This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Efficient capacity management and strategic financial initiatives aimed at debt reduction have been key factors in its success. billion in debt, the company expects to achieve annual interest savings of $145 million, contributing to a debt reduction of $500 million. Total debt at the quarter's end was $27.0

Even with the company currently in the trough of its business cycle, Omega Flex currently holds a return on invested capital (ROIC) of 24%. Measuring the company's profitability compared to its debt and equity, this resilient ROIC is indicative of a wide moat surrounding Omega Flex's operations.

We are also excited to have several portfolio companies in the advanced stages of completing strategic acquisitions, which if successful, will provide the opportunity for additional future fair value appreciation in addition to providing us highly attractive incremental debtinvestments in these high-performing portfolio companies.

Best-in-class profitability and incredible returns However, this leadership position means nothing if it doesn't lead to profits and free cash flow (FCF). With a return on invested capital (ROIC) of 28% and an expected $1 billion in FCF in 2023, Bombardier is also a leader on the profitability side of things.

million, producing a core EBITDA margin of 11% and a trailing 12-month return on invested capital of 8.4%. As can be seen on Slide 19, for the first fiscal quarter of 2025, our net debt to adjusted EBITDA ratio now sits at just 0.6 While net debt to capitalization is only 6%.

3D printing is targeted at the enormous tail of the curve, meaning complex, low-volume, high-mix part types where injection molding tooling often presents a prohibitive return on investment for the OEMs. The largest use of cash during the year was $87 million used to repurchase $111 million of debt in March.

And this quarter, we reached a key financial milestone by returning to a fully unsecured capital structure. billion of debt, lowering rates by 300 basis points. This transaction allowed us to address a 2025 debt maturity, while also effectively buying back 5.1 You're at double-digit return on invested capital.

43 million loyalty members strong While growth may slow in the upcoming year as consumers wrestle with rising interest rates and credit card debt levels at all-time highs, Ulta's customer loyalty should help it ride through this potential downturn. Ulta's market-beating qualities Ulta Beauty boasts a return on invested capital (ROIC) of 61%.

This resulted in higher realized iron ore premiums, but more importantly, higher margins and returns on invested capital. They should rather be treated as a type of debt amortization. As you can see on the next slide, our expanded net debt remained stable at $16.5 billion in the quarter. billion in the quarter.

We owe an immeasurable debt of gratitude to Bernie. Interest and other expense for the third quarter increased by $157 million to $595 million due primarily to higher debt balances than a year ago. I'd like to thank them for their dedication and hard work. He was a master merchant and a retail visionary. in the third quarter of 2023.

A mere $10 invested weekly would balloon to just over $1 million by the time she turns 55, assuming 10% returns. Should we dare to dream of beating the market by 2 percentage points via outperforming stocks like the one included in today's article, this $1 million would spike to $2.4 Image source: Getty Images.

Free cash flow as a percentage of revenue has declined from 2023 due to higher cash interest expense from debt related to the VMware acquisition and higher cash taxes due to a higher mix of U.S. billion of cash and 74 billion of gross debt. So, that's the return on investment that attracts and keeps us going at this game.

Snap-on's best-in-class profitability With a return on invested capital (ROIC) of 17%, Snap-on has a long history of delivering high profitability in comparison to its debt and equity. Image source: Getty Images. Snap-on seems to fit this mold with an ROIC ranking in the top quartile among its S&P 500 peers.

billion in debt and returned $1.6 Interest expense of $206 million in the quarter was up $82 million versus last year primarily reflecting the issuance of $7 billion in debt to fund the NFP acquisition. billion of debt in 2024 and coupled with earnings growth, lowered our debt-to-EBITDA leverage from 4.1

And I'd like to acknowledge the work of our finance team for developing methods to track the retail industry standard metric gross margin return on investment, commonly known as GMROI, down to the category level for our own internal use. We expect these workstreams and their related expenses to be completed in the fourth quarter.

