This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

And many of the biggest companies in the industry are happy to return that cash to shareholders. billion to shareholders over the last 12 months. billion to shareholders over the past year. But one of its biggest competitors has returned even more cash to shareholders. It sports a 5% dividend yield, paying out $8.2

The Canadian pipeline company just announced another raise for shareholders in 2024, bringing it to 29 straight years of dividend increases. EBITDA = earnings before interest, taxes, depreciation, and amortization. That should translate into those annual dividend increases for shareholders.

While oil prices have an effect on Occidental's cash flows, it has several catalysts unrelated to oil that could boost shareholder value in the future. Sign Up For Free Rapidly repaying debt Occidental Petroleum made a needle-moving acquisition last year, closing its $12 billion purchase of CrownRock. Start Your Mornings Smarter!

This is thanks, in part, to Carnival's fantastic earnings performance, but another element may be even better news for shareholders. Carnival's wall of debt First, let's take a quick look back in time at the challenges Carnival faced in recent years. Carnival also has prepaid debt, for example prepaying $7.3

Carvana risked bankruptcy because it operated at a loss, funded its business with low-interest debt that was no longer available, and stuffed its sales channels with used car inventory right as consumer demand slowed. Fortunately for shareholders, Carvana's management renegotiated some of its debt. Here's why.

Before the deal Enbridge generated 57% of earnings before interest, taxes, depreciation, and amortization (EBITDA) from oil. That's because a quarter of its debt has a floating rate, meaning the interest expenses on this debt rise and fall with rates. After the deal that will be down to 50%.

Why the stock scares off some investors The debt-to-equity (D/E) ratio of DigitalOcean is a negative 675% due to total debt of $1.47 billion and negative shareholder equity of $217.7 You can calculate it by dividing the company's total debt by shareholder equity. On the one hand, the company has high debt.

Buying shares of businesses that produce profits and commit to returning those profits to their shareholders is an investing strategy with a terrific track record. Shares of the phone and internet service provider have fallen about 23% in 2023 as investors worry about a high debt load and potential litigation regarding lead-lined cables.

In his 1988 annual letter to shareholders, Buffett penned that when it comes to owning outstanding businesses with excellent management, "our favorite holding period is forever." As for why Buffett's love grew for Apple, the company returns an incredible amount of capital to its shareholders in the form of dividends and share buybacks.

Once they make such a commitment, returning a portion of profits to shareholders forces management teams to make smarter decisions. AT&T finished September with $129 billion in net debt. 30 and it's using these profits to reduce debt. The average yield it receives on debt has risen sharply from 8.7%

They buy dividend-paying stocks because they know that companies committed to returning a portion of earnings to shareholders tend to outperform ones that don't. Strong cash flows have management thinking it can reduce its debt load from 2.9 Billionaire investors generally don't necessarily need dividend income to make ends meet.

I've seen numerous companies harm shareholders with massive debt-fueled acquisitions that put the balance sheet in peril. While Illinois Tool Works leans on debt, it doesn't do so too heavily. Today, the company has a reasonable debt-to- EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio of 1.8.

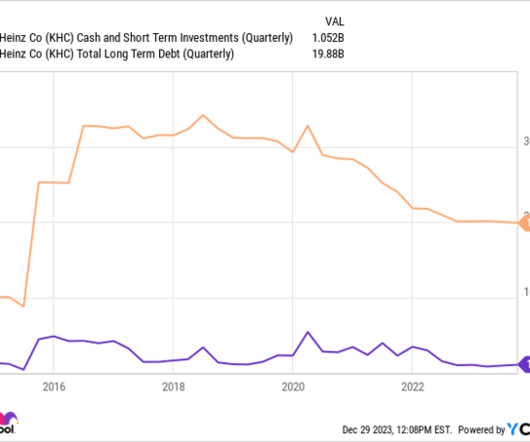

Here are three reasons why the future looks bright for Kraft Heinz and its shareholders in 2024 and beyond. However, the merger also loaded up the new entity with debt. Below, the merger more than tripled the company's debt to over $30 billion. Is it stubbornness? Is it perfect yet? But management has brought leverage down to 2.9

On the bright side, Walgreens' healthcare segment, which delivers treatment direct to consumers, generated adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA ) of $23 million for the first time in Q3. billion in debt while issuing $24.1 And, with $33.6 Over the last 12 months, it repaid $26.8 billion more.

