This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The leading North American pipeline and utility operator generates very durable cash flow and has very visible growth prospects. Enbridge currently gets 98% of its earnings before interest, taxes, depreciation, and amortization (EBITDA) from stable cost-of-service or contracted assets. times target range.

The sector has gone through a transformation in the past decade, with midstream companies reducing leverage and being more disciplined when it comes to funding growth projects. Even better, the company has said it could pay excess distributions once its leverage is below 3 times and it has excess free cash flow.

It might have balance sheet issues, lack growth prospects, or have a more complex corporate structure. billion of adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) this year. Many factors can cause a company to trade at a relatively lower valuation. They're both publicly traded limited partnerships.

KMI Financial Debt to EBITDA (TTM) data by YCharts That said, a part of the problem was Kinder Morgan's more aggressive use of leverage than its peers'. Kinder Morgan's leverage is lower today, but it still tends to use more leverage than Enterprise.

It recently added more fuel to its growth engine by making a $2 billion acquisition that will supply it with incremental cash flow while enhancing its growth prospects. The company is paying about 10 times estimated 2024 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) for these assets. billion to $6.8

Analysts expect its revenue to grow at a CAGR of 33% from 2022 to 2025, and for its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) to rise at a CAGR of 54%. Image source: Getty Images. All of those strengths make it a great play on the long-term expansion of the cloud, cybersecurity, and AI markets.

I've also included its adjusted debt to earnings before interest, taxation, depreciation, amortization, and rent ( EBITDAR ) multiple. This is a typical leverage ratio that debt investors use for gauging credit quality, demonstrating Delta's creditworthiness improvement. Using cash flow to pay down debt (adjusted debt fell from $32.9

billion in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and $1.2 However, growth prospects haven't improved as the country returns to normal. Sirius XM is also starting to pay down its long-term debt since that bearish leverage peaked in 2022. The model works. It expects to generate $2.7

BigBear.ai (NYSE: BBAI) and SoundHound AI (NASDAQ: SOUN) are two small-caps attempting to leverage unique AI-powered applications into long-term growth. The company reported a loss on Q2 adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of $3.7 Image source: Getty Images. The case for BigBear.ai

But some top consumer-oriented companies quietly delivered market-beating gains and still have bright prospects. Looking ahead to 2024, Carnival expects adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) to reach $5.6 billion, and it expects adjusted net income of $1.2

In fact, management thinks that Carnival will produce adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of $4 billion (at the midpoint) this fiscal year. However, there are reasons for investors to be optimistic about this top auto stock 's prospects. That's quite the turnaround from last year.

The best way to ensure you're always a step ahead of Wall Street is to hold shares of quality companies with great prospects for long-term growth. The stock has good prospects to beat the market again. After a disappointing year for stocks in 2022, the markets have rebounded this year. billion-$4.25

On an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) basis, it generated a profit of $3.3 That leverage gives Carnival a high debt-to-equity ratio of 4.6. But as its business recovered, it narrowed its net loss to $6.1 billion in the first nine months of fiscal 2023, compared to a loss of $1.6

The company claimed it could deliver a compound annual growth rate (CAGR) of 40%, taking revenue from $140 million in 2020 to $388 million in 2023 while expanding its gross margin from 30% to 50% and keeping its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margins in the high teens.

Low historic industry valuations Between 2011 to 2016, midstream companies on average traded at an enterprise value (EV) -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) multiple of over 13.5 Today, multiples throughout the industry are much lower. However, its stock does trade at a premium to its peers.

Approximately 90% of Energy Transfer's 2024 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) is projected to come from fee-based activities. When Energy Transfer cut its distribution in 2020, it was because its leverage became too high, and it needed to pay down debt. cents is now higher than the 30.5

That's exactly when and why you should step into a position in a company with real prospects like Chewy, however. better than 2021's sales, and despite brisk inflation being a problem for the better part of the year, Chewy pumped up 2021's earnings before interest, taxes, depreciation, and amortization (EBITDA) from $78.5 billon is 13.6%

In addition to the opportunity to increase sales and ultimately realize further growth in the pOpshelf banner, we are also able to leverage learnings from this banner and apply them in our non-consumable categories in our Dollar General stores to further strengthen that offering for our DG customers.

