This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Is a dividend cut around the corner, or can this highly diversified assetmanager maintain its eye-popping yield for everyday investors who buy at recent prices? Here's a look at how the REIT is managing its quarterly dividend commitment. The Sculptor portfolio continues to reduce reliance on mortgage servicing. per share.

This process can often be delayed at the collateral underwriter review stage where workloads are already substantial. Our AI tools are driving these gains from automating income verification and collateral review to enabling multiple client chats and insights that boost conversion. You mentioned the $70 billion.

On the institutional side, our continued leadership in pension risk transfer was reinforced through a second transaction with IBM, this time to reinsure $6 billion of pension liabilities. We maintain a AA rating, which reflects a healthy capital position, including more than $4 billion in highly liquid assets at the end of the third quarter.

professional liability and general liability portfolios where we took underwriting actions to improve profitability. The one-point increase was due to higher attritional loss ratios on our professional liability and general liability insurance product lines as we remain prudent in adding margin to classes with challenging loss trends.

After that deadline has passed, Oaktree has the right to take control of Inter by claiming the collateral pledged in the 2021 financing deal – Suning’s majority stake in the club. If Oaktree does take control of Inter, it will be following in the footsteps of Elliott Management.

Although the prize of this purchase was General Re's reinsurance operations, General Re also owned a specialty investment company -- New England AssetManagement (NEAM). The WSJ report suggests legacy operators like AT&T and Verizon could face hefty clean-up costs and health-related liabilities because of their lead-clad cables.

Professional Liability and General Liability portfolios. General Liability and Professional Liability product lines within our Insurance segment. Favorable development in the first quarter this year was most notable within our International Professional Liability and Marine and Energy product lines.

Today with Pyro, we get a crystal clear understanding of advances within hours of reviewing the deal tape, which allows us to price the deal quickly and accurately while the seller doesn't need to worry about a tail of liabilities. We look at all these portfolios. We run them. The Motley Fool has no position in any of the stocks mentioned.

Pension plans and insurers have been piling into funds that invest in equity tranches of collateralized loan obligations in recent months, according to several assetmanagers who spoke on the condition of anonymity. GoldenTree AssetManagement, Sculptor Capital Management, Carlyle Group Inc.

PGIM, our global assetmanagement business, is well positioned to address the increasing demand for retirement solutions around the world while capitalizing on growing institutional demand for private credit and alternative investments. and international businesses in retirement, assetmanagement, and insurance.

And within these coupons, only a small fraction of our pools are backed by generic collateral and approximately 70% have what we would characterize as high-quality prepayment protection and the benefits of our collateral selection were best seen in the latest prepayment report. Please go ahead. Trevor Cranston -- Analyst Hey, thanks.

We continue to monitor and manage the office exposure in the portfolio. We did move one loan into NPL status and have the collateral of that loan and the collateral of the NPL from last quarter, both being marketed for sale. And I'm also curious if assetmanagement acquisitions are likely in the cards for you all.

Our servicing and assetmanagement business contributed meaningfully to the strength in adjusted EBITDA, thanks to dramatically lower runoff in the portfolio and our conservative credit culture, which has led to strong credit fundamentals within the portfolio. The decrease in non-cash MSR revenues drove a $7.2 Those are two examples.

As we look ahead, we are well positioned as a global leader at the intersection of assetmanagement and insurance. Our insurance and retirement businesses, in turn, provide a source of growth for PGIM through affiliated net flows, as well as unique access to insurance liabilities. Moving to Slide 5.

Prismic will enhance our mutually reinforcing business system and drive future growth by leveraging our differentiated brands, global asset and liability origination capabilities, and multichannel distribution. We have cash and collateral balances that earn short-term yields. Turning to Slide 5. Results of our U.S. Sure, Ryan.

Michele Reber -- Senior Director, AssetManagement Thank you, and good morning. I mean it's a fully collateralized loan. Operator [Operator signoff] Duration: 0 minutes Call participants: Michele Reber -- Senior Director, AssetManagement Taylor C. I would now like to turn the conference over to Michele Reber.

Morgan AssetManagement China, both of which closed within the last year. For the quarter, record net long-term inflows were 61 billion, positive across all channels, regions, and asset classes, led by fixed income and equities. So, we had a reward liability adjustment this quarter, kind of a technical thing.

billion of total liquidity transactions this year, including the recently announced sale of 75% of our interest in five Utah hospitals to a new joint venture with a leading multibillion-dollar assetmanager. Did you pledge any of your real estate as collateral in conjunction with the Steward ABL or bridge loan refinancing?

Michele Reber -- Senior Director, AssetManagement Thank you and good morning. And it's collateralized as well by the equity interest in that private investment. So it's well collateralized, high net worth individual with great track record. [Operator instructions] As a reminder, this conference is being recorded.

