This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Buyout firms have long relied on controversial loans backed by equity stakes to enhance fund returns, but growing investor criticism has triggered a slowdown, according to a report by Bloomberg UK. This shift partly reflects a rebalancing of power, enabling LPs in private equity funds, such as pensionfunds to exert influence over GPs.

And such REITs often employ leverage, usually using their loan portfolio as collateral, to enhance returns. In some ways, a mortgage REIT is more like a mutual fund than a company. The answer is institutional investors focused on asset allocation. That list might include pensionfunds, endowments, and insurance companies.

Annaly buys mortgages that are pooled into bond-like securities, often called something like a collateralized mortgage obligation (CMO). Annaly is really designed to be owned by total return investors who focus on asset allocation (such as insurance companies and pensionfunds). Image source: Getty Images.

It buys pools of mortgages that have been brought together into bond-like securities, often called something along the lines of collateralized mortgage obligations (CMOs). In fact, Annaly is most appropriate for institutional-level investors with a focus on asset allocation , as it provides exposure to the mortgage debt market.

Pension plans and insurers have been piling into funds that invest in equity tranches of collateralized loan obligations in recent months, according to several asset managers who spoke on the condition of anonymity. billion in assets, said the attraction of low default rates for leveraged loans, estimated at 1.5%-2%

Rather, it buys mortgages that have been pooled into bond-like securities, sometimes called collateralized mortgage obligations or something similar. Mortgage REITs usually use leverage in an effort to enhance returns, with the mortgage securities they own acting as collateral.

trillion of assets under management supporting defined benefit and defined contribution plans, PGIM serves more than half of the world's 300 largest pensionfunds. We maintain a AA rating, which reflects a healthy capital position, including more than $4 billion in highly liquid assets at the end of the third quarter.

Investors in the Fund, which were a mix of numerous new investors as well as existing New Mountain Net Lease investors, include pensionfunds, insurance companies, asset managers, endowments, family offices and high net worth individuals. Since inception, New Mountain’s net lease strategy has completed $1.9

A mortgage REIT like AGNC buys mortgages that have been pooled into bond-like securities, often referred to as something like a collateralized mortgage obligation (CMO). Generally, leverage is employed so that more CMOs can be bought, with the CMO portfolio acting as collateral for the loan.

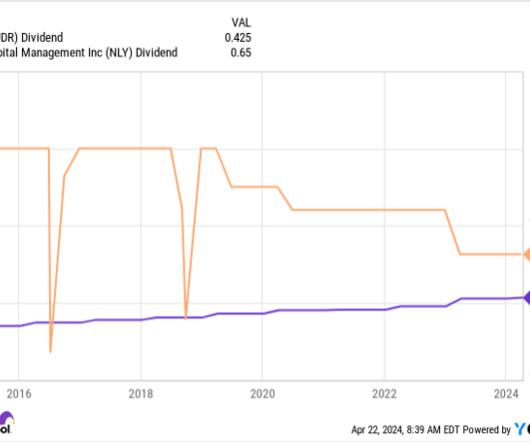

UDR Dividend data by YCharts To be fair, Annaly isn't a bad REIT -- it's just meant for large institutional investors, like pensionfunds, that focus on total return (which assumes dividend reinvestment) and asset allocation. That's very different from what most small dividend investors are looking for.

The answer is investors who follow a fairly complex asset allocation model (which should obviously include mortgages as an asset class). In fact, the most common asset allocators are large investors like pensionfunds, family offices, and endowments. That's not likely to be a small income investor.

It owns mortgages that have been pooled together into bond-like securities, which are usually called something like a collateralized debt obligation (CDO). However, it is how institutional investors using an asset allocation model would think about dividends and investing in general. Thus, their prices can be fairly volatile.

Annaly is a mortgage REIT, which means it buys mortgages that have been pooled into what are often called collateralized mortgage obligations (CMOs), or something similar. It is very different from a property owning REIT, which buys physical assets and rents them out. dividend yield, which can cause an unfortunate emotional reaction.

Blackstone (NYSE: BX) recently reached a huge milestone when it surpassed over $1 trillion in assets under management ( AUM ) in the second quarter. It became the first global alternative asset manager to hit that level and will add another notch to its belt when it joins the S&P 500 index later this month.

Technically, mortgage REITs like Annaly usually buy bond-like securities that represent a pooled collection of mortgages, often called something like a collateralized mortgage obligation (CMO). The portfolio of mortgages is often used as collateral for that leverage, which can be a problem if CMO values fall dramatically.

Layan Odeh of Bloomberg reports CPPIB plows at least $5 billion into private equity in three months: Canada Pension Plan Investment Board poured at least $5 billion into private equity in the last three months of 2024 as the asset class regained appeal. Canadas largest pension notched a 3.8% billion 10-year net return of 9.2%

OHA sourced this transaction through its strategic direct lending partnership with BMO Capital Markets (“BMO”), which includes over $1bn to invest in jointly originated senior secured private credit assets.

A higher cost of debt and slower economic growth have created a tough investing environment, pushing down the value of some private assets that pensionfunds own. Private credit has been one of the best-performing asset classes for some large pensionfunds in recent years, often earning double-digit percentage gains.

