This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Importantly, this strong performance flows through to our bottom line as we reach an inflection point in our operating leverage earlier than anticipated. We made a strong start into leveraging our existing partnerships with global operators entering the market while expanding ties with local operators seeking additional capabilities.

The company expects to further leverage lower-cost seed-based technology by targeting approximately 20% of harvests from seeds in fiscal 2025 with monthly fluctuations between 15% and 30% depending on the cultivar requirements. million, including both restricted and unrestricted cash, and negligible debt. million in Q4 compared to $3.5

Learn More Ares Capital fills a hole left by banks Ares Capital Corporation is a business development corporation (BDC) that provides financing to middle-market companies -- those with earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ranging from $10 million to $250 million. Image source: Getty Images.

It repaid debt, which steadily drove down its leverage ratio. Today, Energy Transfer has a strong investment-grade balance sheet with a leverage ratio in the lower half of its 4.0-to-4.5x That improving leverage ratio has provided Energy Transfer with increased financial flexibility. times target range.

billion, including debt, and will pay for the deal with cash on hand in debt. Home Depot makes a big move Home Depot will acquire SRS Distribution for $18.25 SRS will give Home Depot a stronger presence with its Pro customer, an area where it typically has an advantage over rival Lowe's.

KMI Financial Debt to EBITDA (TTM) data by YCharts That said, a part of the problem was Kinder Morgan's more aggressive use of leverage than its peers'. Kinder Morgan's leverage is lower today, but it still tends to use more leverage than Enterprise.

The deal will undoubtedly cause some debt concerns since the company already has nearly $10 billion in net debt (total debt minus cash and cash equivalents). For comparison, Kroger's net leverage ratio at the end of its fiscal first quarter 2023 was a much-healthier 1.3 times EBITDA.

Its debt load will continue to come down A big reason investors aren't overly thrilled with Viatris is that the business has a lot of debt on its books; that's not a good look as interest rates are rising. As of June 30, the company's long-term debt was over $17.2 The company is targeting a gross leverage ratio of 3.0.

But it's not bad news for debt providers because they have been rewarded for putting up capital, with their investment backed up by a relatively liquid asset, the airplanes themselves. I've also included its adjusted debt to earnings before interest, taxation, depreciation, amortization, and rent ( EBITDAR ) multiple.

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 Western appears on track to reach its leverage (net debt/adjusted EBITDA) goal of 3 times by year end, at which point it could pay out excess (special or variable) distributions above its current $0.875 quarterly based payout.

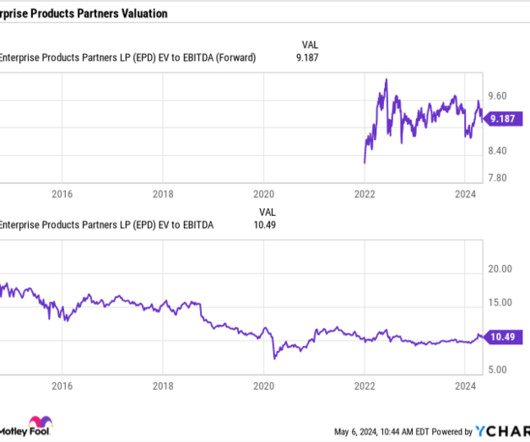

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, rose 6% to nearly $2.5 Enterprise ended the quarter with leverage of 3x. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. cents per unit.

Roughly 98% of its earnings before interest, taxes, depreciation, and amortization ( EBITDA ) comes from cost-of-service arrangements or long-term contracts. Finally, Enbridge has a strong balance sheet with a conservative leverage ratio. times leverage ratio , well within its 4.5x-5.0x target range. billion-$6.6

Also, the healthcare REIT's leverage as measured by the adjusted net debt to transaction-adjusted annualized EBITDAre (earnings before interest, income taxes, and depreciation and amortization for real estate) increased in Q2. Wall Street might actually cheer a dividend cut that enabled the company to lower its debtleverage.

