This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bill Mann: It's funny because stock buybacks are thought to be a very efficient way to return cash to existing shareholders in the form of there's not much in the way of tax, and every share of stock you should think of as being a perpetual claim on earnings and assets of a company. Why are they so curious about this, Bill? Bill Mann: Yes.

yield after managementfees and actual capex and generated a 10.6% in the aggregate, including property taxes, which represented approximately 36% of our total operating expenses and are projected to increase approximately 3% in 2024. And then maybe on the real estate tax guide. The community was sold at an approximate 5.5%

At the end of September, the fair value of our equity portfolio included cumulative pre-tax unrealized gains of $7.8 Net unrealized investment gains included in other comprehensive income in the first nine months of 2024 were $283 million net of taxes, compared to net unrealized investment losses of $135 million net of taxes last year.

This quarter's higher RWA is largely due to seasonal effects, including higher client activity in Markets and higher risk weights on deferred tax assets, partially offset by lower Card loans. Asset & Wealth Management reported net income of $1 billion with pre-tax margin of 28%. above the effective tax rate.

The expansion of our affordable housing capabilities with the acquisition of tax credit syndicator Alliant Capital in 2021 is an enormous addressable market with fantastic growth drivers that will fuel additional growth in our core debt and sales businesses. 1 issue on their minds is affordable housing and housing affordability.

See the 10 stocks *Stock Advisor returns as of April 30, 2024 As a quick review of the bidding, at the Markel Group, we are working to build one of the world's great companies. At the end of March, the fair value of our equity portfolio included cumulative pre-tax unrealized gains of $7 billion.

This morning, we reported full year 2023 earnings of $2 billion, reflecting record pre-tax pre-provision income of $3.2 You know, if they -- if we can hit the bid that we have to make sure we get an appropriate risk-adjusted return, we'll do that. We appreciate you joining our call today. However, the pace of remixing has slowed.

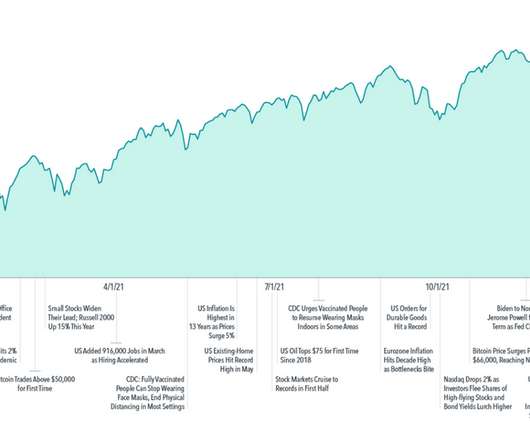

Another market curiosity arose in early 2021, when individual investors and others helped bid up shares of videogame retailer GameStop, as Exhibit 3 shows. Commissions, trailing commissions, managementfees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing.

The Global Pension Transparency Benchmark is a world first global standard for pension disclosure, bringing a focus to transparency in a bid to improve pension outcomes for members. Costs matter, and they should be understood, managed, and disclosed.

Managementfees increased by $165 million, due to an increase in average assets managed by external fund managers. Other categories affecting our total cost profile include taxes and expenses associated with various forms of leverage. Our operating expense ratio was 28.6 bps and up marginally from 27.1

trillion of assets under management. Our 15th consecutive quarter of managementfee and FRE growth and a record fundraising quarter for the firm. Some additional highlights for the year include managementfees up 30% and 91% of these managementfees are from permanent capital vehicles.

All of these factors enabled us to end the year with after-tax adjusted operating income of $1.6 billion and after-tax adjusted operating earnings per share of $8.44, which represents growth of 10.2% The strong earnings power for GAAP was also apparent in our statutory results with full-year after-tax operating earnings of over $1.3

Horner is asked another question from the critics who believe Harper will just do the Smith government’s bidding. “I Horner cited low investment returns and rising operating costs, managementfees, and staffing when announcing the firings on Nov. 30 this year.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content