This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

However, the robust growth prospects of its data center/AI-related business shouldn't detract from the strength of its underlying growth driver coming from the retrofit opportunity in commercial buildings as it seeks to improve efficiency and meet its net zero emissions aims. Data source: Johnson Controls presentations. Chart by author.

The stock is down 95% from the all-time high it hit three years ago when the growth prospects for the leading provider of remote medical consultations were far kinder. The transaction was valued at $18.5 Today you can buy all of Teladoc at an enterprisevalue barely above $3 billion. billion at the time.

It might have balance sheet issues, lack growth prospects, or have a more complex corporate structure. Energy Transfer: A low value gives it a high yield Energy Transfer expects to generate $13.1 billion of adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) this year. billion to $13.5

On an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) basis, it generated a profit of $3.3 Nevertheless, investors should still take into account Carnival's debt -- which is reflected in its higher enterprisevalue instead of its lower market capitalization -- when valuing its stock.

At its current price, it trades near the high end of its historical enterprisevalue -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) range, excluding the impact of the COVID-19 pandemic. That said, the stock's valuation has grown to reflect the company's strong prospects.

But Buffett would describe the prospects for Coca-Cola as “better than the average American corporation.” and an enterprisevalue -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) ratio of 6, the shares are trading at a fair value. which is roughly in line with the S&P 500.

The company claimed it could deliver a compound annual growth rate (CAGR) of 40%, taking revenue from $140 million in 2020 to $388 million in 2023 while expanding its gross margin from 30% to 50% and keeping its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margins in the high teens.

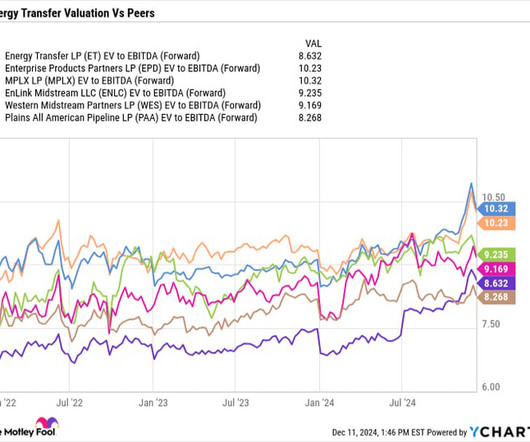

Approximately 90% of Energy Transfer's 2024 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) is projected to come from fee-based activities. I typically use an enterprisevalue- to- EBITDA multiple to value midstream stocks. Should you invest $1,000 in Energy Transfer right now?

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprisevalue (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 It and Enterprise also have the most attractive yields of the group at 8.1% and 7.2%, respectively.

The company typically looks for at least a 12% return on its spending, which would help boost earnings before interest, taxes, depreciation, and amortization (EBITDA) by more than $370 million per year once all the projects are fully ramped up. It plans to spend around $3.1 billion on growth projects this year. The reason for this is twofold.

These growth drivers have the MLP on track to increase its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) by 12% at the midpoint of its guidance range this year. Further, as noted, the MLP has strong growth prospects that are growing stronger. times target range. per share by 2027.

Let's look at the company's most recent quarterly results, future prospects, and valuation to see if this is a good time to buy the beaten-down stock. It also said that it is seeing success in newer verticals such as enterprise restaurant chains and food and beverage retailers. billion and an enterprisevalue (EV) of about $11.9

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). Should you invest $1,000 in Enterprise Products Partners right now?

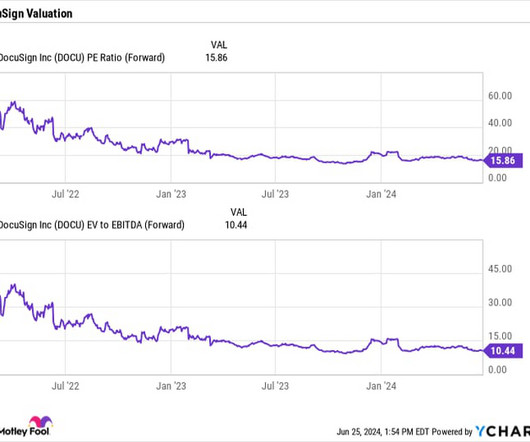

billion in net cash and marketable securities on its balance sheet, the stock trades at an enterprise-value -to-forward-sales ratio of just 3.6 That's just plain cheap for a software company that is still growing nicely and has strong potential prospects ahead. Taking into consideration the $1.9 the stock is cheap.