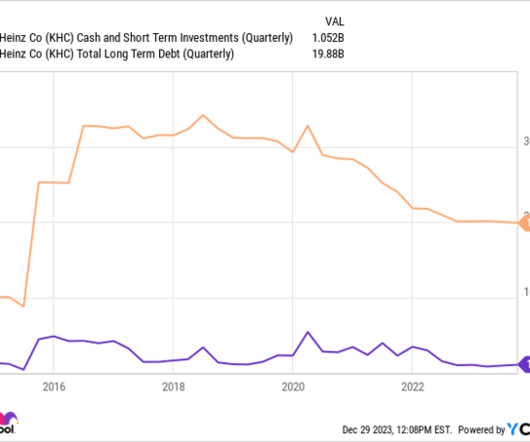

However, the merger also loaded up the new entity with debt. Below, the merger more than tripled the company's debt to over $30 billion. KHC Cash and Short-Term Investments (Quarterly) data by YCharts But through cost-cutting and divesting non-strategic brands, Kraft Heinz has slowly gotten its debt back under control.

Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) edged up 2.5% Verizon's balance sheet is also in solid shape, with the leverage ratio on unsecured debt (net unsecured debt/trailing-12-month adjusted EBITDA) coming in at 2.5. billion consensus. Meanwhile, it has paid out dividends of $5.6

The cruise line operator's revenue plunged in 2020 and 2021 as global travel ground to a halt during the pandemic, and it was forced to take on a lot more debt to stay solvent. On an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) basis, it generated a profit of $3.3 NYSE: CCL). billion in 2025."

Carnival's financial position improved steadily over the course of 2023, reducing its debt balance by $4.6 Looking ahead to 2024, Carnival expects adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) to reach $5.6 As it pays down debt and lowers its interest expense, the bottom line should also improve.

Enbridge currently gets 98% of its earnings before interest, taxes, depreciation, and amortization (EBITDA) from stable cost-of-service or contracted assets. The company currently boasts an investment-grade credit rating backed by a leverage ratio toward the low end of its 4.5-5.0 times target range. billion-$6.6

The company continues to see a ton of operating leverage in its business as sales climb, with gross margin for the quarter improving to 77.5% Adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, climbed 72% to $722 million. billion in net debt. Overall revenue climbed 39% to $1.2

That makes logical sense, given that, historically, around 57% of its earnings before interest, taxes, depreciation, and amortization ( EBITDA ) came from oil pipelines, with another 28% from natural gas pipelines. Enbridge is a North American energy giant that is usually lumped into the midstream sector. and 5 times.

Why the stock scares off some investors The debt-to-equity (D/E) ratio of DigitalOcean is a negative 675% due to total debt of $1.47 This ratio measures a company's financial leverage. You can calculate it by dividing the company's total debt by shareholder equity. On the one hand, the company has high debt.

SoFi CEO Anthony Noto pointed out the company is benefiting from a combination of strong cross-buying activity and improving operating leverage thanks to its "broad product suite and unique Financial Services Productivity Loop (FSPL) strategy." Deposits at the company's SoFi Bank subsidiary also soared 26% sequentially this quarter, to $12.7

For example, its ratio of debt to EBITDA ( earnings before interest, taxes, depreciation, and amortization ) is generally among the lowest of its closest peer group. Acquisitions are partly to blame for that trend, but investors need to understand that leverage increases risk. Trust The next big issue here is less tangible.

The company now holds a significant amount of debt. Management plans to divest non-core assets to accelerate the paydown of that debt. Shares currently trade for an enterprise value/earnings before interest, taxes, depreciation, and amortization (EV/ EBITDA ) multiple of just 5x. By comparison, Chevron trades for a 6.6x

in net debt to earnings before interest, taxes, depreciation, and amortization ( EBITDA ). Further evidence of Franco-Nevada's appeal for conservative investors comes from the stock's rock-solid balance sheet that features zero debt and $1.3 Currently, investors can grab shares of Agnico Eagle from the bargain bin.

