This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

News of a premium-priced buyout strapped a rocket to the share price of IT consultancy Perficient (NASDAQ: PRFT) on Monday. The enterprisevalue of the transaction is roughly $3 billion. Three billion-dollar price tag Perficient is being acquired by a unit of Sweden-based investment firm EQT.

Meanwhile, IBM is buying HashiCorp for $35 per share, an all-cash deal with an enterprisevalue of $6.4 IBM expects HashiCorp's services to unlock synergies with its hybrid cloud computing platforms, built around the $34 billion Red Hat buyout in 2019. Buy the news?

Both Morrisons and MFG are controlled by the private equity firm Clayton Dubilier & Rice (CD&R), and sources said the talks were focused on a transaction with an enterprisevalue of up to £2.5bn.

Alpine plans to invest the capital for Fund IX in control buyouts of software and services businesses with total enterprisevalues of up to $1 billion and focus on add-on acquisitions for high-performing platform investments. Europe, Asia, and the Middle East.

That is, there are service providers that offer state-of-the-art platforms and support, an ever-growing number of consultants to serve as guides at start-up and longer-term, and a growing pool of capital resources available to advisors seeking working capital, liquidity, or to offset unvested deferred comp that may be left behind.

And large teams with many advisors are often continuously fulfilling a sunset buyout for a retiring team member—creating a continuous cycle that can be difficult to break. Plus, don’t forget the happiness quotient, a non-economic source of value that we shouldn’t ignore.

With deep-rooted backgrounds in private equity, encompassing roles as investors and trusted advisors, we have actively contributed to transactions exceeding $2 billion in enterprisevalue.” ” Visit Meritage Partners’ Profile “Founded in 2009, Solganick & Co.

As a family office, we are interested in long-term investment partnerships of all sort (minority, majority, and buyout), and our permanent capital allows us to to build and hold our platform investments for generations, rather than the typical short time horizons constraining most private equity funds.

Theres no universally agreed-upon definition of the middle market, but typically it includes companies with annual revenues in the low hundreds of millions and enterprisevalues that dont quite reach the stratosphere. What Exactly Is the Middle Market? Their referrals often lead to the highest quality deals.

It’s not just power generation from those sources, but it’s companies that are involved in consulting, in utility services, in companies that make components that are helping electrify the economy, in electric vehicles or in HVAC systems. BARATTA: — that are $10 billion to $15 billion-plus enterprisevalue company.

And the equity checks being written by these private equity firms are larger than they’ve ever been as well, greater than 50% usually of the enterprisevalue of the transaction that they’re, they’re taking on that, [ Ritholtz 00:14:56 That, that’s big. And they’re being bought out by private equity firms.

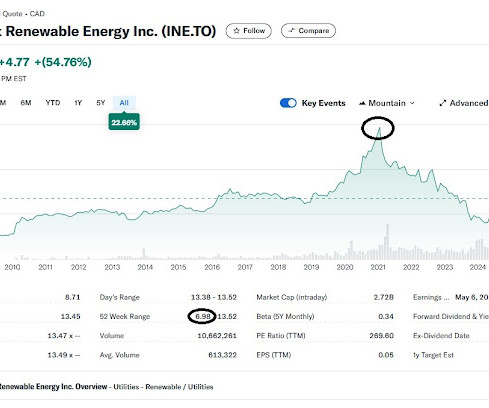

Total enterprisevalue of the agreement, which includes debt on the Innergex balance sheet, is $10-billion. The buyout is expected to close in the fourth quarter. on the TSX as of February 24, 2025 The Transaction represents a total enterprisevalue of $10.0 CDPQ is already the second-largest holder.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content