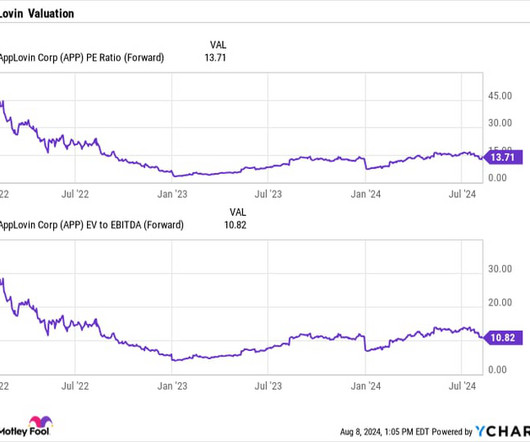

Adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, soared 80% to $601 million. Gross margins for the quarter came in at 73.8%, a huge jump from 65.5% a year ago. In the second quarter, AppLovin's net income nearly quadrupled from $80 million to $309.9

The growth prospects aren't very appetizing Cracker Barrel's management already has a pretty detailed long-term vision in place. Cracker Barrel's growth prospects aren't inspiring. In fiscal 2027, it hopes to earn adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) of about $400 million.

However, management is forecasting a profit on an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) basis by the end of 2025. The business reported an adjusted net loss of $4 million last quarter, but that's where Nvidia's recent investment is pivotal for Applied Digital's growth prospects.

Lockheed Martin's valuation That said, every stock has its value, and a quick look at Lockheed Martin's valuation suggests it's being priced with some pretty positive assumptions in mind. In addition, on a price-to-free cash flow basis, the stock trades at slightly less than 22 times Wall Street estimates for free cash flow (FCF) in 2024.

Let's take a closer look at the midstream company's Q2 results, distribution, long-term prospects, and whether now is a good time to buy the stock. For Q2, the Enterprise saw its total gross-operating margin increase nearly 11% to $2.4 It generated distributable cash flow of $1.8

Let's look at the company's most recent quarterly results, future prospects, and valuation to find the answer. The company reported $57 million in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) , compared to a negative $17 million a year ago. With an enterprisevalue (EV) of about $13.7

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) also improved from negative $94 million in 2022 to positive $536 million in 2023. Robinhood's prospects are brightening, but investors shouldn't overlook its weaknesses. With an enterprisevalue of $23.4

The investment case for Siemens rests on the idea that its mobility business (rail rolling stock, rail infrastructure, and services) and Siemens Healthineers are relatively stable businesses with good growth prospects through the economic cycle. WHR Days Inventory Outstanding (Quarterly) data by YCharts.

It has also received requests from more than 40 prospective data centers in 10 states that could use 10 BCF a day of natural gas. Attractive valuation Besides having some of the best growth opportunities in the pipeline space, Energy Transfer is also one of the most attractively valued MLPs. Image source: Getty Images.

The debt will take Owens Corning to a net debt-to-earnings before interest, taxation, depreciation, and amortization (EBITDA) multiple of 2 to 3 times EBITDA, dropping to around 2 times at the end of 2024. The deal values Masonite at an enterprisevalue (market cap plus net debt) of 8.6 times adjusted EBITDA, or around 6.8

Buyers who purchase items through Etsy's mobile app have a 40% higher lifetime value, making this ongoing shift very important to its prospects. In Etsy's case, customer lifetime value equals the present value of all the future revenue it would generate from a given user.

Do you feel good about T-Mobile's prospects moving forward with that or is that something that you're wary of? That is enterprisevalue to earnings before interest, tax, depreciation, amortization. Jason Moser: I think on the whole you have to be you have to feel pretty good about this.

Interestingly, Dassault trades at a current enterprisevalue (market cap plus net debt), or EV, to earnings before interest, taxation, depreciation, and amortization ( EBITDA ) valuation of nearly 30. That's a reasonable valuation for a company with excellent long-term growth prospects.

