This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many of these companies are structured as master limited partnerships (MLPs), which pass through their profits to their unitholders and as such don't pay corporate taxes. In the past, companies often had a structure of a general partner (GP) and limited partner (LP) that ultimately was more beneficial to the GP.

Importantly, this strong performance flows through to our bottom line as we reach an inflection point in our operating leverage earlier than anticipated. Given our global reach, we believe we are the only sports technology company that can help the league engage fans and bettors all over the world and help unlock new revenue opportunities.

He bought 5% of the entire company through Buffett Limited Partnership in the 1960s prior to taking his position as the CEO of Berkshire Hathaway. That said, the company is pushing its premium cards to more consumers while raising the annual fees across its lineup. Combined, they account for about 28.4% Image source: The Motley Fool.

Listeners should be aware that today's call will include estimates and other forward-looking information from which the company's actual results could differ. On rare occasions, our expert team of analysts issues a Double Down stock recommendation for companies that they think are about to pop. Then youll want to hear this.

Companies evolve and change over time, particularly those that have long operating histories. The way that midstream companies tend to grow is through the addition of new assets. That can come via acquisitions of existing infrastructure (or entire companies) or from ground-up construction. This is important.

substantially beat the analyst consensus of $0.79, due to strong operational leverage. EBITDA = Earnings before interest, taxes, depreciation, and amortization. The company's strategic priorities center around the expansion of the ODR segment. Adjusted earnings per share (EPS) of $1.15 EBITDA $20.8 million N/A $12.6

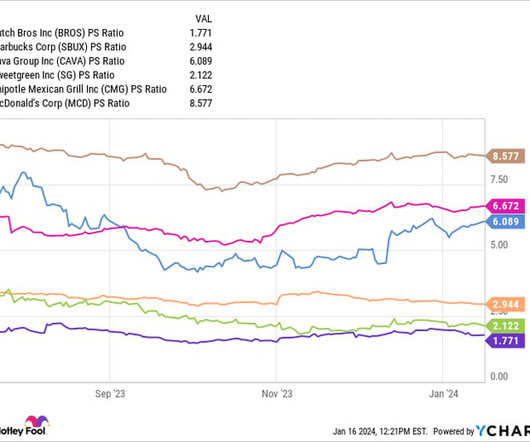

The company's "broistas" are held to a high standard of not only preparing drinks efficiently, but ensuring the customer experience is top-notch. Let's take a look at the company's financial and operating picture and assess how this approach is paying off. The company has a stated mission of opening 4,000 shops in the long run.

Learn More Ares Capital fills a hole left by banks Ares Capital Corporation is a business development corporation (BDC) that provides financing to middle-market companies -- those with earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ranging from $10 million to $250 million.

The sector has gone through a transformation in the past decade, with midstream companies reducing leverage and being more disciplined when it comes to funding growth projects. Despite the companies being in better financial shape today than under the old MLP model, the stocks trade at a discount to the 13.7

It repaid debt, which steadily drove down its leverage ratio. Today, Energy Transfer has a strong investment-grade balance sheet with a leverage ratio in the lower half of its 4.0-to-4.5x That improving leverage ratio has provided Energy Transfer with increased financial flexibility. times target range. billion of distributions.

Roughly 98% of its earnings before interest, taxes, depreciation, and amortization ( EBITDA ) comes from cost-of-service arrangements or long-term contracts. The company is acquiring three natural gas utilities , which will increase the earnings from stable gas distribution operations from 12% to 22%. target range. billion-$5.1

Rui Chen, head of investor relations of the company. The company's financial and operating results were published in the press release earlier today and are posted on the company's IR website. On rare occasions, our expert team of analysts issues a Double Down stock recommendation for companies that they think are about to pop.

The latter only includes the stocks of midstream companies structured as master limited partnerships (MLPs) , while the former includes midstream companies structured as both MLPs and corporations. MPLX MPLX (NYSE: MPLX) is a midstream company involved in logistics and storage as well as gathering and processing (G&P).

Kinder Morgan made a hard call Cutting a dividend is not something that most companies want to do, but sometimes it is the right choice. This was done because management had to choose between paying the dividend or putting money to work in capital investment projects that would grow the company.

Since the launch of its Axon 2 AI-based advertising technology in the second quarter of 2023, the company has seen explosive growth. Let's take a close look at the company's Q3 results and whether the stock is still a buy. The company's legacy apps business, meanwhile, saw revenue increase 1% to $369 million. from 69.3%

Most investors have avoided the stock as the company undergoes multiple internal and external challenges, including competition, slower growth, and geopolitical tensions. Let's focus today on the latter, pointing out two reasons to be optimistic about the company. The company is now making adjustments to recapture shoppers.