PGIM, our global asset management business, is well positioned to address the increasing demand for retirement solutions around the world while capitalizing on growing institutional demand for private credit and alternative investments. pension plans, and is the largest pensionfund manager in Japan.

Artemis reports the Healthcare of Ontario Pension Plan (HOOPP) grew ILS investments 35% in 2022: Large Canadian institutional retirement fund, the Healthcare of Ontario Pension Plan (HOOPP), grew its allocation to insurance-linked securities (ILS) investments in 2022, with the asset class nearing 1% of its overall portfolio by the end of the year.

We’re seeing a slow-grinding implosion of this titanic asset bubble that started in 2012,” says Dan Zwirn, CEO at Arena Investors. estimates private-market assets were $13.1 Apex Group, a provider of services to asset managers, has just refinanced a slug of debt with a $1.1 McKinsey and Co. trillion at the end of June 2023.

They’re talking about asset management firms, in which public pensionfunds often have investments, supporting shareholder proposals meant to achieve social justice or climate objectives yet of dubious financial value. Both are financially deleterious. Nor is it supported by the empirical evidence.

Freschia Gonzales of Wealth Professional reports HOOPP achieves 9.38% return in 2023: The Healthcare of Ontario Pension Plan (HOOPP) announced a return of 9.38 percent for the year 2023, increasing its net assets to $112.6bn from $103.7bn at the end of 2022. in assets for every dollar owed in pensions. billion ($84.9

So if you start with the S&P 500 or in this case stocks and bonds, you only have two asset classes, right. So the proper benchmark for those pools has to look a little bit like the underlying assets they’re investing in. If you look at the types of assets that Yale invests in, you can create a benchmark for each pool.

We surpassed $1 trillion of assets under management. We believe our clients view us as the gold standard in alternative asset management. In fact, virtually all of our drawdown funds we've launched in our history, have been profitable for our investors. Thank you all for joining the call.

James Bradshaw of the Globe and Mail reports OMERS reports steady gains at mid-year mark in shift to bonds, credit: Ontario Municipal Employees Retirement System relied on steady returns from private assets, tailwinds from strong stock markets and a resilient U.S. dollar assets, which boosted its overall investment return by 1.7

Paula Sambo of Bloomberg reports Canada pensionfund's credit head wants to take advantage of leveraged buyout boom: Canada’s largest pensionfund plans to nearly double the size of its credit holdings over the next five years, and it’s counting on an upturn in leveraged buyouts to generate some of that growth.

So they’d give individual asset allocation to people and they’d go invest their money. So we’d have credit, we’d have equities, we’d have hedge fund strategies, but with no silos. So it, it really has and, and pensionfunds, they’re on hold today. How has this affected your business?

For example, the federal government recently announced it would stop issuing real return bonds – an important liability matching asset for many defined benefit pensions in Canada. Many Canadian pension must now consider non-Canadian alternatives, such as US TIPS. Investors need be prepared for and accept this added risk.

And now we, you know, we’re just shy of $145 billion of assets on the management across the entire credit curve. Not its asset management, its brokerage piece. And the Japanese regulators were having a tough time with cross collateralization and issues about whether there were balance sheet accounting issues. billion in assets.

KKR was the biggest with $400 million of assets and eight people. And Forstmann Little was the second biggest with $200 million of assets, and four professionals and they hired me in as the fifth professional. Do you do distressed asset, real estate? It’s the big Canadian asset plans. And by ‘90s, two guys had left.

The Fund’s quarterly results were driven by positive performance in credit and private equities and gains across U.S. dollar-denominated assets, which benefited from a strengthening U.S. The $1 billion decrease in net assets consisted of $1 billion in net income, less $2 billion in net base CPP outflows.

And this is just a masterclass in how to manage assets, think about your career, understand the relationship between markets, between fixed income, the Fed, the dollar, sentiment, consumer spending, just everything is related and understanding what matters when is the key to your success. He helps to oversee $2.5 RIEDER: It is.

In addition to BMW and Volkswagen AG , Northvolt’s top investors included Goldman Sachs’s asset management arm, Denmark’s biggest pensionfund ATP, Baillie Gifford & Co. funds and a number of Swedish entities. Northvolt will also have access to about US$145 million in cash collateral.

We were talking about luck earlier, got introduced to a local asset manager outside of Boston who saw what I was working on and said, this is really interesting. And so as those assets grew, I’m now a young 20-year-old going out trying to go to other asset managers saying, Hey, I have this quantitative research.

MORGENSON: It can be collateralized loan obligations, now it’s big private debt. I think that the asset stripping that has also occurred, pensions, for instance, are sold off, overfunded pensions get sold off and that goes into the private equity firm instead of into the company itself. Kind of a thing.

So, if you remember, we were, we were still rolling out various facilities like the, the, the term asset backed, the lending facility, for example. We were running the commercial paper funding facility. 00:20:24 They have, I don’t know, three, $4 trillion of custody assets from foreign. I’m sorry.

David Milstead of the Globe and Mail reports HOOPP, with half of assets in Canada, has no plan to retreat despite trade chaos: The Healthcare of Ontario Pension Plan has invested more than half of its assets in Canadian holdings and that is not about to change despite the threatening economic climate, its leaders say.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content