This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

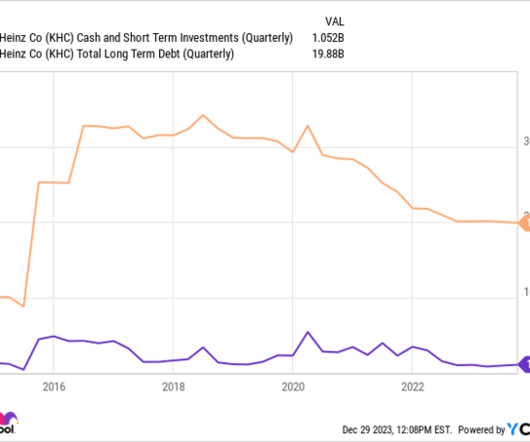

Strong cash flows have management thinking it can reduce its debt load from 2.9 times adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) at the moment to 2.5 times adjusted EBITDA in the first half of 2025. Consider when Nvidia made this list on April 15, 2005.

If you're searching for a reliable income stream from your investment portfolio, Ares Capital (NASDAQ: ARCC) is one stock that should be on your radar. Add in regulations due to the fallout of the Great Recession , and banks have focused on lending to larger companies whose debt is seen as less risky and more liquid.

The company is debt free and had a liquidity position of about $1.3 And hospitals, after spending more than $1 million to buy or lease a robot, probably will continue using it to amortize the investment. It's a great way to instantly diversify your portfolio, offering you exposure to 11 industries and many of today's top stocks.

British American Tobacco's debt-heavy balance sheet is partially a result of this cigarette megadeal. Reynolds brought with it a portfolio of popular brands, including Newport, Camel, and American Spirit. Going even further, the company will begin amortizing the remaining value of those brands in 2024. cigarette brands.

After staring at the brink of bankruptcy, a debt restructuring deal rescued the stock. The company has now reported an earnings before interest, taxes, depreciation, and amortization ( EBITDA ) profit and positive net income for each of the first two quarters in 2024. Also, most of that debt has interest rates between 12% and 14%.

billion in consolidated debt and only $12.6 billion in earnings before interest, taxes, depreciation, and amortization ( EBITDA ), and $31.3 billion in net debt in 2026. Boeing gets a downgrade An analysis of Akers' report suggests his reasoning is sound, and there are serious questions about Boeing's free cash flow ( FCF ).

Guidance for fourth-quarter adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) of $114 million came in below analyst expectations of $116 million based on net yield growth guidance of 5% compared with last year, which management says was very strong. The large debt is the hole in the Carnival investment thesis.

Real estate companies have a lot of depreciation and amortization, which is deducted as an expense under GAAP. Since depreciation and amortization is a non-cash charge, net income tends to understate the cash flow of the company. billion in mortgages and debt maturing in 2024 that it will need to roll over.

billion, including debt, and will pay for the deal with cash on hand in debt. Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month.

A key part of the company's approach is to adjust its portfolio along with the changes taking shape in global energy demand. That's why the company's portfolio includes oil pipelines , natural gas pipelines, natural gas utilities, and renewable power investments. But Enbridge offers so much more than just a dividend.

This probably won't be the fastest-growing dividend in your portfolio, but continued movement in the right direction seems likely. billion of net debt on AT&T's balance sheet at the end of 2023 is concerning, but the company's efforts to reduce it have been encouraging. Net debt fell to 2.97 With the U.S.

Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) more than doubled from last year in the first quarter to $871 million, and Carnival reported its third consecutive quarter of positive operating income. The market won't give Carnival a high valuation when it's not profitable and has a high debt load.

Shares of the phone and internet service provider have fallen about 23% in 2023 as investors worry about a high debt load and potential litigation regarding lead-lined cables. Selling off its media assets helped reduce AT&T's debt load, but the company was still sitting on $132 billion in net debt at the end of June.

billion, we expect to gradually resume receipt of cash rents on this portfolio in the first quarter of 2025, ramping up to approximately $90 million in the aggregate annualized rent by the end of 2025 and fully stabilized aggregate annualized rent of approximately $160 million by the end of 2026. Beginning in 2016, MPT spent roughly $5.3

AT&T finished September with $129 billion in net debt. 30 and it's using these profits to reduce debt. The company is on pace to achieve a net debt-to-adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ratio in the 2.5 billion portfolio is spread across 130 portfolio companies.