While a recession could have a major impact on some companies, it likely won't affect Enbridge (NYSE: ENB) at all. In late 2023, the company notched its 29th consecutive year of increasing its payout when it raised its dividend by 3.1% The company's low-risk business model is a big driver of its remarkable consistency.

The company also showed off strong margin improvement as its restaurant-level profit margin improved to 26.5% Margins benefited from leverage from higher sales. Adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) nearly tripled, from $12.7 from 26.1% in the quarter a year ago. million to $34.3

Enbridge (NYSE: ENB) is not an exciting company, but that's really part of management's plan. With 29 years' worth of annual dividend increases, the Canadian energy company has clearly lived up to the plan. To be fair, that's higher than most midstream companies, but it is also lower than most utility companies.

Shares of Home Depot (NYSE: HD) finished lower today as investors seemed to give a thumbs-down to its deal to buy SRS Distribution, a leading specialty-trade company that will help it expand its presence in the pro market. The deal is certainly a risk for Home Depot and represents the company's first major move under CEO Ted Decker.

That said, the company continues to add new features and capabilities to the app that should result in continued organic growth and even higher monetization rates over the long run. For a company with the growth potential of Block and two sticky products, that looks like a great use of your $100. Then youll want to hear this.

However, the company is set to go into growth mode, which should excite investors even more. Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, rose 6% to nearly $2.5 Enterprise ended the quarter with leverage of 3x. Prior to the COVID-19 pandemic in 2019, the company spent $4.3

The company's dividend yield has been in the double digits throughout most of 2023 and currently tops 13%. Other investors were more anxious about the fact that the company's executives didn't utter the word "dividend" in the Q2 conference call. Few stocks offer as juicy of a dividend as Medical Properties Trust (NYSE: MPW).

The company beat revenue estimates, made progress on the bottom line, and offered first-quarter guidance that was better than the analysts' consensus view. The company also reported another quarter with average unit volumes of $2.9 The company also reported another quarter with average unit volumes of $2.9 million to $1.8

What happened Shares of SoFi Technologies (NASDAQ: SOFI) climbed 37% in July, according to data provided by S&P Global Market Intelligence , after the fintech and banking company announced strong second-quarter 2023 results and raised its full-year outlook. So what SoFi bolstered its member count by 44% year over year to 6.2

The Canadian pipeline and utility company has paid dividends for more than 69 years, including increasing its payout for the last 29 straight years. Meanwhile, the company is on track to achieve its financial guidance for the 19th year in a row. Those factors give the company significant visibility into its cash flows.

Utilizing his remarkable skill set, he transformed Berkshire Hathaway from a struggling textile company into a multinational holding company with a valuation of over $750 billion. As a result of Apple's aggressive share buybacks, the company has lowered its outstanding share count by 37.5% over the past decade.

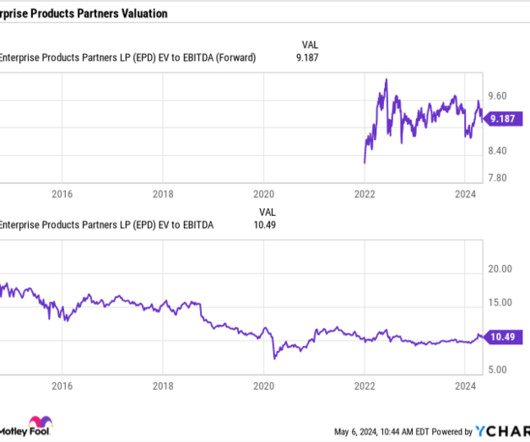

Most of its businesses are fee-based, but this gives the company additional opportunities to profit when seasonal, regional, or product spreads arise. The company is particularly well positioned in the Permian, the most prolific oil basin in the U.S. forward yield and low leverage of 3.1 billion in 2025.

Many factors can cause a company to trade at a relatively lower valuation. It's a confounding discount, since the economically equivalent companies have the same earnings ($0.72 The company and its partners recently agreed to acquire Triton International in a cash-and-stock deal, valuing Triton's equity at $4.7 billion to $13.5

The Trade Desk (NASDAQ: TTD) has been at the forefront in leveraging this opportunity by programmatically matching buyers and sellers of advertisements on the CTV (connected television, a device or software used to support video content streaming) platform. The company is already profitable and cash-flow positive. billion in 2022.

However, despite their differences, these companies need each other to thrive in today's world. That's evident in a recent collaboration agreement between these companies, with Microsoft helping Enbridge harness the power of artificial intelligence (AI) to enhance its operations. That will save the company money and reduce emissions.

The company's latest results are a case in point. It's a better way to estimate the long-run cash flow potential of the company. From 1990 to 2022, for example, Heico achieved an impressive 15% compound annual growth rate (CAGR) with regard to revenue, while the company increased its net income at an 18% CAGR during the same period.

