This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The company is debt free and had a liquidity position of about $1.3 And free cash flow and return on invested capital are on the rise, showing Chewy is benefiting from its investments. And hospitals, after spending more than $1 million to buy or lease a robot, probably will continue using it to amortize the investment.

ITW Return on Invested Capital data by YCharts. The company has prudently acquired companies over the years (more than two dozen acquisitions), steadily increasing its return on invested capital (ROIC). While Illinois Tool Works leans on debt, it doesn't do so too heavily. TTM = trailing 12 months.

As the International Air Transport Association argues, "Even prior to the COVID-19 crisis, equity owners had not been rewarded adequately for risking their capital," because "average airline returns have rarely been as high as the industry's cost of capital." Using cash flow to pay down debt (adjusted debt fell from $32.9

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, rose 6% to nearly $2.5 It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. The company is also in solid financial shape concerning its debt load.

Best-in-class profitability In addition to this advantage from monetizing the by-product of its core collections business, Waste Management has historically held higher return on invested capital (ROIC) figures than its two most prominent peers. ROIC shows that it is the best in its industry at reinvesting in its business.

billion in adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). Chief Investment Officer Mark Manduca said in an interview that the company's debt-to-EBITDA ratio would be within investment-grade range by the end of the year, potentially setting the company up for an acquisition.

With interest rates rising at their fastest pace in four decades, the return on investment for solar and wind projects is no longer as compelling. On the other hand, Alliance Resource Partners' management team has done an excellent job of conservatively expanding production while keeping debt-servicing costs manageable.

It reported a better-than-expected adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) profit of $681 million, though it's still losing money on a generally accepted accounting principles ( GAAP ) basis. The company said customer deposits reached a record of $7.2 billion-$4.25

However, one goal may be even more important than all of these : reducing debt. Carnival's debt load remains alarming While Carnival's revenue and operating income have exceeded pre-pandemic levels, the cruise company's stock is still 68% below its all-time high of $66 , reached in early 2018. billion in long-term debt.

Carnival's wall of debt First, let's take a quick look back in time at the challenges Carnival faced in recent years. The halt in sailings drove the previously profitable company to a loss, and resulted in Carnival building up a wall of debt. Carnival also has prepaid debt, for example prepaying $7.3 Image source: Getty Images.

We owe an immeasurable debt of gratitude to Bernie. In the quarter, pre-tax intangible asset amortization was $138 million including $86 million related to SRS. Excluding the intangible asset amortization in the quarter, our adjusted operating margin for the third quarter was 13.8%, compared to 14.5%

Data source: Author's calculations using amortization calculator. You will be chipping away at your debt a little bit each month, but it will be many years until more of your money actually goes towards principal. In that February payment, more than 20 years after you started repaying your debt, $1,331.93 would go to interest.

On the bottom line, Carnival continued to move in the right direction though the company is still facing stiff headwinds from its heavy debt burden, which jumped during the pandemic. The company is making progress on easing its debt burden as it prepaid more than $1 billion in short-term, variable-rate debt, though it still has about $7.5

Generating positive free cash flow (FCF) every year since the turn of the century, the stock has delivered total returns of 3,600% over that time -- or seven times the S&P 500 index's return. This $400 million outlay gives the company plenty of integration work to do as it focuses on paying down its $686 million net debt balance.

So, to examine this, investors can look at what each company is generating as a return on invested capital (ROIC). LOW Return on Invested Capital data by YCharts A high ROIC is excellent, but what a company pays for its capital, called the weighted average cost of capital, or WAAC , is just as important.