It has continued to reduce its leverage and now plans to finish the year with a net debt-to-adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ratio of just 3.9. yield, another factor driving Kinder Morgan is its future earnings prospects.

What current and prospective investors should be focused on is AT&T's steadily improving operating performance. million in net debt, its net-leverage ratio is a modest 0.31. This should help the company's oil and gas royalty segment bring in higher earnings before interest, taxes, depreciation, and amortization ( EBITDA ).

Revenue increased 27% year over year, and adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) increased 121% to $98 million, driven by increases in non-lending segments. It's leveraging tremendous economies of scale, and it's now sustainably profitable with increasing operating margins.

Meanwhile, the company ended the first quarter with 3 times leverage, which it defines as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted interest, taxes, depreciation, and amortization ( EBITDA ). This has come down from the over 4 times leverage it was at in 2017.

Upstart bounces back Upstart, which uses an AI-based model to screen prospective lenders to better assess creditworthiness and default risk, has struggled with the high-interest-rate environment like most lending platforms. As of 12:51 p.m. ET, the stock was up 48.6%. Image source: Getty Images.

As disclosed earlier in the third quarter, First Solar also possesses a TOPCon patent portfolio through our acquisition of TetraSun in 2013, which we have begun to leverage as part of our ongoing efforts to develop the next generation of PV technologies. Have you fully remediated the backdrop here around the $50 million warranty liability?

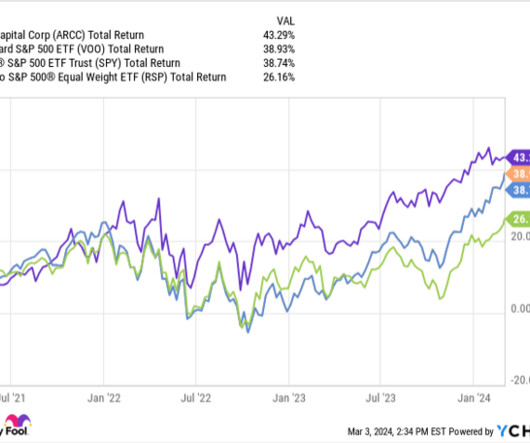

The company specializes in more complex transactions such as leveraged buyouts , for example. Revenue, EBITDA (earnings before interest, taxes, depreciation and amortization), and free cash flow saw some dips that resulted in a modest sell-off of the stock. Given its size, Ares also has more financial flexibility than a typical BDC.

These growth drivers have the MLP on track to increase its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) by 12% at the midpoint of its guidance range this year. Meanwhile, its leverage ratio is trending toward the low end of its 4.0 times target range. per share by 2027.

The company has won over investors excited about its strong financial performance and growth prospects. million in annual sales volume, with an outstanding restaurant-level earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margin of 26.5% (this figure excludes corporate expenses). Cava generated $16.1

Adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) surged 39% to $180 million. The Trade Desk's prospects in the next few years The Trade Desk executed well over the last few years, growing revenue by 412% from $308 million in 2018 to $1.6 Discovery and Walmart , to its list of partners.

Let's take a closer look at the midstream company's Q2 results, distribution, long-term prospects, and whether now is a good time to buy the stock. Its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, climbed 10% to nearly $2.4 It ended the quarter with leverage of 3 times.

While this industry has proven to be more cyclical than investors had hoped, its long-term prospects are favorable. The company was able to post positive adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) and free cash flow in three straight quarters, a streak that's still active.

This year, management believes Cava will produce adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of $89 million (at the midpoint), which would be higher than last year's total. In theory, Cava should be able to better leverage some of its fixed expenses, like corporate overhead and marketing costs.