Just as a diverse stock portfolio keeps you afloat when one stock languishes, its diverse revenue streams keep Illinois Tool Works afloat when one segment hits hard times. I've seen numerous companies harm shareholders with massive debt-fueled acquisitions that put the balance sheet in peril.

But where could the company be five years from now, and is this an underrated investment to add to your portfolio today? Its debt load will continue to come down A big reason investors aren't overly thrilled with Viatris is that the business has a lot of debt on its books; that's not a good look as interest rates are rising.

This is a diverse portfolio of products that consumers buy constantly, making it a durable business model that should thrive in good and bad times. However, the merger also loaded up the new entity with debt. Below, the merger more than tripled the company's debt to over $30 billion. Is it perfect yet?

Shares of Ares Capital offer an ultra-high dividend yield because the market has concerns about its borrowers' ability to repay debt that got a lot more expensive over the past year and a half. More than two-thirds of this BDC's portfolio earns interest at variable rates. At the end of June, loans representing 1.1%

It also cut the dividend enough to free up cash to help pay down debt. T Cash Dividend Payout Ratio data by YCharts Yep, that's discretionary cash profits that can go toward paying down debt (more on that in a minute) and eventually repurchasing shares to help drive earnings growth. However, things could finally be looking up.

Plug Power has been promising it's close to adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) break-even for over a decade, which I highlighted as far back as 2017 ! PLUG Total Long Term Debt (Annual) data by YCharts It won't be as easy to raise the billions of dollars needed to fund operations in the future.

billion in net debt, not including operating leases, an ill-advised investment was not a good use of cash. Healthcare segment was able to flip to positive adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of $17 million and a modest adjusted operating loss of $34 million. For a company with $8.8

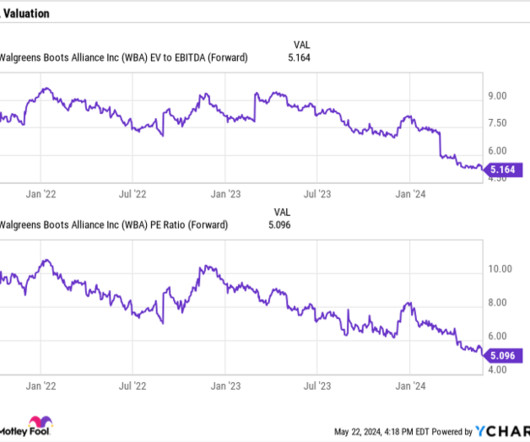

billion, with adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) of $23 million, an improvement from negative $113 million a year ago. billion in debt and $703 million in cash. Walgreen's balance sheet is loaded with debt, so paying off debt and returning to positive free cash flow is a priority.

But what's the best route to add some glitter to your portfolio? in net debt to earnings before interest, taxes, depreciation, and amortization ( EBITDA ). Further evidence of Franco-Nevada's appeal for conservative investors comes from the stock's rock-solid balance sheet that features zero debt and $1.3

Apple At a stake worth over $150 billion, Apple (NASDAQ: AAPL) represents nearly 50% of Berkshire's portfolio, making the tech company by far and away the largest position it holds. The deal will undoubtedly cause some debt concerns since the company already has nearly $10 billion in net debt (total debt minus cash and cash equivalents).

There was $129 billion in net debt on AT&T's balance sheet at the end of September, which isn't as frightening as it might seem. The company expects to achieve a manageable net debt-to-adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA) ratio of 2.5 million in net unsecured debt.

It had no revenue and was taking on huge debt. That led to earnings before interest, taxes, depreciation, and amortization ( EBITDA ) to rise 5% per unit from 2019 levels despite interim inflation. The main risk now lies in its debt repayment. There's still plenty of room to move up, and 2024 might be the best time to buy.

