This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Additionally, Starbuck's net income declined 15% from $908 million a year ago to $772 million in the latest quarter as its operating expenses, depreciation and amortization expenses, and general and administrative expenses all increased. That marked a 2% year-over-year decline, partly attributed to a 6% decrease in transactions.

billion in adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and $1.2 However, growth prospects haven't improved as the country returns to normal. The real star in returning money to shareholders has been its share buybacks. It has posted an annual profit every year since 2010. The model works.

shareholders that “when we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever.” He clarified his position in his 2016 letter to shareholders: “It is true that we own some stocks that I have no intention of selling for as far as the eye can see (and we’re talking 20/20 vision).

Industries such as e-commerce and fintech have terrific prospects, too, and the leaders in these spaces could deliver outsize returns over the long run. But beyond that, the company's prospects are attractive. That'll allow Adyen to remain a leader in fintech for a while while delivering solid returns to its shareholders.

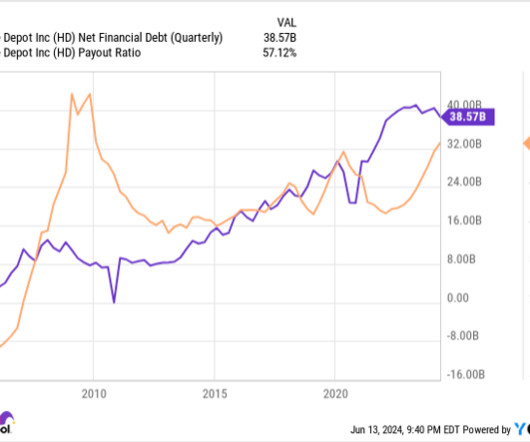

All told, Home Depot's dividend (current yield 2.6%) is sustainable and has growth prospects as the housing market improves. Having raised its dividend for 27 consecutive years, York Water certainly warrants respect for increasing its payout to shareholders. HD free cash flow per share data by YCharts; TTM = trailing-12-months.

We continue to take meaningful action that better positions our business to create compelling shareholder value over the long term. Finally, Prospect's California facilities continue to report growth, driven by admissions and surgeries, which have each increased 3% year over year. This morning, we reported GAAP net loss of $1.34

Phillips 66 has demonstrated consistent interest in rewarding shareholders since it started paying a dividend in 2012. Further evidence of the company's commitment comes in the form of a recent announcement that the company has upwardly revised its target for shareholder distributions. in 2023 to 20% to 23% in 2027.

Perhaps even more encouraging for shareholders is Carnival's path to getting back toward profitability. In fact, management thinks that Carnival will produce adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) of $4 billion (at the midpoint) this fiscal year. That's quite the turnaround from last year.

He will then buy shares and use his influence to unlock shareholder value. At its current price, it trades near the high end of its historical enterprise value -to- EBITDA (earnings before interest, taxes, depreciation, and amortization) range, excluding the impact of the COVID-19 pandemic. billion in public equity holdings.

It's a smart idea to consider what stocks billionaire investors are buying (or selling), and there's no better investor to follow in this regard than Warren Buffett , who has built a mountain of wealth for Berkshire Hathaway shareholders. Meanwhile, the stock still trades within its historical average price-to-earnings (P/E) valuation range.

Deere's capital return program uses both dividends and buybacks to reward shareholders. Deere's payout ratio is just 19%, meaning that if it returned all of its earnings to shareholders through dividends, its yield would be over 7.5%. times earnings before interest, taxation, depreciation, and amortization ( EBITDA ) for Masonite.

It's been a tough past couple of years for Chewy (NYSE: CHWY) shareholders. That's exactly when and why you should step into a position in a company with real prospects like Chewy, however. That's exactly when and why you should step into a position in a company with real prospects like Chewy, however. billon is 13.6%

The best way to ensure you're always a step ahead of Wall Street is to hold shares of quality companies with great prospects for long-term growth. A high-growth restaurant John Ballard (Chipotle Mexican Grill): Chipotle has been a stellar performer for shareholders over the last decade. billion-$4.25

The company claimed it could deliver a compound annual growth rate (CAGR) of 40%, taking revenue from $140 million in 2020 to $388 million in 2023 while expanding its gross margin from 30% to 50% and keeping its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) margins in the high teens.

Since Hercules is a BDC, it's required to pay out 90% of its taxable income to shareholders each year in the form of a dividend. As such, shareholders have cheered the stock for quite some time. I see this as a clear sign of premium shareholder value. Over the last 10 years, Hercules stock has a total return of 230%.

Over the long term, management is guiding for its earnings before interest, taxes, depreciation, and amortization (EBITDA) margin to reach at least 8%. However, unless the company can significantly grow its revenue while also expanding its profitability, it will likely struggle to generate cash it can return to shareholders.

It has continued to reduce its leverage and now plans to finish the year with a net debt-to-adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) ratio of just 3.9. yield, another factor driving Kinder Morgan is its future earnings prospects.

But if you don't have The Trade Desk in your stock portfolio yet, you're missing out on a tremendous growth stock with robust business prospects, both in the near term and over the long haul. Although the stock hasn't performed especially well so far in 2024, I think Enbridge's growth prospects are pretty good.

Even though it's gaining direct-to-consumer (DTC) subscribers, adjusted operating income before depreciation and amortization (OIBDA) for its DTC segment worsened to a loss of $511 million in the March-ended quarter -- 12% worse than the year-ago period. Mature businesses are known for returning capital to patient long-term shareholders.

Approximately 90% of Energy Transfer's 2024 earnings before interest, taxes, depreciation, and amortization ( EBITDA ) is projected to come from fee-based activities. Energy Transfer is structured as a master limited partnership (MLP), so investors will get a K-1 and have unique tax advantages (and obligations).

