This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

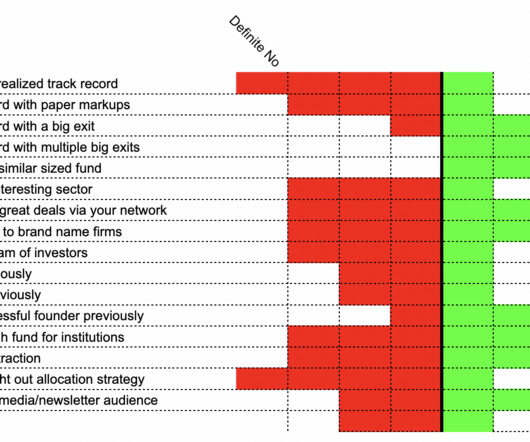

Normally, I can tell whether or not a VC will be able to raise capital for their fund at the particular size they’re trying for—and if not that size, what the market might bear at this stage. Yes, as track record is a combination of dealflow and deal selection. Are there proxies for track record?

The structural underinvestment in critical minerals over the past decade has resulted in severely discounted valuations for excellent assets and created a massive need for capital investment, as countries transition to more sustainable energy sources,” said Brandon. Source: businesswire Can’t stop reading? (BX)

in consultative discussions, demonstrating the added clinical utility to be gained by adding the Nanox.ARC to their practices. Inaudible] Altogether, in terms of the locations and the place, by far, our pipeline and dealflow is far bigger than what we have indicated, and we continue to work. we have put the U.S.

In the middle market, where every deal counts, you need to be both methodical and a bit opportunistic. Building a Healthy DealFlowDealflow is a term youll hear in almost every PE conversation. Their referrals often lead to the highest quality deals.

At the same time, we're swiftly capitalizing on two distinct opportunities. I am confident these actions are foundational for producing consistent comparable store sales growth and improved working capital efficiency. This action will enable us to consistently offer fresher, balanced assortments of good, better, and best products.

And as long observed in markets, information about capital has become almost as important as capital itself. Nonoperating results for the quarter included $108 million of net investment gains, driven primarily by gains linked to a minority investment and unhedged seed capital investments. Earnings per share of $11.46

I have known Ramesh for a number of years, and he is familiar with our business through previous consulting work. We continue to experience healthy dealflow, which helped offset the margin impact of our system integration, which we estimate was approximately 130 basis points in the quarter. Gross profit increased 6.3%

Last year resulted in a record-breaking year for deal volume on Axial, with 10,735 deals coming to market in 2024 a 7.8% The increase happened largely in the second half of the year, with both Q3 and Q4 resulting in 26% and 15% higher dealflow than the same periods in 2023, respectively. CA 8 Solganick & Co.

Technology ranked 4th in dealflow but had the highest average pursuit rate, 8.76%, of all sectors. See below for the full Q3 deal activity overview on the Axial platform, and for a more detailed breakdown by industry, check out The SMB M&A Pipeline: Q3 2023. We do ground-breaking, confidential global client marketing.

It reflects the continuing success of our proactive efforts to enhance working capital and thoughtfully manage our costs. We are committed to building on this progress and achieving positive free cash flow in the second half of our next fiscal year. These dynamics can impact visibility into the timing or size of potential deals.

Our balance sheet is strong across the board, an intentional result of our high-quality assets, robust capital and liquidity positions, and rigorous risk management. billion in capital to our common shareholders, and that includes $500 million through share buyback. During the first quarter, we returned $1.5 First, we generated $3.1

Dealflow is very strong, and we believe that we are still the best partner in the industry. For fiscal 2025, we will have increased capital expenditures due to a higher number of organic new store openings and supply chain investments, and as a result, higher depreciation and amortization. And Eric, welcome back.

My comments today will seek to provide insights into our quarterly business performance, insights into our capital allocation priorities, early insights into integration and synergy tracking as well as views on overall guidance for the remainder of the year. million, and free cash flow was $83.4 million or 40.7% million or 41.9%

This translates to billions in excess capital, meaning that unlike many U.S. This approach not only enhances long-term risk-adjusted returns, but also allows for diversification and access to dealflow that is not otherwise available through indexing to public markets. per cent, respectively.

Transactions Highlights Ontario Teachers’ manages approximately 80% of assets internally, with a focus on deploying capital into active strategies. Helped portfolio company APCO Holdings LLC acquire National Auto Care , a leading provider of finance and insurance products, administration, consulting services, training, and marketing support.

We also continue to bring on additional new resources to increase our in-house capabilities and further decrease our reliance on third-party consultants. Please see our Terms and Conditions for additional details, including our Obligatory Capitalized Disclaimers of Liability. The Motley Fool has a disclosure policy.

It will be the 105th deal out of Brooklyn Bridge Ventures, the firm I started back in September 2012, and it will be the last deal I’ll be making out of my third fund. It will also be my last venture capitaldeal. For me, I don’t mind sharing how I think about it.

We also stated our belief that an easing of the cost of capital would be very positive for Blackstone's asset values and would be a catalyst for transaction activity, including deployment and ultimately, realizations, which in turn fuel fundraising. Turning to the recovery in commercial real estate.

Our team's efforts continue to produce unique and proprietary dealflow, and we continue to identify attractive investment opportunities across all three external growth platforms. However, I think it is prudent due to the lack of current visibility into fourth quarter acquisition activity and the rapid change in our cost of capital.

When I started leading deals at First Round Capital, I sourced investments in 8 companies. Singleplatform was a referral from an IT consultant who was trying to sell me stuff—which was pretty much the most random source ever, and Backupify was actually my own idea built by someone far more capable than I was to see it through.

There's $466 million in operating cash flow for the quarter, very capital-light. They bring most all of that down to the free cash flow. We saw that as underwriting activity picked up and they had higher dealflow, they had a higher conversion rate of around 19%. But getting to the numbers, revenue was up 12%, $2.5

And it’s, you have to focus on financing the litigation cases with a high probability of a successful outcome, but where the plaintiff doesn’t have the capital to see it through and are up against the deep pocketed defendant who could just wait him out. Was how helpful was Peter Thiel’s capital?

The transcript from this week’s, MiB: Armen Panossian, Oaktree Capital Management , is below. Armand Posiion is head of performing credit at Oaktree Capital Management, where he works with the likes of, of Bruce Kosh and Howard Marks. We returned a lot of capital. Another extra, extra special guest. The sector was perfect.

trillion units of trusts, BlackRock's platform is becoming the premier long-term capital partner across public and private markets. We're connecting investors, corporates, and the public sector to the power of the capital markets. At more than 10.6 trillion in assets under management, 10.6 Operating income of 1.9

Private equity deal activity in Asia-Pacific is showing signs of recovery, with transaction volumes rising 11% year-on-year to $176bn in 2024, according to a report by Bloomberg citing global consultancy Bain & Co. Dealflow is expected to gain further momentum, as financial sponsors adapt to shifting market conditions.

Companies will either have the growth and performance to attract new capital or will need to find a home with a larger company. Increased dealflow and M&A activity should create more opportunities at all levels, opening up executive and leadership roles as companies hope to shift back into growth mode.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content