This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

revenues have increased to 24% of our total revenue, up 500 basis points versus a year ago, as we capitalize on our continued rapid domestic market growth and the growing demand for our innovative products and depth of content. We also generated strong gains both in the U.S. and globally, with the U.S. dollar-denominated sports rights.

Main Street Capital (NYSE: MAIN) Q4 2024 Earnings Call Feb 28, 2025 , 10:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Greetings and welcome to the Main Street Capital fourth quarter earnings conference call. Image source: The Motley Fool. You may begin. for the quarter.

Decrease in net sales was driven by a 12% decrease in the volume of megawatts sold and the aforementioned increase in our Series 7 product warranty liability, partly offset by expected payments associated with contract terminations in the U.S., This decrease was primarily driven by capital expenditures associated with our new U.S.

This is a function of investors being concerned following a July report from The Wall Street Journal that alleged legacy telecom companies utilizing lead-sheathed cables could face large environmental/health liabilities, as well as replacement costs. Furthermore, any potential liabilities would likely be determined by the U.S.

FCEVs can be charged more quickly than BEVs and have a much longer driving range, but they require more capital-intensive hydrogen charging stations to be built. million in total liabilities. Nikola is trying to differentiate itself from those competitors by selling more hydrogen-powered FCEVs. million for the full year. It had $256.3

Charles Reynolds Lambert -- Vice President, Treasurer, and Managing Director of Capital Markets Good morning and welcome to the Medical Properties Trust conference call to discuss our third quarter 2024 financial results. Land and buildings are often an operator's single largest asset, and that must be funded with some form of capital.

Rithm Capital (NYSE: RITM) Q2 2024 Earnings Call Jul 31, 2024 , 8:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Good morning and welcome to the Rithm Capital second-quarter 2024 earnings call. Should you invest $1,000 in Rithm Capital right now? Today we have $7.3

There is no structural change in our free cash flow generation, and this variance is driven primarily by certain nonrecurring working capital benefits that we previously communicated were in the prior trailing 12-month period as well as the timing of significant capital expenditure payments. That's my first question.

We finished the quarter with record liquidity and a very strong capital ratio, as Kurt will take you through, while also continuing our share repurchases, albeit at a slightly lower level, given the strong returns we saw in the bulk MSR market. You should expect us to remain disciplined in how we deploy our capital.

Since our last report, we have also begun implementation work on both our new enterprisewide POS solution and our new human capital and payroll management system. per share negative impact, primarily from unfavorable general liability insurance claims. We have also launched new mobile apps for both Family Dollar and Dollar Tree.

And in terms of the ONVO brand, as William has mentioned, the sales performance of the ONVO product didn't meet our expectations in this year considering the amortizations and other factors. But a side note here is that NIO Capital has invested in a lot of AI companies, especially industry-leading AI companies.

The other expenses that were a greater percentage of net sales in the fourth quarter were retail labor, incentive compensation, repairs and maintenance, depreciation and amortization, and technology-related expenses, partially offset by a decrease in professional fees. In 2024, total capital expenditures were $1.3 billion to $1.4

Rithm Capital (NYSE: RITM) Q1 2024 Earnings Call Apr 30, 2024 , 8:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Hello, and welcome to the Rithm Capital first quarter 2024 earnings conference call. Should you invest $1,000 in Rithm Capital right now? Today, we're at $7.1

Where appropriate, we may refer to non-GAAP financial measures to evaluate our business, specifically adjusted EBITDA, a measure of earnings before interest, taxes, depreciation, amortization, and share-based compensation. Ashley Cordova -- Chief Financial Officer I'd say that has more to do with the ending of the amortization of the royalty.