This helps support the franchise, generates great returns for the house, and should increase enterprisevalue for both Sculptor and Rithm at the top of the house. Very excited for the prospects of that business. On the amortization front, if you look at the slides, I think amortization came in roughly at 6 CPR.

As you think about all these comments, we're super excited where we are with the business and the prospects for the future. billion, just to give you a sense, is now down to $800 million, it amortizes extremely quick. This was anchored by a commitment from Rithm. In the quarter, we priced two CLOs, one in Europe and one in the U.S.

This in itself should drive long-term enterprisevalue creation through earnings outperformance. The Compass reverse prospecting tool is a powerful new tool that enables agents and their homeowners to identify which of the 33,000 Compass agents and their millions of buyers have viewed, shared, favorited or commented on their listing.

We continue to ramp this channel onboarding our third embedded partner in signing three new partners to effectively scale for an increasing pipeline of prospective partners, we continue to develop this channel by expanding our team capacity, establishing partner frameworks in developing sales enablement tools to drive mutual success.

Our total debt to enterprisevalue was approximately 30% while our fixed charge coverage ratio, which includes principal amortization and the preferred dividend, is very healthy at 4.9 As of the end of the quarter, pro forma for the settlement of our outstanding forward equity, net debt to recurring EBITDA was approximately 4.3

As we enter the back half of '23, we remain bullish on our full-year prospects and believe we are well-positioned to achieve continued overall record revenues for the full year. Depreciation and amortization expense increased to $1 million for the three months ended June 30, 2023, versus $0.4 million in the prior year's period.

Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) and free cash flow ( FCF ) also turned positive in 2023 as it streamlined its spending. Based on these expectations and its enterprisevalue of roughly $8 billion, Roku's stock looks reasonably valued at less than 2 times next year's projected sales.

However, with an enterprisevalue of $21.6 That's why Toast's adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) finally turned positive in 2023 and grew more than eightfold year over year in the first nine months of 2024. billion,Toast looks pretty cheap at 3.5 times next year's sales.

Does Alphabet have below-average long-term prospects? billion in adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ). Considering it has an enterprisevalue of $62 billion, it trades at just 10 to 11 times this year's EBTIDA. Those are quality financial results as far as I'm concerned.

However, its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) broadly missed its initial expectations. With an enterprisevalue of $268 million, it looks dirt cheap at less than 1 times this year's sales. Are brighter days ahead for EVgo? billion loan facility from the U.S.

First, here's how Honeywell stacks up against the named comparable aerospace companies in terms of forward enterprisevalue, or EV (market cap plus net debt), to earnings before interest, taxation, depreciation, and amortization ( EBITDA ). As such, investors must be patient and hope management can improve earnings over time.

However, the underlying strong business prospects of those stocks still make them great picks for long-term investors. But have ExxonMobil's long-term business prospects faltered? Graham also knew, though, that business fundamentals matter over the long term. Sometimes, investors' "votes" temporarily cause good stocks to decline.

Their growth prospects Enbridge projects adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) between CA$19.4 Over the longer term, the growth prospects for these two companies should be similar because they face many of the same industry dynamics and opportunities. impact Enbridge's business?

It might seem prudent to take some profits after that massive rally, but Wall Street remains bullish on its growth prospects. With an enterprisevalue of $1 billion, Intuitive still looks like a bargain at 4 times this year's sales and just 2 times its estimated sales for 2026.

As a rough assumption, a price-to-earnings (P/E) ratio of around 15 times earnings and an enterprisevalue (market cap plus net debt) to earnings before interest, taxation, depreciation, and amortization of around 11 times EBITDA can be seen as a decent value for a mature company. Start Your Mornings Smarter!

million, and its adjusted earnings before interests, taxes, depreciation, and amortization (EBITDA) fell by 6% in the same period, arriving at $83.3 Looking at its valuation, its enterprise-value -to-revenue multiple (EV/R) is just 0.9. Compared to a year ago, its third-quarter revenue was down 3%, reaching $640.5

The company is looking for 2025 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) to be between $7.2 Energy Transfer is also one of the cheapest stocks in the midstream space with an enterprisevalue (EV)- to-EBITDA multiple of just 8.7 This is a pipeline that just keeps giving. billion and $7.6

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content