Companies that regularly dole out a dividend to their shareholders are often profitable on a recurring basis, time-tested, and capable of offering transparent, long-term growth guidance. What current and prospective investors should be focused on is AT&T's steadily improving operating performance. Image source: Getty Images.

Overall, we are proud of the continued progress we're making and are pleased with how it has positioned us to drive profitable sales growth and capture growth opportunities while creating long-term shareholder value. During the quarter, we returned cash to shareholders through a quarterly dividend of $0.59 per share.

Revenue increased 27% year over year, and adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) increased 121% to $98 million, driven by increases in non-lending segments. This perennial market-beating stock also pays a dividend, and it has tons of gas left in the tank to make shareholders rich in the long term.

When a company that most have discarded or ignored changes its fortunes for the better, the prospect of outsize stock returns is large. But adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) fell even more by just over 20%, as the company made increased investments on a declining revenue base.

After falling from around $36 per share to reach near $22 in the last 12 months, there may not be much of a reprieve in sight for shareholders of Walgreens Boots Alliance (NASDAQ: WBA). According to an updated price target issued by financial analyst Daniela Bretthauer at HSBC , the stock could fall even further soon, to $20.

As Home Depot shareholders wait for the deal to go through and the housing cycle to turn around, the company will continue to pay a handsome dividend. billion in adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) annually. But is that enough for the stock to remain healthy?

Enterprise's consistency can also be seen in its distribution to shareholders, which it has been able to grow each year for the past 25 years. Enterprise Products offers a growing distribution with a high yield One of the first things that draws investors to Enterprise Products is its high yield, which is currently 7.3%.

And executives forecast adjusted earnings before interest, taxes, depreciation, and amortization in the 12-month period to be higher than last year. I believe that it's impossible to predict what will happen in the near term, both for executive teams and for shareholders. That's encouraging, but these results are far from guaranteed.

Here's what prospective investors need to know before buying the stock. From 2017 through 2022, Block's gross profit (excluding technology amortization) had grown 598%. As a result, shareholders have had a volatile ride , with the stock reaching as high as $289 per share before falling to about $54 per share today.

million of adjusted EBITDA ( earnings before interest, taxes, depreciation, and amortization ) that was produced, I view this as a terrible gauge of profitability. No growth prospects Peloton's leadership team touts reducing expenses. And when it comes to the $70.3 It excludes many important costs.

Towards the bottom of the income statement, Nikola reported earnings before interest, taxes, depreciation, and amortization (EBITDA) of negative $752.7 Further powering the bears' concerns is the prospect of shareholder dilution. However, it's critical that prospective buyers know the considerable risks of an investment.

A very bankable income stream Enbridge has paid dividends to its shareholders for nearly 70 years , and the pipeline and utility operator has increased its payment for the last 29 straight years. The accretive deal enhanced its diversification and growth prospects. billion over the next three years.

Even companies with solid prospects sometimes fail to keep pace with the market. In some cases, an investment could pay off handsomely in the long run, provided the companies in question have excellent prospects. Block's long-term prospects are more important than its performance in the next year.

Stripping out these outlays (plus other line items, like employer payroll tax on employee stock transactions and amortization of prepaid marketing) reveals Klaviyo actually became more disciplined with costs. Since then, it has stayed on as an important institutional shareholder. The company did not provide net income projections.

Adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) grew 8% in the fourth quarter 2024, and management projects another 5% growth in 2025. Despite its hefty yield and prospects for AI-powered growth, Energy Transfer only trades for around eight times last year's distributable cash flow.

With the prospect of higher tax revenue likely to eventually lure the remaining state legislatures to legalize sports gambling, DraftKings has plenty of room for further expansion within the United States. DraftKings is gaining access to new markets as more governments move to legalize betting on sports.

These incidents demanded swift crisis management and care, while Carnival's growth prospects were carefully safeguarded and key initiatives remain in place. Carnival recognizes the importance of incident management to ensure customer safety, rebuild trust, and deliver exceptional experiences, thereby generating value for shareholders.

As tantalizing as these growth prospects are, Dutch Bros' nearly positive free cash flow (FCF) is what makes the company so interesting to me right now. Trading at 21 times forward earnings , Chewy's budding profitability, devout customer base, and veterinary growth potential look reasonably priced for prospective investors.

Mature, profitable companies with long track records of paying shareholders, and also increasing the amount they pay yearly, can be a strong foundation for any retirement portfolio. Additionally, the average home in America is nearly 40 years old, so future needs for remodeling should help support Home Depot's long-term business prospects.

Read on to see the financial metrics, growth prospects, and potential risks of both companies. In other words, this stock looks ready to run for years, building shareholder value along the way. Toast is one of my favorite buy ideas in this bull market, and I don't even have a serious runner-up suggestion in the restaurant sector.

Depending on which view of the company you subscribe to, things could keep getting worse for shareholders over the next couple of years -- or they could get a lot better. Management's primary goal at the moment is to break even on its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) before the close of 2026.

Very few public companies offer monthly dividends, and the ones that do are typically real estate investment trusts (REITs) because they are legally required to pay out 90% of their taxable earnings to shareholders. Prospects look promising for LTC Properties because America's aging population should keep demand for its services high.

Third, it needs to do those two things without sabotaging its future prospects for growth. At the same time, since Q1 of 2022 it paid out nearly $700 million in dividends to its shareholders, so it will need to pay at least that much over the coming four quarters to keep investors satisfied.

This has helped Amazon's shares soar over time, scoring a win for long-term shareholders. In the most recent quarter, Etsy announced four-year compound annual growth rates in the double digits for revenue, gross merchandise sales (GMS), and adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ).

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content