Periods of dislocation only reinforced this awareness, including Russia’s war in Ukraine and the regional bank crisis and capital market dislocation in 2023. Private capital financed 86% of LBO transactions in 2023, up from 65% in 2021. The economics of private capital are compelling. 2 The next phase is just getting started.

as compared to the prior-year quarter driven by an overall record of capital units sold during the quarter. in the prior-year quarter, driven by operational improvements as well as lower inventory step-up amortization. Adjusted gross profit, which excludes the impact of step-up amortization, was 67.1% Q4 '24 U.S. versus 55.4%

Share repurchases continue to be a high priority use of capital for us at current prices. We remain disciplined and thoughtful in our capital allocation decisions, and it is exciting to see our existing businesses find ways to grow. In our Markel Ventures operations, top-line revenues grew 5% from 4.8 billion in 2023, compared to 9.8

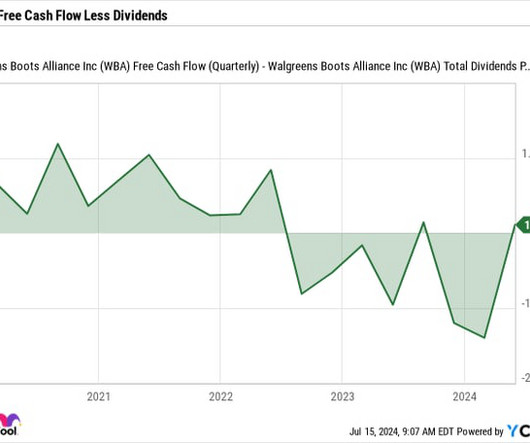

The company also only recently achieved profitability in the segment, reporting an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) profit of $23 million for the period ending May 31. Walgreens recently said that it would be "simplifying and focusing the U.S. Its total current assets of $16.3

times its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) over the past few years. It also has by far the highest market capitalization of these three REITs, at $57.3 However, management has been able to manage this debt, as shown by its coverage ratio , which has slightly dropped from 6.0

We want our shareholders to win as we earn profitable on the capital we use to do this work. First, we moved to a consistent measure of profitability of operating income across each segment of our business that excludes amortization of acquired intangible assets. Professional Liability and General Liability portfolios.

Notwithstanding our capital-constrained environment during the year, we continued to expand our experiential portfolio by effectively utilizing our operating cash flow and through limited use of our line of credit. As we have discussed previously, given our cost of capital, we are limiting our near-term investment spending.

As compared to last year, depreciation expense declined $4 million and $6 million, respectively, driven by reduced technology capital spend. Capital expenditures for the quarter were $99 million and $466 million for the year. Depreciation and amortization of $730 million, interest expense of $315 million, and a tax rate of 18%.

Importantly, capital in the form of either tangible book value or tangible common equity are significantly better than originally projected due to a combination of a smaller balance sheet and rate changes over the past year. Capital is stronger, and asset quality is well marked and accounted for. Slide 6 gives an overview.

Steve Bakke -- Vice President, Capital Markets and Investor Relations Thank you all for joining us today for Realty Income's fourth-quarter operating results conference call. billion merger with Spirit Realty Capital in an all-stock transaction in October, which closed subsequent to year-end on January 23rd. Please go ahead, sir.

Turning next to capital on Slide 17, we return 1.7 billion of capital to our shareholders in the third quarter. As we think about the Basel III proposal, the RWA increase could consume the buffer above regulatory capital requirements if the proposal is adopted as written. This included common stock repurchase of 1.3

We're pleased with Enact's continued strong operating performance and capital levels. Since Enact's IPO, Genworth has received approximately $615 million in capital from Enact, including $128 million in the fourth quarter. Then I'll provide an update on our investment portfolio and capital position before we open the call for Q&A.

While we continue to maintain strong credit ratings, a solid balance sheet, and long-term earnings growth outlook of 4% to 6%, our earnings guidance for 2024 reflects a combination of lag related to our capital investments and inflationary pressures that we are experiencing simultaneously. I'll describe these two factors in more detail.

of EPS that wasn't in our June outlook, was related to general liability claims. Predicting these claims is complex and we again increased our accrual for general liability this quarter after observing higher-than-expected costs to resolve certain claims. was attributable to the general liability adjustment, while the remaining $0.08

Second, regarding managing our debt and accelerating the path to positive free cash flow, we have committed to taking the steps necessary to improve our capital structure. Cost of revenues decreased by $6 million, or 53%, in Q4, primarily due to previous technology-related amortization expenses that became fully amortized in 2024.