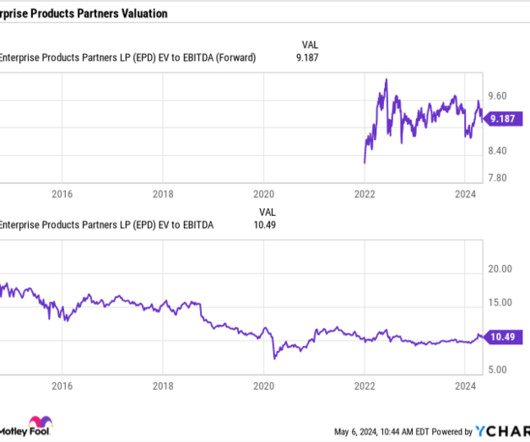

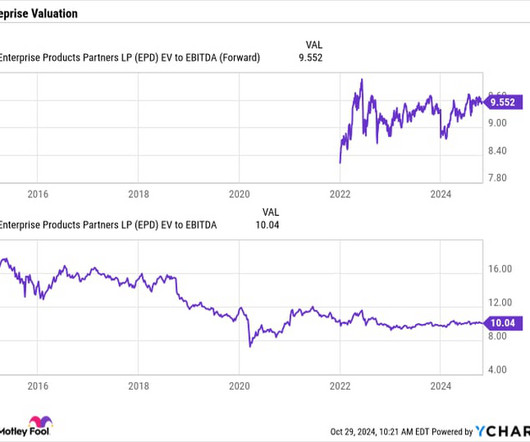

It has averaged a return on invested capital (ROIC) of about 12% over the past decade. Enterprise value takes into consideration a stock's net debt, while EBITDA removes non-cash expenses. The company currently plans to spend between $3.25 billion to $3.75 On that basis, Enterprise is trading at just over a 9x multiple.

s (NYSE: CCL) debt was enough to make investors cringe -- and flee the stock. Cruise operators were forced to halt sailings during the early stages of the pandemic, and as a result, Carnival took on more and more debt to stay afloat (excuse the pun). This is key because free cash flow is the tool to pay down debt.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) also rose 5% to nearly $2.44 It ended the quarter with leverage of 3x, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. It produced distributable cash flow (DCF) of $1.96

The second thing that this gets rid of is the debt. When we get to this return number, why are we getting debt out of this thing? Asit Sharma: Let's now extend net tangible assets by one letter, unlevered net tangible assets and that is getting rid of the debt. We're talking about real returns. Why is that?

Yet, on the other hand, inflation and higher interest rates are a big counterweight to the bull case, as all major cruise companies are now loaded with debt -- a result of the emergency borrowing during the pandemic -- while also battling higher labor costs. In 2023, investors in the largest cruise company in the world, Carnival Corp.

Further, management said it had made substantial progress toward its 2026 "SEA Change" goals of sustainability; earnings before interest, taxes, depreciation, and amortization (EBITDA) per available lower berth day; and return on invested capital (ROIC). billion after Q2, even larger than Carnival's $26.3 billion market cap.

Importantly, the company also continued to chip away at its debt load it accumulated during the pandemic. billion in debt, while repricing another $2.7 The company also issued $535 million in notes maturing in 2030 to pay off its 2026 unsecured notes, extending its debt maturities. In the second quarter, Carnival paid down $1.6

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, climbed 10% to nearly $2.4 Over the past five years, Enterprise has averaged about a 13% return on invested capital, so these growth projects should provide meaningful growth to the company in the years ahead.

This resulted in higher realized iron ore premiums, but more importantly, higher margins and returns on invested capital. They should rather be treated as a type of debtamortization. As you can see on the next slide, our expanded net debt remained stable at $16.5 billion in the quarter. billion in the quarter.

After seeing the company saddled with over $39 billion in debt during a rising interest rate environment, the market seems to be taking a more cautious approach to American Tower's stock. Furthermore, 85% of its debt has fixed interest rates, making it less susceptible to today's interest rate hikes.

The trifecta to be achieved by the end of 2025 seemed ambitious at the time: Royal Caribbean was aiming to top $100 in adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) per available passenger cruise day. This would shatter its pre-pandemic record of $87 in 2019. Its previous record was 10.5%.

An excellent way to quantitatively answer this question is to compare its return on invested capital (ROIC) to its peer group, as historically, companies with a higher ROIC have tended to perform better over time. ROK Return on Invested Capital data by YCharts.

Doximity says its customers get exceptional return on investment from marketing on the app, and the company has historically turned that into upsell opportunities for more marketing -- and, more recently, the upsell of app extensions like video conferencing and e-signature.