The company's balance sheet is currently in good shape, with leverage (as used by rating agencies) toward the low end of its 4x to 4.5x EV to EBITDA = enterprise-value-to-EBITDA (earnings before interest, taxes, depreciation, and amortization). target range. times distribution coverage ratio in the second quarter.

For origination, we leverage relationships across all our divisions to identify new opportunities while our global presence and deep-rooted partnerships with sponsors, corporates, advisors, and bankers help us create a high-quality funnel of deals. LTV refers to the approximate leverage through leveraged loans utilized to finance U.S.

Roughly 98% of its earnings before interest, taxes, depreciation, and amortization (EBITDA) comes from cost-of-service or contracted assets, which are highly stable and predictable. The company also has a strong investment-grade balance sheet backed by a leverage ratio currently in the lower half of its 4.5 times target range.

Stocks of companies with excellent growth prospects typically sell at expensive valuations, which will cause the share price to fall when the company experiences a hiccup in revenue or earnings growth. Another positive sign for investors is that Celsius continues to leverage costs to grow profits at high rates.

Profitability has risen at an even faster pace, showing the operating leverage in the company's business as it gains scale. Adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ), meanwhile, soared 80% to $601 million. Gross margins for the quarter came in at 73.8%, a huge jump from 65.5% a year ago.

Notably, leverage is back to manageable levels, with the company's debt-to-EBITDA ( earnings before interest, taxes, depreciation, and amortization ) ratio of around 3.6 Leverage is right in line with management's target as well, which allows the company to shift from defense to offense. back in line with its peers.

Most notably and uniquely, our lower middle market strategy provides attractive leverage points and income yield on our first-lien debt investments while also creating a true partnership with the management teams and other equity owners of our portfolio companies through our flexible and highly aligned equity ownership structures.

Just as important as the revenue growth, the company has also seen a lot of operating leverage in its business as well, which is leading to even stronger profitability growth. a year ago to $1.25, while its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) soared 72% to $722 million. from 69.3%

Let's take a closer look at the cosmetic company's most recent results and prospects to see if now is a good time to buy the stock. Adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) increased 9% to $146.8 And since the fiscal 2025 second-quarter earnings release on Nov. but easily surpassed the $0.43

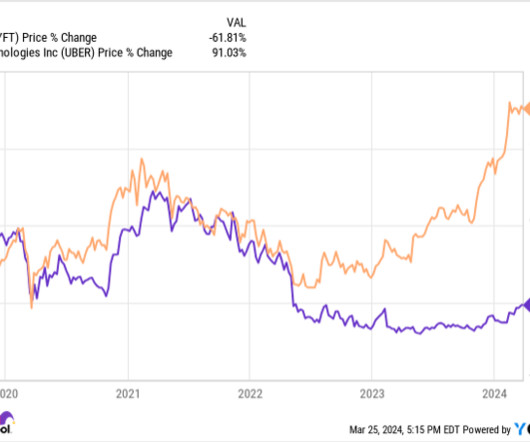

Why Lyft is not (necessarily) the same as Uber To evaluate its turnaround prospects, investors need to understand the differences between Uber and Lyft. And through its larger size, Uber has better leveraged such improvements to its advantage. Let's venture to find out. For one, Lyft has so far limited itself to one country.

billion of adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) last year. Meanwhile, it has a strong investment-grade balance sheet, with its leverage ratio in the lower half of its target range of 4 to 4.5 If anything, Energy Transfer's growth prospects have only gotten stronger over the past year.

Customers using the platform are actively leveraging our advanced AI features and, more importantly, finding real value in them. Cost of revenues decreased by $6 million, or 53%, in Q4, primarily due to previous technology-related amortization expenses that became fully amortized in 2024. R&D decreased by $1.1 million or 6%.

Notably, the second quarter of 2023 marked DraftKings' first quarter of positive adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA), a milestone that strengthens its standing in the market. This efficiency-oriented approach has been instrumental in driving the company toward profitability.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content