For us, SG&A means selling, general, and administrative expenses including payroll and other compensation, marketing and advertising expense, depreciation and amortization expense, and other selling and administrative expenses. And we are working to ensure we are properly positioned to capitalize on this opportunity. Thanks, Chuck.

This is just a start as our goal is to get to 75 days, freeing up cash for our capital deployment priorities, which include returning cash to shareholders. Roofing granules add another year of mid-single-digit growth as we continue to capitalize on the multiyear roof replacement cycle. Last year, we returned $3.8

expanded nearly 400 basis points compared to the previous quarter due in part to pricing adjustment and cost savings from earlier restructuring activities as well as lower amortization costs, which were about $40 million consistent with our view for ongoing demand recovery. Capital expenditure were also flat sequentially at $70 million.

This increase was primarily driven by working capital improvements, resulting from focus on better managing our inventory through adjustments to our sourcing plans as well as implementation of newly adopted payment terms with our suppliers. In the spring, it became clear that we needed to do more structurally and evolve how we operate.

We are deliberately allocating capital to expand and enhance our networks and improve financial flexibility to drive incremental shareholder returns. Turning to our last key priority, the benefits from our capital allocation strategy are meaningful and evident in our results. For the quarter, capital expenditures were 4.6

Our property ranking criteria is finalized, and we are applying operational and capital allocation focus on our properties within the Fortress, Steady Eddie, and Eddie's categories. We are very pleased to see this important source of capital return to our sector, albeit selectively at this time. On to balance sheet matters.

As discussed on the year-end call in February, results in 2024 reflect a combination of regulatory lag related to our capital investments and inflationary pressures. million, primarily due to customer growth and the amortization of deferrals, partially offset by the effects of warmer weather and lower gains on gas costs.

These increases were partially offset by a $4 million decrease in amortization expense, as the intangible technology assets acquired with our rentals business completed their amortization. Please see our Terms and Conditions for additional details, including our Obligatory Capitalized Disclaimers of Liability.

I'm going to talk about the highlights of the third quarter, then we're going to do some -- a little bit of strategic updates and we're going to end up with Tony talking about the results and capital allocation. And the third is our capital allocation priorities. Our first capital allocation priority is to invest in the business.

CWEN also committed to approximately $215 million of new corporate capital deployments in 2023, an average five-year annual CAFD yield of approximately 10%, while further diversifying CWEN's fleet. And while due to capital market volatility in 2023, we didn't execute on any third-party M&A. Turning to Page 7.

The settlement also included a 50-50 capital structure and ROE of 9.4% and a cost of capital of approximately 7.1%. million, primarily due to customer growth and the amortization of deferrals. With the overall cost of capital increasing, we have remained disciplined in our approach to deploying capital.

Comparable Company Analysis This analysis benchmarks your companys valuation against similar businesses in the HVAC industry, considering factors like size, growth, geography, capital structure (including debt levels), and lifecycle stage. Six months after going to market, they executed a Letter of Intent with Amalgam Capital.

GAAP and non-GAAP measures pertaining to our operating performance and capital results are on Slide 3. In March, we successfully closed on the sale of Ally Lending, which generated capital and allows us to better serve our dealer and consumer customers. GAAP measures. Should you invest $1,000 in Ally Financial right now?

We continue to make progress on the remaining leases and expect to have entered settlement agreements with landlords for substantially all remaining lease liabilities by the end of the year. Depreciation and amortization expense was $4.5 The company has paid approximately $13 million through the second quarter.

On brand strategy, broadly, I'll say that we're in the process of thoroughly reviewing whether and to what extent our portfolio needs to change so that shareholder capital is best allocated. million in combined expenses for bad debt and loan liabilities; and 0.5 Moving on to depreciation and amortization. million for severance.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content