For many years, there were a lot of opportunities for midstream companies to grow, and investors were happily willing to help finance that via the equity and debt markets. Leverage has also been reduced, with debt-to-earnings before interest, taxes, depreciation, and amortization ( EBITDA ) at roughly 3.2

Further, its distributable cash flow payout ratio is well within management's target range of 60% to 70% The balance sheet is also healthy: Leverage is well within management's target range of 4.5 to 5 times debt to EBITDA (earnings before interest, taxes, deprecation, and amortization). ENB Dividend Yield data by YCharts.

Its balance sheet isn't pretty ChargePoint insists it can turn profitable on an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) basis by the fourth quarter of calendar 2024 (which lines up with the third and fourth quarters of fiscal 2024). However, its high debt-to-equity ratio of 2.9

Unlike some aggressive companies that jeopardize their financial well-being by relying heavily on leverage to pursue acquisitions, Heico has adopted a more conservative approach. At the end of 2022, Heico's net debt-to-earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ratio was only 0.25.

Meanwhile, the company said it was seeing selling, general, and administrative expenses (SG&A) leverage, as 40% of its order volume is now benefiting from automation. It ended the period with $695 million in cash and marketable securities and no debt. Adjusted earnings per share (EPS) soared 60% to $0.24.

Management expects to generate about $80 billion in additional capacity for investments and shareholder returns through 2027 by maintaining its current leverage ratio and growing its earnings before interest, taxes, depreciation, and amortization (EBITDA). They're still working to pay down debt, which eats up a lot of cash flow.

billion in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and $1.2 Sirius XM is also starting to pay down its long-term debt since that bearish leverage peaked in 2022. It has posted an annual profit every year since 2010. The model works. It expects to generate $2.7

BigBear.ai (NYSE: BBAI) and SoundHound AI (NASDAQ: SOUN) are two small-caps attempting to leverage unique AI-powered applications into long-term growth. The company reported a loss on Q2 adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of $3.7 Image source: Getty Images. The case for BigBear.ai

Since our last earnings call on April 30, I am pleased to announce that we are making solid progress on our path forward of one, simplifying the business; two, operational performance improvement and three, reducing leverage. Our path forward goal is to reduce $2 billion in debt. One, a $4 million increase in interest expense.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprise value (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower. Today, multiples throughout the industry are much lower.

But the hope is that with a much larger number of units sold and higher revenue, the business will be better able to leverage its fixed costs and approach management's goal of EBITDA ( earnings before interest, taxes, depreciation, and amortization ) margins between 8% and 13.5% over the long term.

It has continued to reduce its leverage and now plans to finish the year with a net debt-to-adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ratio of just 3.9. Kinder Morgan has done a good job of balancing investments and financial discipline. in dividends per share.

It locks in the spreads with hedges and then uses leverage to increase its returns. Main Street Capital Another stock that pays a monthly dividend is Main Street Capital (NYSE: MAIN) , which is a business development company (BDC) that invests in the debt and equity of lower-middle-market companies. Image source: Getty Images.

billion in adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). Chief Investment Officer Mark Manduca said in an interview that the company's debt-to-EBITDA ratio would be within investment-grade range by the end of the year, potentially setting the company up for an acquisition.

In fact, management thinks that Carnival will produce adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of $4 billion (at the midpoint) this fiscal year. The company also has $33 billion of long-term debt on its balance sheet. That's quite the turnaround from last year.

The benefits for Main Street included significant dividend income, fair value appreciation, and the realized gain, resulting in best-in-class returns on our equity investment, in addition to the attractive interest income provided by our debt investments. This compares favorably to the 4.4 times money invested return on our equity investment.

Looking ahead, management also gave new long-term guidance, calling for adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) per available passenger berth day (ALBD/APBD) to increase by 50% by 2026, reaching its highest level in almost two decades.

Part of the reason is that it has an incredibly conservative balance sheet, with low leverage giving it the wherewithal to add debt during tough times to support its business and your dividends. It has proven that it is a survivor and one that can support its attractive 4.3% dividend yield even if oil prices plunge.

Thanks to fast portfolio growth and impressive operating leverage, servicing income reached $273 million. during the first quarter, minimizing our amortization expense. Finally, we did an outstanding job generating positive operating leverage, with expenses up only $6 million sequentially, despite our rapid growth.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content