In addition to Home Point, we closed the acquisition of Roosevelt Management, which provides us the professional team in the RA infrastructure for our assetmanagement strategy. Finally, I'd like to update you on our deferred tax asset, which declined by 158 million this quarter and now totals 499 million.

NII ex-markets was up $274 million or 1%, driven by the impact of balance sheet mix and securities reinvestment, higher revolving balances in card, and higher wholesale deposit balances, predominantly offset by lower deposit balances in banking and wealth management and deposit margin compression. NIR ex-markets was up $1.8 Expenses of $22.6

This past May, MicroStrategy submitted our response letter to the FASB on the proposed change, so we noted there was an overwhelming response from interested parties, which included support from sophisticated institutional assetmanagers, large accounting and audit firms, crypto exchanges, and banks.

Also, we have an information advantage consisting with decade's worth of data on collateral performance on the part of literally thousands of sellers. Currently, we're in discussions with several institutional investors, as well as pension plans, sovereign wealth funds, assetmanagers, and family offices.

We're in active discussions with potential new clients, and we're also building out our assetmanagement capability in preparation for launching an MSR fund later this year. billion, 517 million was in cash, with the remainder consisting of available liquidity on our MSR lines, which is fully collateralized and immediately available.

billion in liquid assets to pay pension benefits, fund investment opportunities, satisfy potential collateral demands related to our use of derivatives, and to fund expenses. It's part of their asset-liability approach where they allocate massively to bonds when rates are higher and much lower when rates are very low.

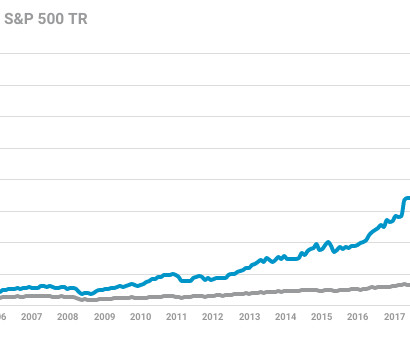

So if you start with the S&P 500 or in this case stocks and bonds, you only have two asset classes, right. And the question was if you can find other areas of investment that can generate the types of returns you need for your liability stream, diversification becomes the free lunch. RITHOLTZ: Fair enough. Less, 20, 30%?

You've got a point there because they are the world's largest alternative assetmanager live, they have hundreds of billion dollars to sling around to make acquisitions, to finance big deals, etc. You have on one hand, private equity group, masters of collateral, masters of financing. Asit Sharma: Maybe. I think actually, yeah.

We believe our clients view us as the gold standard in alternative assetmanagement. Our original strategic plan, which was to start in corporate advisory and then quickly move into private equity, followed by a succession of other assetmanagement businesses over time. And we have no insurance liabilities.

billion in liquid assets to pay pension benefits, fund investment opportunities, satisfy potential collateral demands related to our use of derivatives, and to fund expenses. Given our known liabilities, this is a strategy that works for us, I can't comment on others want to do.

Less than 20 per cent of the fund’s credit portfolio is being managed by third parties, according to Edgell, though the firm maintains strong relationships with some of the world’s largest alternative assetmanagers. But, he said he doesn’t see any systemic risks in the asset class. KKR & Co. Things have changed.

Not its assetmanagement, its brokerage piece. And the Japanese regulators were having a tough time with cross collateralization and issues about whether there were balance sheet accounting issues. You sort of have a one foot in the um, financial planning, assetmanagement side and another side in actual fund management.

Brian Higgins has put together a amazing track record handling distressed and stressed debts, as well as other forms of credit real estate collateralized obligations. In 2017, you launched a collateralized loan obligation business. They might have had some spill that they had a big liability from, or the governance was bad.

I mean, I have to say the first thing, and maybe I wasn’t very good at it early in my career, but you start to think about particularly on the assetmanagement side. It’s roughly two-thirds, three-quarters of the liabilities in the world. It’s the collateral.

from the underwriting actions and changes in our professional liability reinsurance structure and higher operating expense ratio in our international operations to support investment and growth initiatives. Our exited collateral protection insurance product line, or CPI, added 2.3 points last year. Moving to our reinsurance segment.

.; chairman, president, and chief executive officer of the company; Steven Hamner, executive vice president, and chief financial officer; Kevin Hanna, senior vice president, controller, and chief accounting officer; Rosa Hooper, senior vice president of operations and secretary; and Jason Frey, managing director, assetmanagement and underwriting.

By leveraging our best-in-class servicing platform, they can focus on what they do best and whether that's assetmanagement, retail originations or banking, they're growing faster than the industry overall, which is driving our joint growth. billion in assets from Flagstar, which principally consisted of mortgage servicing rights.

The servicing and assetmanagement revenues that these two businesses generate are wonderful sources of revenue and earnings in up cycles and also paramount in down cycles. Our SAM segment continues to deliver healthy recurring cash flows from our scaled servicing and assetmanagement activities.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content