As a REIT, Medical Properties Trust can avoid paying income taxes by distributing at least 90% of earnings to shareholders as dividends. This is another type of investment vehicle that avoids income taxes by returning most of its profits to shareholders. of the total investment portfolio at amortized cost.

However, due to the $6 billion in long-term debt it took on to fund that purchase, the market has taken a cautious view toward Nasdaq's stock, and it remains below its pre-acquisition announcement price. Armed with this growing FCF creation, management aims to lower Nasdaq's debt load from 4.3 With its $10.5 times within three years.

He also said while the company didn't need to raise additional capital, a rising stock price would make it easier to do so without significantly diluting shareholders. year over year, its lowest rate since October 2021. Overall, those numbers show inflation cooling faster than expected.

Companies that dole out a dividend to their shareholders on a regular basis tend to be recurringly profitable and time-tested. BDCs are businesses that invest in the debt and/or equity (common and preferred stock) of middle-market companies, which are generally unproven small- and micro-cap enterprises. Image source: Getty Images.

It had no revenue and was taking on huge debt. That led to earnings before interest, taxes, depreciation, and amortization ( EBITDA ) to rise 5% per unit from 2019 levels despite interim inflation. The main risk now lies in its debt repayment. There's still plenty of room to move up, and 2024 might be the best time to buy.

Basically, through thick and thin, the MLP has made sure that its shareholders receive a steady and growing quarterly disbursement. For example, its ratio of debt to EBITDA ( earnings before interest, taxes, depreciation, and amortization ) is generally among the lowest of its closest peer group.

After announcing a trifecta of improving earnings numbers, a debt restructuring, and an at-the-market (ATM) stock offering last week, shares of the online used car marketplace are now up about 780% year to date and were, at one point, up over 1,000%. Well, Carvana (NYSE: CVNA) has had an interesting last few years. However, with around $6.5

Here's what GE shareholders need to know about the company, which will receive stock soon. The table below breaks out organic earnings before interest, taxation, depreciation, and amortization ( EBITDA). The change will create two dramatically different companies, with GE Vernova arguably being the most interesting, albeit the weaker.

The company took on a lot of debt during the pandemic and diluted shareholders. billion in adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) -- and $31 billion in debt. billion through the first three quarters of the year, which management is committing to use to pay down that debt.

shareholders that “when we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever.” He clarified his position in his 2016 letter to shareholders: “It is true that we own some stocks that I have no intention of selling for as far as the eye can see (and we’re talking 20/20 vision).

The company now holds a significant amount of debt. Management plans to divest non-core assets to accelerate the paydown of that debt. He called her "an extraordinary manager" at Berkshire's 2023 Shareholder meeting in May. Occidental's big investments in the Permian Basin have put pressure on its balance sheet.

Adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), which measures the underlying health of core activities, came in at $681 million, above guidance, and management is expecting that to more than triple in the third quarter. However, it's managing the debt quite effectively, and it's $1.4

billion in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and $1.2 The good news is that I saved some of the more potent aspects of the bullish argument for the end to justify at least holding Sirius XM if you are already a shareholder. It has posted an annual profit every year since 2010.

in net debt to earnings before interest, taxes, depreciation, and amortization ( EBITDA ). Further evidence of Franco-Nevada's appeal for conservative investors comes from the stock's rock-solid balance sheet that features zero debt and $1.3 Currently, investors can grab shares of Agnico Eagle from the bargain bin.

WM Cash from Operations (TTM) data by YCharts Despite this ramped-up capex spending, Waste Management remains FCF positive, returning $283 million in dividends and $370 million in stock buybacks to its shareholders during the third quarter. ROIC shows that it is the best in its industry at reinvesting in its business.

It's financially healthy: The nearly $17 billion in debt on its balance sheet is just 1.7 times the business' earnings before interest, taxes, depreciation, and amortization ( EBITDA). All of this points to a reliable company that allows shareholders to sleep well at night. But there are some positive signs.