ChargePoint (NYSE: CHPT) became the world's first publicly traded electric vehicle (EV) charging network company after it merged with a special purpose acquisition company (SPAC) on March 1, 2021. That stock offering won't increase its leverage, but it will cause significant dilution for a company with an enterprise value of only $1.4

Shares of Verizon Communications (NYSE: VZ) were falling after the wireless company reported mixed second-quarter earnings results. Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) edged up 2.5% The company enjoyed strength in its important wireless business, where revenue rose 3.5%

Further, the company has increased its payment for 25 straight years. The company offers a higher 8.3% It has two business segments: Logistics & Storage : The company transports, distributes, stores, and markets crude oil, refined products, and other hydrocarbons. leverage ratio , which falls in the middle of its 2.75-3.25

The company added 2 million active accounts in Q2, bringing the total to 83.6 Roku prides itself on being an agnostic platform that plays ball with all the content companies out there. For starters, the company isn't generating positive-net income. This tells me that the content publishers have the negotiating leverage.

The cybersecurity company dazzled the bulls with its impressive growth rates. Analysts expect its revenue to grow at a CAGR of 33% from 2022 to 2025, and for its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) to rise at a CAGR of 54%. Image source: Getty Images.

But where could the company be five years from now, and is this an underrated investment to add to your portfolio today? As of June 30, the company's long-term debt was over $17.2 As of June 30, the company's long-term debt was over $17.2 That's a concerning number when the company's current assets total less than $10 billion.

The table below shows the company's improvements in earnings and cash flow. I've also included its adjusted debt to earnings before interest, taxation, depreciation, amortization, and rent ( EBITDAR ) multiple. JPMorgan Chase is an advertising partner of The Ascent, a Motley Fool company. billion at the end of 2022 to $29.2

The list of pros includes the dividend (but for more than just the yield), the diversified underlying business, and the expansion the company has undertaken. to 5 times debt to EBITDA (earnings before interest, taxes, deprecation, and amortization). It boasts an attractive dividend yield Enbridge's dividend yield of 6.9%

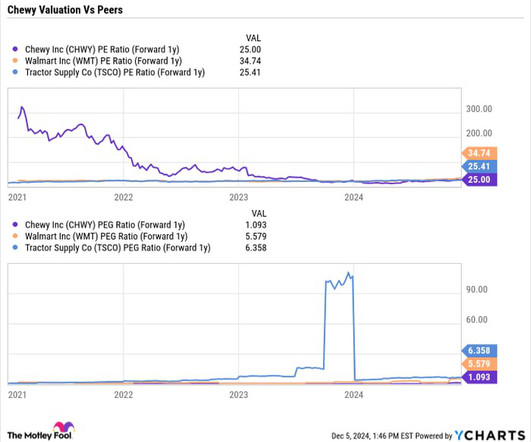

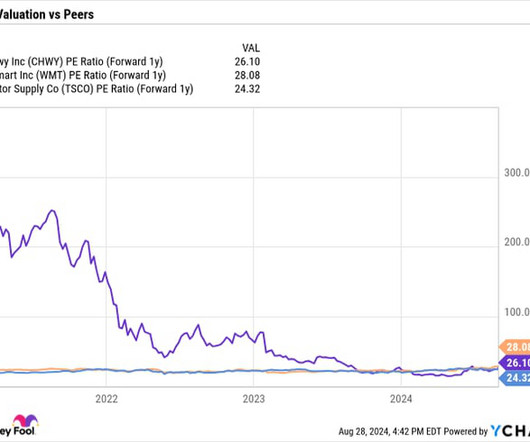

Shares of Chewy (NYSE: CHWY) were trading lower last week following the online pet products retailer's third-quarter results, despite the company increasing its full-year guidance. Gross margin continues to be a focus for the company, and it saw a year-over-year improvement of 80 basis points to 29.3%. Gill has since taken his profits.

The company also saw mobile orders climb 15% after it revamped its app. Meanwhile, the company said it was seeing selling, general, and administrative expenses (SG&A) leverage, as 40% of its order volume is now benefiting from automation. The company opened two vet clinics in the quarter, bringing the total to six.

As the global economy evolves, investors are always on the lookout for innovative companies that can offer high returns. One such company that's lately been generating a lot of buzz is Symbotic (NASDAQ: SYM) , a cutting-edge robotics and automation company that's taking the logistics industry by storm.

The opportunity for the company's Square and CashApp ecosystems to gain an expanding slice of an estimated $205 billion addressable market highlights a significant runway. Several trends underpin a long-term outlook, including Block's ability to leverage its multiproduct platform.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content