn to the detailed results beginning FPL. year over year.

And as we start 2024, we remain steadfast in our continued focus on execution and creating long-term value for shareholders. Our two businesses are deploying capital in renewables and transmission for the benefit of customers, providing visible growth opportunities for shareholders. At NextEra Energy, the plan is simple.

Our strategy introduced in 2018, coupled with consistently strong execution, is delivering results that lead industry across a range of metrics, including earnings and cash flow growth, total shareholder distributions, and total shareholder returns since 2019, the baseline year of our plans. Now, I'll turn it back to Jennifer.

in the prior-year quarter, which is inclusive of product-related intangible amortization for both periods presented. The decline in GAAP gross profit is primarily the result of step-up amortization from the NuVasive merger, which will end during our fiscal fourth quarter. Our capital allocation priorities remain unchanged.

Moritex's heavy exposure to electronics and semi has also negatively impacted its recent growth, but we expect to see growth in those segments rebound as capitalinvestment in equipment to support demand for chips grows over the remainder of this decade. We are excited about the returns that this investment can deliver.

This quarter, other income and expense was $389 million, higher than anticipated, driven by interest income, partially offset by net losses on investments and foreign currency remeasurement. billion to shareholders through share repurchases and dividends. Our effective tax rate was approximately 18%. And finally, we returned $9.1

With the strongest balance sheets in the sector and worldwide banking relationships, we believe NextEra Energy has both significant access to capital and cost-of-capital advantages and is well positioned to continue to deliver long-term value for shareholders. FPL's capital expenditures were approximately $2.6

With the strongest balance sheets in the sector and worldwide banking relationships, we believe NextEra Energy has both significant access to capital and cost-of-capital advantages and is well positioned to continue to deliver long-term value for shareholders. FPL's capital expenditures were approximately $2.6

We are making smart capitalinvestments in low-cost solar generation and battery storage, which are continuing to reduce our overall fuel cost and when combined with generation modernizations, have saved customers nearly $16 billion since 2001. FPL's third-quarter retail sales increased 1% from the prior year comparable period.

Consistent with the prior year, the decrease in gross profit is largely associated with the NuVasive merger, namely step-up amortization. Excluding the impact of step-up amortization, adjusted gross profit was 69%. Capital expenditures during this quarter were $28.6 Moving into the performance of our business areas. of revenue.

Many of these stores had been underinvested in for years and the capitalinvestment required to fix them could not deliver an acceptable rate of return. Adjusted SG&A increased primarily from temporary labor for Dollar Tree's multi-price rollout, higher depreciation and amortization and sales deleverage.

billion to shareholders with $1.3 Cash from operations in the quarter was 925 million, capital expenditures were 381 million, and free cash flow was 544 million. billion to shareholders in the quarter, including 1.3 And I wouldn't -- look, we're amortizing the benefit of that tax move of years to go. We distributed 1.6

Turning to our final priority, we continue to allocate capital in a deliberate manner to create best-in-class experiences for customers, drive sustainable, profitable growth, and deliver long-term value for shareholders. At the same time, we're investing in the future of our company and the future of our country's connectivity.

This new action will offset about $1 billion in depreciation and amortization, which means that relative to 2022, our automotive fixed costs will be down $2 billion on a net basis as we exit '24. Tom Narayan -- RBC Capital Markets -- Analyst Hi. We will have more details to share soon. Your line is open.

We are taking actions that we believe will optimally position GrafTech to benefit from medium- to longer-term industry tailwinds and deliver shareholder value. At the same time, we remain focused on maintaining sufficient liquidity to navigate the current environment via our working capital management and other initiatives.

Our goal is to drive our cost of doing business, which is our total operating expenses excluding depreciation and amortization, toward 30% of net sales over time. Our capital allocation strategy includes a comprehensive approach to balance investing and long-term growth while providing strong returns to our shareholders.

Diluted earnings per share on a GAAP basis was $0.07, down year on year due to lower operating margins, acquisition and amortization costs, and unfavorable discrete tax items. We returned $22 million to shareholders in the form of stock buybacks and dividends. Sequentially, GAAP diluted EPS increased 7%.

Despite lower fuel prices, the Edison Electric Institute is projecting a 20% increase in the electric utility capitalinvestment from 2022 to 2024 over the previous three years. The first was $8 million of amortization of higher install costs over lower volume. And then we also had about $5 million of inventory write-downs.

Our two businesses are deploying capital in renewables, storage, and transmission for the benefit of customers while also providing visible growth opportunities for shareholders. This would further extend our scale advantages and create value for customers and shareholders. FPL's capital expenditures were approximately $2.3

Our two businesses are deploying capital in renewables, storage, and transmission for the benefit of customers while also providing visible growth opportunities for shareholders. This would further extend our scale advantages and create value for customers and shareholders. FPL's capital expenditures were approximately $2.3

We have also enhanced shareholder returns by establishing the company's first-ever share repurchase program. We conveyed that at our November 2021 Investor Day when we issued 2025 goals that we believe can create significant value for shareholders. Net debt leverage of 3.1 Total liquidity remains solid at $1.8

However, this is not simply a story of survival, but one about the value of long-term strategic decision-making underpinned by a differentiated technology and business model, driving value creation for our shareholders and our partners. This excludes an additional 5,800 construction-related jobs tied to our capitalinvestments in 2023.

Our third-quarter operating income was $273 million, which included depreciation and amortization and accretion of $78 million, round cost of $25 million, production stage expense of $12 million, and share-based compensation expense of $8 million. Since our last earnings call, we have continued to make steady progress on this journey.

Diluted earnings per share on a GAAP basis was $0.21, down year on year due to lower operating margins and higher acquisition and amortization costs. Cognex continues to have a strong cash position with $555 million in cash and investments and no debt. Sequentially, GAAP diluted EPS increased 200%. year on year and up $0.11

Second, we continue to work toward our goals of maximizing volumes on both our vehicle and energy business, but most importantly, doing so in a way that generates the capital to continue our pace of R&D and capitalinvestments. I love you, guys.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content