I am incredibly excited about this acquisition, which enhances our footprint in some of the most bet-upon sports, including tennis, soccer, and basketball, and will deliver significant value to our clients, partners, and shareholders. The deal, once closed, is expected to be immediately accretive to our business and margins.

These specialized investment vehicles can avoid paying income taxes by distributing at least 90% of their profits to shareholders. Middle-market companies are generally willing to pay higher interest rates than their larger peers and accept debt at floating rates. a year earlier. a year earlier. a year earlier.

Companies that regularly dole out a dividend to their shareholders are often profitable on a recurring basis, time-tested, and capable of offering transparent, long-term growth guidance. Since March 31, 2022, AT&T's net debt has declined from $169 billion to $128.9 million in net debt, its net-leverage ratio is a modest 0.31.

There was $129 billion in net debt on AT&T's balance sheet at the end of September, which isn't as frightening as it might seem. The company expects to achieve a manageable net debt-to-adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA) ratio of 2.5 million in net unsecured debt.

Should these upgrades go according to plan, management believes its earnings before interest, taxes, depreciation, and amortization (EBITDA) margin -- lately 9% -- will improve to 14% by 2026. Its dividend at the current share price has a generous 3.7%

During the third quarter, we continued to advance our strategy of generating additional liquidity to accelerate debt paydown and enhance financial flexibility. We continue to take meaningful action that better positions our business to create compelling shareholder value over the long term. billion in debt. Turning to our U.S.

The company invested heavily and is still servicing an enormous debt. billion in net debt. At the end of March, the telecom giant's net debt pile equaled 2.9 times adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). AT&T says it's on track to shrink its debt-to-EBITDA ratio to 2.5

A company must grow its earnings to distribute more money to shareholders over time. WM (NYSE: WM) , ExxonMobil (NYSE: XOM) , and Owens Corning (NYSE: OC) are three businesses that generate near-record-high earnings and use the dividend as an important way to reward patient shareholders. billion, ExxonMobil reported $83.1

Growth stocks can generate sizable gains for their shareholders. If you have some money you'd like to invest in this wealth-building asset class -- that you don't need for living expenses or to pay off debt -- read on to learn about two great growth stocks. You can buy shares in both companies for less than $100 today.

The gross-margin improvement led to strong increases in profitability metrics, with adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) surging 64% year overyear to $144.8 It ended the period with $695 million in cash and marketable securities and no debt.

billion) in 2025, all while working to bring its net debt to adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) ratio down to a range of 2.0 The company plans to spend 700 million pounds (about $889 million) on buybacks this year and 900 million pounds (about $1.1 by the end of this year.

In the second quarter, adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) increased by 2.6%, while free cash flow of $4.6 Long plagued by a heavy burden of liabilities, AT&T is managing to deleverage with a decline in net debt supported by positive free cash flow. billion was up $0.4

Some of this gain was fueled by a big jump in the share price this week as the company reported better-than-expected revenue and significant positive adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). billion in long-term debt. Its valuation, at this stage, is extraordinarily difficult to justify.

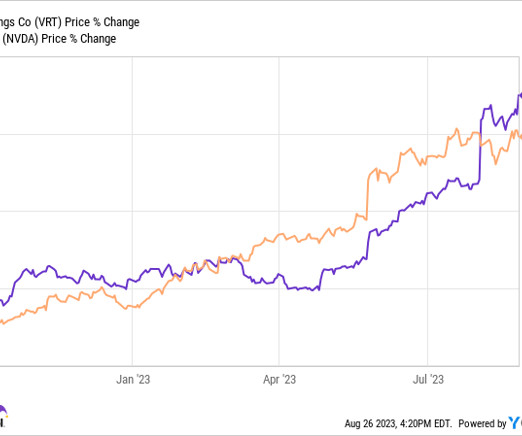

Vertiv also has a significant amount of debt, which stood at around $3 billion at the end of last quarter, against just $275 million in cash. times adjusted EBITDA (earnings before interest, taxes, depreciation and amortization), but that it should go down to 2.3 The company noted that current leverage is at 3.1 Probably not.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content