His most recent purchase for Berkshire Hathaway's portfolio amounted to about $246 million. The company now holds a significant amount of debt. Management plans to divest non-core assets to accelerate the paydown of that debt. That follows purchases of about $589 million and $312 million in December.

Over the past two years, its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margins shrank and it racked up steep losses. billion in long-term debt and a staggering debt-to-equity ratio of 70. billion (which includes all of its long-term debt), it trades at just 1.8 billion in 2024.

But it's not bad news for debt providers because they have been rewarded for putting up capital, with their investment backed up by a relatively liquid asset, the airplanes themselves. I've also included its adjusted debt to earnings before interest, taxation, depreciation, amortization, and rent ( EBITDAR ) multiple.

In Verizon's case, the market is worried about a debt load that rose to $150.7 Verizon's debt load works out to about 2.6 times adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). This is on the high side, but Verizon has the means to steadily reduce its debt load and raise its dividend payout.

On the bright side, Walgreens' healthcare segment, which delivers treatment direct to consumers, generated adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA ) of $23 million for the first time in Q3. billion in debt while issuing $24.1 And, with $33.6 Over the last 12 months, it repaid $26.8 billion more.

However, due to the $6 billion in long-term debt it took on to fund that purchase, the market has taken a cautious view toward Nasdaq's stock, and it remains below its pre-acquisition announcement price. Armed with this growing FCF creation, management aims to lower Nasdaq's debt load from 4.3 With its $10.5 times within three years.

I first added the midstream giant to my portfolio in early 2020, right before the pandemic hit. It repaid debt, which steadily drove down its leverage ratio. Roughly 90% of its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) come from stable, fee-based sources. billion of distributions.

Net yields and adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) are at or close to 2019 levels, and Carnival is on track to meet its three-year growth goals ahead of schedule. Carnival assumed tons of debt and is still carrying more than $30 billion on its balance sheet. There's still risk today.

Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) edged up 2.5% Verizon's balance sheet is also in solid shape, with the leverage ratio on unsecured debt (net unsecured debt/trailing-12-month adjusted EBITDA) coming in at 2.5. billion consensus. Meanwhile, it has paid out dividends of $5.6

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, rose 6% to nearly $2.5 It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. The company is also in solid financial shape concerning its debt load.

Lumen is a debt-riddled company whose stock became distressed earlier this year. However, an early-year deal to extend its debt maturities, combined with long-term deals for AI (artificial intelligence) networking, caused the stock to skyrocket in early August. billion in debt and pension liabilities. as of 2:23 p.m.

to 5 times debt to EBITDA (earnings before interest, taxes, deprecation, and amortization). This list is important to examine, however, because it speaks to the very different segments contained within the portfolio. Simply put, the dividend is on a strong financial foundation. ENB Dividend Yield data by YCharts.

If you are trying to live off the income your portfolio generates, history suggests the lower-yielding master limited partnership (MLP) will be a much safer choice. For example, its ratio of debt to EBITDA ( earnings before interest, taxes, depreciation, and amortization ) is generally among the lowest of its closest peer group.

billion in growth capex a year would allow it to pay its distribution while having money left over from its cash flow to pay down debt and/or buy back stock. million in EBITDA (earnings before interest, taxes, depreciation, and amortization) a year. billion in debt, $3.9 Moving forward, spending between $2.5 billion to $3.5

Reducing its debt-to-earnings before interest, depreciation, amortization, and rent (EBITDAR) ratio to parity compared to a figure of 2.9 To put these figures into context, a significant reduction in debt-to-EBITDAR would derisk the stock from investors' fears over its debt load, and an FCF of around $4 billion is worth more than 9.7%

Below, I'll highlight some strengths against the company's weaknesses to see if adding it to your portfolio makes sense. The company invested heavily and is still servicing an enormous debt. billion in net debt. At the end of March, the telecom giant's net debt pile equaled 2.9 in the first half of 2025.

year-over-year increase in its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) to nearly $1.9 NextEra Energy Partners benefited from the increased income earned by new projects added to the portfolio and a reduction in management fees from its parent, NextEra Energy. It delivered a robust 13.6%

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content