This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Main Street Capital (NYSE: MAIN) Q3 2024 Earnings Call Nov 08, 2024 , 10:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Greetings, and welcome to the Main Street Capital third-quarter earnings conference call. Image source: The Motley Fool. You may begin.

Main Street Capital (NYSE: MAIN) Q4 2024 Earnings Call Feb 28, 2025 , 10:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Greetings and welcome to the Main Street Capital fourth quarter earnings conference call. Image source: The Motley Fool. You may begin. for the quarter.

Decrease in net sales was driven by a 12% decrease in the volume of megawatts sold and the aforementioned increase in our Series 7 product warranty liability, partly offset by expected payments associated with contract terminations in the U.S., This decrease was primarily driven by capital expenditures associated with our new U.S.

This is a function of investors being concerned following a July report from The Wall Street Journal that alleged legacy telecom companies utilizing lead-sheathed cables could face large environmental/health liabilities, as well as replacement costs. Furthermore, any potential liabilities would likely be determined by the U.S.

Here are eight ways the wealthiest Americans reduce their tax liability -- or even avoid paying taxes altogether. No taxes on unrealized capital gains The No. This is known as unrealized capital gains and can be a great tool to defer taxes on winning investments in your brokerage account.

FCEVs can be charged more quickly than BEVs and have a much longer driving range, but they require more capital-intensive hydrogen charging stations to be built. million in total liabilities. Nikola is trying to differentiate itself from those competitors by selling more hydrogen-powered FCEVs. million for the full year. It had $256.3

Since our last report, we have also begun implementation work on both our new enterprisewide POS solution and our new human capital and payroll management system. per share negative impact, primarily from unfavorable general liability insurance claims. We have also launched new mobile apps for both Family Dollar and Dollar Tree.

And with ROIC ending 2024 at 11%, comfortably above our cost of capital, we are already delivering long-term value for our shareholders as we lay the foundation we'll build upon in 2025 and beyond. million guest visits in 2024, we believe we have a meaningful opportunity to expand and capitalize on this strategic advantage.

Regarding capital allocation during the third quarter, we repurchased approximately 1.5 I think having price stabilization, not a bunch of big price swings from an appreciation or depreciation, more specifically depreciation. You can remember there was some big depreciation. I think that's a tailwind.

Throughout this process, we have been strengthening the balance sheet and prudently allocating capital to prioritize returns. As you will recall, based on the joint venture agreement we have with Total, our capital spending exposure for the project will be very manageable. Lastly, we continue to deliver on our capital return framework.

The other expenses that were a greater percentage of net sales in the fourth quarter were retail labor, incentive compensation, repairs and maintenance, depreciation and amortization, and technology-related expenses, partially offset by a decrease in professional fees. In 2024, total capital expenditures were $1.3 billion to $1.4

Main Street Capital (NYSE: MAIN) Q1 2024 Earnings Call May 10, 2024 , 10:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Greetings, and welcome to the Main Street Capital first-quarter earnings conference call. Should you invest $1,000 in Main Street Capital right now?

Main Street Capital (NYSE: MAIN) Q2 2023 Earnings Call Aug 04, 2023 , 10:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Greetings, and welcome to the Main Street Capital Corporation second-quarter earnings conference call. and Main Street Capital wasn't one of them!

billion RMB, primarily due to the loss from the revaluation of overseas RMB-related assets caused by the depreciation of RMB against the U.S. But a side note here is that NIO Capital has invested in a lot of AI companies, especially industry-leading AI companies. Interest and investment loss was 0.2 billion in 2023 Q4 and 0.3

Main Street Capital (NYSE: MAIN) Q2 2024 Earnings Call Aug 09, 2024 , 10:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Greetings and welcome to the Main Street Capital second quarter earnings conference call. Should you invest $1,000 in Main Street Capital right now?