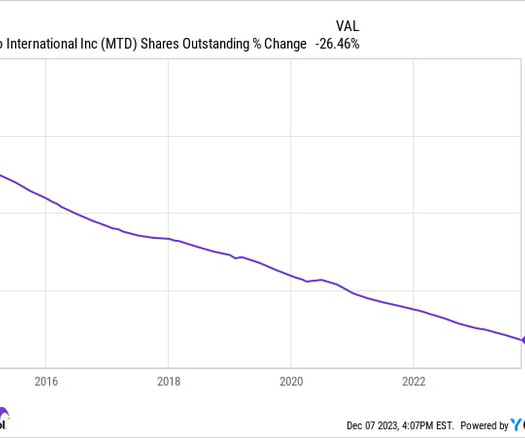

Best-in-class profitability and cash returns to shareholders With a return on invested capital (ROIC) of 44% -- the 10th best in the S&P 500 index -- Mettler-Toledo's immense profitability indicates a wide moat that allows the company to maintain strong pricing power.

Historically, stocks that sell for less than $50 a share tend not to be an ideal pond to fish in for dividend growth investments. However, the three businesses in this article are the exception to this hypothesis. Consider Kroger (NYSE: KR) and Rollins (NYSE: ROL). Executing five 2-for-1 stock splits and eight 1.5-for-1

However, the four businesses mentioned in this article operate in niche industries poised to deliver steady growth over the long haul. Calling stocks "no-brainers" is generally something not to be taken lightly.

The second thing that this gets rid of is the debt. When we get to this return number, why are we getting debt out of this thing? Asit Sharma: Let's now extend net tangible assets by one letter, unlevered net tangible assets and that is getting rid of the debt. That's your return piece. of long term debt.

Recycling capital in this way keeps our portfolio competitive, lower its capital expenses, and accelerates our return on invested capital, driving long-term core FFO growth. Atlanta ranks as a B performer with an improving outlook mainly due to the progress we've made in reducing bad debt and fraudulent activity.

In line with our stated financial strategy after funding our dividend, Core continued to dedicate free cash to paying down debt. During the quarter, Core's net debt was reduced by $15.8 This reduction in our outstanding debt also decreased our leverage ratio to 1.66, down from 1.76 million, net debt was $132.3 or lower.

In line with our stated financial strategy, after funding our dividend, Core continued to dedicate free cash to paying down debt. During the third quarter, Core's net debt was reduced by nearly $12 million or 9%. This reduction in our outstanding debt also decreased our leverage ratio to 1.47, down from 1.66 last quarter.

While merely investing $8 a week in the S&P 500 Index may not sound like enough to set you on a path to retirement, this $400 added annually could balloon to nearly $200,000 after 40 years, assuming the market's standard 10% returns. This slightly higher rate would turn these weekly $8 additions into $344,000 over the same time.

Today, we consider ourselves to be in a strong financial position, having recently reduced our net debt position and right-sized the balance sheet through our ongoing strategic shift toward an asset-lighter business model. Debt less cash on hand as of January 31st, 2024, was $51.6 Long-term debt as of January 31, 2024 was $51.4

We have made tremendous progress toward those goals and now expect to achieve record EBITDA per APCD and record return on invested capital this year. billion of debt during the quarter, including $392 million of our 11.5% billion of debt related to new ship deliveries that are contributing minimal to no EBITDA in 2023.

All of these actions have positioned our company to be in a stronger financial position, with our balance sheet rightsized and our net debt position at the lowest level since becoming a publicly traded company. Debt less cash on hand as of October 31, 2023 was $37.4 Long-term debt as of October 31, 2023 was $40.6

We continue to repay debt, and we reinstated a quarterly dividend, signifying strong execution on our three-year plan and creating value for our owners. Our strategy is underpinned by a commitment to financial performance, with a focus on free cash flow, return on invested capital, and earnings durability.

compounded annually, which will allow us to use our cash flow generation to pay down debt and rebuild the balance sheet as we work toward investment-grade leverage metrics. During the quarter, we used excess liquidity to opportunistically prepay over $1 billion of debt while still retaining $7.3 billion off the peak.