But its debt-to-equity ratio at 0.65 The company estimates it could generate an additional $300 million of annual adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) from this business in the coming years. CVX Dividend Per Share (Annual) data by YCharts. times is still dramatically higher than Chevron's 0.12

Management believes these acquisitions now grow sales by more than 10% annually, generate more than $3 billion in annualized sales, and maintain an adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margin of 20%.

This three-year strategy -- introduced in June 2023 -- is a comprehensive approach aimed at bolstering Carnival's financial health, as indicated by improvements in earnings before interest, taxes, depreciation, and amortization ( EBITDA) and return on invested capital ( ROIC). billion and a significant reduction in debt by $4.6

Beginning this quarter, in addition to our GAAP measures, we are providing the following non-GAAP measures: adjusted operating income, adjusted operating margin, and adjusted diluted earnings per share, which excludes noncash amortization of acquired intangible assets. Our operating margin for the second quarter was 15.1%, compared to 15.4%

In line with our stated financial strategy after funding our dividend, Core continued to dedicate free cash to paying down debt. During the quarter, Core's net debt was reduced by $15.8 This reduction in our outstanding debt also decreased our leverage ratio to 1.66, down from 1.76 million, net debt was $132.3

In line with our stated financial strategy, after funding our dividend, Core continued to dedicate free cash to paying down debt. During the third quarter, Core's net debt was reduced by nearly $12 million or 9%. This reduction in our outstanding debt also decreased our leverage ratio to 1.47, down from 1.66 last quarter.

compounded annually, which will allow us to use our cash flow generation to pay down debt and rebuild the balance sheet as we work toward investment-grade leverage metrics. During the quarter, we used excess liquidity to opportunistically prepay over $1 billion of debt while still retaining $7.3 billion off the peak.

That's the ratio of net unsecured debt to adjusted EBITDA. Our focus is to continue to pay down debt between now and the closing of the Frontier deal. As we work toward that target, we continue to focus on generating strong cash flows and paying down debt. We're still facing headwinds with primary amortization.

We are working to pivot our business toward a model that will streamline our operations and sell nonstrategic assets, improve the consistency of our earnings, increase EBITDA and dividends per share, reduce debt, rightsize the balance sheet, and improve the return on invested capital. Long-term debt as of July 31, 2023 was $40.7

The growth was primarily driven by a larger base of operating studios, which contribute to a higher number of franchise license revenue being amortized in addition to higher royalties generated by the increase in systemwide sales and positive same-store sales growth. Depreciation and amortization expense was $4.2

This includes everything from equipment and inventory to debts and loans. The capitalization rate is determined by dividing the expected rate of return on investment by the risk-free rate of return. Subtract the value of the business’s liabilities, including debts and loans.

We will also offer some perspective on our strengthened balance sheet position with the recent divestiture of one of our noncore businesses, which underscores our focused product strategy and our commitment to driving a strong return on invested capital. Our senior-term debt is now $92.7 We drove a 125% IRR and 9.5

In the factory, we're beginning to see early returns on investments in production, including robotics, our patented automated mold polishing process, and machine perception in our quality verification process. million of cash and investments on our balance sheet and zero debt. On March 31st, 2024, we had $112.9

The decrease in GAAP gross profit was driven by the impacts of the NuVasive merger, namely step-up inventory amortization. Adjusted gross profit, which excludes the impacts of inventory step-up amortization, was 65.5%. in the prior year, driven again by the impact of step-up amortization as a result of the NuVasive merger.

At the same time, we continue to execute on our key financial strategies including reducing net debt and strengthening our balance sheet. Depreciation and amortization for the quarter was 3.9 On the liability side of the balance sheet, our long term debt was $185 million at June 30th and considering cash of 22 -- 26.2

Trades around 55 times free cash flow, 31 times enterprise value to forward EBITDA so the value of its debt and equity compared to its forward earnings. What it might be going on here is a bit of investment. When you invest in your capital base and make it bigger, that lowers your return on invested capital.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content