Last but not least, we also continued to consistently deliver against our capital allocation priorities. For the full year, given continued favorability from lower average borrowings and adjustments related to capitalized interest, we now expect our fiscal '25 interest expense to be $410 million. We maintained a 2.9 billion to $3.1

Adjusted SG&A expenses increased primarily due to higher depreciation and temporary labor for the 3.0 Capital expenditures were $426 million versus $541 million last year. I just wanted to ask on, it didn't come up this quarter, but there's been the general liability claims a couple of times in the past. Operator Thank you.

Depreciation expense was $183 million in Q4 and was $743 million for the full year. As compared to last year, depreciation expense declined $4 million and $6 million, respectively, driven by reduced technology capital spend. Capital expenditures for the quarter were $99 million and $466 million for the year.

AT&T has a market capitalization of around $120 billion, and the company expects to generate between $17 billion and $18 billion of free cash flow this year. in 2024, a number that will be reduced by an increase in depreciation and a few other items. AT&T expects to report adjusted earnings per share between $2.15

There is no structural change in our free cash flow generation, and this variance is driven primarily by certain nonrecurring working capital benefits that we previously communicated were in the prior trailing 12-month period as well as the timing of significant capital expenditure payments. That's my first question.

In addition, it also enables us to acquire bitcoin through the use of excess cash or proceeds from equity capital raises or corporate debt capital raises. These capital market levers allow us to deploy intelligent leverage to increase our Bitcoin holdings in a manner which we believe has created shareholder value.

This is just a start as our goal is to get to 75 days, freeing up cash for our capital deployment priorities, which include returning cash to shareholders. Roofing granules add another year of mid-single-digit growth as we continue to capitalize on the multiyear roof replacement cycle. Last year, we returned $3.8

billion, up 14%, with the increase driven primarily by content acquisition costs, followed by depreciation, as well as the impact of the Canadian Digital Services Tax, which was applied retroactively. And how are we thinking about the return on invested capital with this AI capex cycle? billion, up 11%. Other cost of revenues was $22.1

of EPS that wasn't in our June outlook, was related to general liability claims. Predicting these claims is complex and we again increased our accrual for general liability this quarter after observing higher-than-expected costs to resolve certain claims. was attributable to the general liability adjustment, while the remaining $0.08

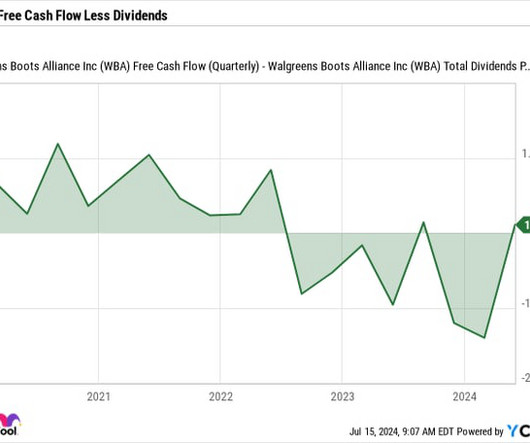

The company also only recently achieved profitability in the segment, reporting an adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) profit of $23 million for the period ending May 31. Walgreens recently said that it would be "simplifying and focusing the U.S. Its total current assets of $16.3

times its adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) over the past few years. It also has by far the highest market capitalization of these three REITs, at $57.3 However, management has been able to manage this debt, as shown by its coverage ratio , which has slightly dropped from 6.0

Depreciation was $67 million for the quarter compared to $61 million last year primarily due to new store and supply chain investments. Moving to the balance sheet and our capital allocation priorities. In the third quarter, we returned $267 million of capital to our shareholders through the repurchase of 731,000 shares.

While we continue to maintain strong credit ratings, a solid balance sheet, and long-term earnings growth outlook of 4% to 6%, our earnings guidance for 2024 reflects a combination of lag related to our capital investments and inflationary pressures that we are experiencing simultaneously. I'll describe these two factors in more detail.

In 2024, we've been focused on executing on our capital investment plan, regulatory dockets, and growth opportunities with great success. million for increased depreciation. The order also included a 50-50 capital structure, a return on equity of 9.4%, and a cost of capital of approximately 7.1%. billion in total.