As a result, the new integration will position both of our companies to expand market share, streamline benefits, and drive higher return on investment for joint clients. These are -- you know, we have no bad debt with any of these accounts, not even on the fringe of having to explore such a scenario. They scale faster.

billion in cash, cash equivalents, and marketable securities and no debt. And we are working to better connect and streamline the organization to improve operational discipline and efficiency while retooling certain go-to-market functions to focus on areas with the strongest return on investment. As of October 31, we had $1.6

At the same time, we continue to aggressively manage down debt and interest expense while reducing the complexity of our capital structure, which David will elaborate on. The number of actions we've taken to improve our balance sheet this quarter puts us further down the path on our return to investment-grade credit ratings over time.

And following the Fitch upgrade in July, our balance sheet now has two investment-grade ratings and our dividend yield is in line with the S&P 500. Strong cash generation has supported debt repayment of $2.4 I think you even have a news article saying flights could be up high-single-digit levels.

Last month, we completed a very successful $16 billion debt exchange offer and consent solicitation. As I stated in my prepared remarks, we're planning to stay within that area of investment not only in FY '26 but for the immediate years beyond. We're making progress on all. And these aircraft acquisitions are within that framework.

We are working to pivot our business toward a model that will streamline our operations and sell nonstrategic assets, improve the consistency of our earnings, increase EBITDA and dividends per share, reduce debt, rightsize the balance sheet, and improve the return on invested capital. Long-term debt as of July 31, 2023 was $40.7

At the midpoint of our guidance this year, we anticipate savings of over $40 million of SG&A, including bad debt relative to 2023. For 2018 and at the midpoint of our 2024 outlook, we expect to reduce cash SG&A, excluding bad debt as a percentage of revenue by roughly 210 basis points in Europe, Africa, and LatAm in aggregate.

That's the ratio of net unsecured debt to adjusted EBITDA. Our focus is to continue to pay down debt between now and the closing of the Frontier deal. As we work toward that target, we continue to focus on generating strong cash flows and paying down debt. times, and that target is unchanged. We have talked about it.

We will remain financially disciplined and evaluate each node in the network based on the return on investment and the timing of the impact to the P&L. We ended the quarter with $51 million of cash and no revolver debt. We have no long-term debt. Now, I'll hand it over to Ryan for a financial update. million, up 1.2%

They allow us to reprioritize where we invest while also reducing the net drag on the business and improving our return on invested capital. These decisions, although difficult at the time, are the right decisions for our business. Now, let me cover the highlights for the quarter as depicted on Slide 4. billion and $3.5

We believe that Azure Solutions will allow us to continue to enhance our existing creative solutions, prioritizing ad creatives with predicted higher return on investment. In addition, we recently expanded our collaboration with Microsoft Azure, integrating Azure OpenAI solution to a range of ongoing services.

And then we see the revenue, operating income and free cash flow benefit for years to come after that, with strong returns on invested capital. The other thing that we're doing with cash flow right now is we're repaying some of the debt that we had taken on during that negative free cash flow period.

So, you mentioned in the prepared remarks that with your current debt levels, you have more flexibility for M&A going forward. And you called out having refinanced some debt at a higher rate. Kofi, is there any opportunity with like some of the shorter term, whether it's commercial paper or just shorter term debt?

Higher interest expense incurred from debt issued at our IPO offset stronger underlying financial results. Higher interest expense incurred from debt issued at our IPO lowered results in 2023. Our cash position and strong performance during 2023 has resulted in a net debt to adjusted EBITDA ratio of 1.4 You know, our No.

We used some of that free cash flow to pay down debt, bringing our net leverage ratio to 3.55 As I mentioned earlier, we have a robust and multifaceted investment plan in place for the second half of the year, reflecting our confidence in consumer responsiveness to our brand building efforts. times in the second quarter.

With strong cash generation, we continue to progress our balance sheet back toward investment-grade metrics and announced a 50% increase to our quarterly dividend. We delivered a return on invested capital of 13%, 5 points above our cost of capital and in the top half of the S&P 500. billion, and after reinvesting 2.3

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content