On the liabilities side, current liabilities decreased by 56 billion NT, mainly due to the decrease in accounts payable. dollar terms, our fourth quarter capital expenditures totaled 5.24 Such a plan will enable higher capital efficiency in the mid to long term, but requires cost and effort in the near term.

During the quarter, we completed a comprehensive benchmarking study to identify opportunities to improve our operating margin, working capital, and asset efficiency. Next, to strategically deploy capital to unlock growth and white space opportunities. Our capital expenditures were 4.3 Q1 net loss was 7.9 million, or minus $0.24

External title data shows that our market share initially accelerated relative to our performance across the second half of 2022, but then came under pressure during multiple periods of steep depreciation. Regarding capital structure, during the quarter we repurchased approximately 686,000 shares for a total spend of $49 million.

As discussed on the year-end call in February, results in 2024 reflect a combination of regulatory lag related to our capital investments and inflationary pressures. First-quarter 2024 results include higher pension, depreciation, and interest expense compared to the same period in 2023. Utility margin increased $0.5

billion, up 9%, with the increase primarily driven by content acquisition costs, primarily for YouTube, followed by depreciation due to increasing investments in our technical infrastructure. In 2024, we saw 28% year-over-year growth in depreciation as we put more technical infrastructure assets into service.

million for increased depreciation. The settlement also included a 50-50 capital structure and ROE of 9.4% and a cost of capital of approximately 7.1%. Utility depreciation and general taxes increased $2.5 Utility depreciation and general taxes increased $4.5 Utility margin increased $0.4 Other income declined $4.2

For us, SG&A means selling, general, and administrative expenses including payroll and other compensation, marketing and advertising expense, depreciation and amortization expense, and other selling and administrative expenses. And we are working to ensure we are properly positioned to capitalize on this opportunity. Thanks, Chuck.

With our new operating model firmly in place, we are accelerating actions to improve profitability and capital efficiency by more than 10 billion in 2025, which I will discuss shortly. The operational and capital improvements we are driving will be especially important as we manage the business through the near term.

So now focusing specifically on Latin America, we had a number of countries that saw significant currency depreciation against the US$, notably Argentina, Mexico, and Brazil. Please see our Terms and Conditions for additional details, including our Obligatory Capitalized Disclaimers of Liability.

This figure excludes $149 million of depreciation. We spent $172 million on capital expenditures. Turning to capital allocation. billion tax liability. The offset to that is a deferred tax liability. Adjusted EBITDA was $8.2 billion or 63% of revenue. Revenue for our semiconductor solutions segment was $7.3

Our capital allocation strategy is consistent with our historical framework as we continue to take a disciplined approach to maximizing shareholder value. Capital expenditures were approximately $588 million in fiscal 2024, supporting our growing real estate pipeline. We also continued to return excess cash to shareholders.

Several hundred million dollars of gross fixed assets invested in our Bloomington fab have been largely depreciated. Total depreciation and amortization is expected to comprise about 5% of our revenues in the current quarter. At the same time, our depreciation declined to $5.1 Interest expense was $2.4

The fundamentals of our business were healthy in the quarter, with solid procedure growth and strong capital placements resulting in healthy financial performance. Turning to capital, we placed 341 da Vinci systems in the quarter, of which 320 were multiport systems, including 70 da Vinci 5 systems. Bariatric procedures in the U.S.

On the liability side, current liabilities increased by TWD 31 billion, while long-term interest-bearing debt decreased by TWD 38 billion. This change was primarily driven by the reclassification of TWD 42 billion in bonds payable from noncurrent to current liabilities. trillion or USD 69 billion. billion and USD 26.9

Altogether, these outside funding opportunities enable us to accelerate our revenue growth while minimizing internal capital requirements. These enable us to increase our capacity and capabilities without requiring us to use our own capital. We continue to improve upon our capital position in fiscal 2023.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content