This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As a result, most pay out very generous distributions, which are similar to dividends, but much of the payout is considered a return of capital. By and large, this structure has been eliminated, and MLPs are generally in better financial shape as a result, carrying less leverage and being able to grow their business through free cash flow.

Gryphon Investors has completed the sale of Kano Laboratories , a producer of branded oils and lubricants that it acquired in November 2020, to L Squared Capital Partners. In November 2023, L Squared held the final closing of its fourth fund with $840 million of capital. 2024 Private Equity Professional | December 20, 2024

Burlington Capital Partners (BCP) has sold Sokol Custom Food Ingredients to Solina , a France-based global provider of ingredient solutions for the food industry. Leveraging Sokols sweet sauce capabilities will round out and enhance our offerings, said Michael Marks , the president of Solina USA. Astorg invests in U.S.

The only caveat is this telecom giant is primarily using share repurchases in its capital-return program, something that's practically non-existent recently at Verizon and AT&T. T-Mobile's massive capital-return program could prove even better for shareholders than big cash dividends from its competition.

It generates a lot of cash through its wholly owned subsidiaries, and it invests a lot of that capital back into its investment portfolio and short-term treasuries. With an enterprisevalue of $1.01 If it trades at 20 times that figure, its enterprisevalue would roughly double to $2 trillion by the end of the decade.

Enterprise ended the quarter with leverage of 3x. It defines leverage as net debt adjusted for equity credit in junior subordinated notes (hybrids) divided by adjusted EBITDA. What this means for investors in simpler terms is that Enterprise's distribution payout is well covered by its cash flow. cents per unit.

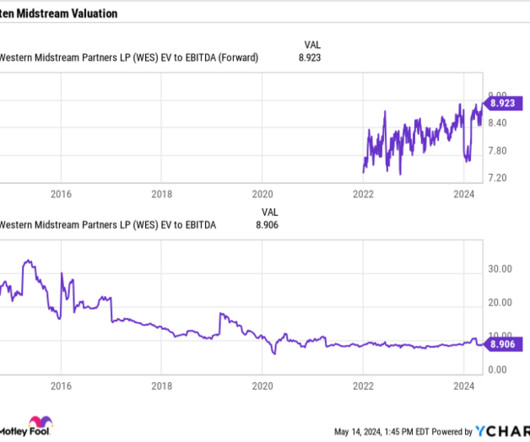

Meanwhile, its balance sheet is in good shape with a leverage ratio (net debt/adjusted EBITDA ) of just 3.2 It is planning to spend $950 million in growth capital expenditure (capex) this year. times (one of the most common ways to value midstream stocks) is attractive and well below the 13.7

Energy Transfer: A low value gives it a high yield Energy Transfer expects to generate $13.1 The master limited partnership (MLP) currently has an enterprisevalue (EV) of $95.2 billion to $13.5 billion of adjusted earnings before interest, taxes, depreciation, and amortization ( EBITDA ) this year. That puts its valuation at 7.2

That leverage gives Carnival a high debt-to-equity ratio of 4.6. Nevertheless, investors should still take into account Carnival's debt -- which is reflected in its higher enterprisevalue instead of its lower market capitalization -- when valuing its stock. It ended fiscal 2019 with $9.7 billion in 2025."

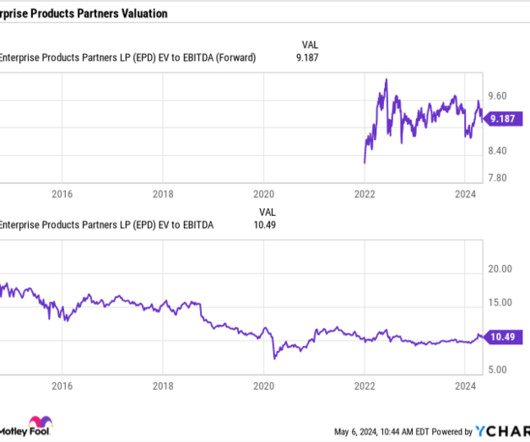

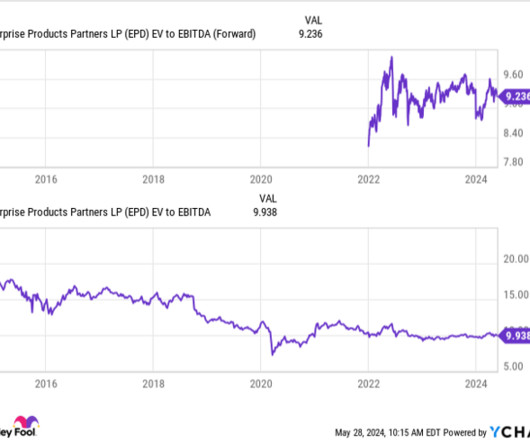

Dirt cheap any way you slice it Enterprise Products Partners has generated $9.1 With its enterprisevalue currently around $88.2 The MLP is also really cheap on a cash flow basis: Image source: Enterprise Products Partners. That should give it the fuel to increase value for investors over the long term.

times based on its non-consolidated distributable cash flow, which is cash flow before growth capital expenditures (capex) , and payout to partners. The company had to cut its distribution in half in the fall of 2020 after it had gotten over its skis with its debt and needed to reduce its leverage.

Gridiron Capital has expanded its team with the hiring of Marcus Meyer as managing director, capital markets. Gridiron created this new in-house capital markets function to improve and expand its financing capabilities and to expand its relationships with senior and mezzanine lenders. “We billion of capital.

Alpha GCC will be owned by the promoter group of Aster India and funds managed by Middle East private equity firm Fajr Capital Advisors. The transaction values the GCC business at an enterprisevalue of $1.7bn and an equity value of $1bn. Aster DM Healthcare to sell Gulf business to Alpha GCC for $1.01bn.

(Nasdaq: CNSL) (“Consolidated Communications” or the “Company”), a top 10 fiber provider in the United States, today announced that it has entered into a definitive agreement (the “Agreement”) to be acquired by affiliates of Searchlight Capital Partners, L.P. Source: Businesswire Can’t stop reading?

but its leverage could keep rising as it brings its new miners and plants online. With an enterprisevalue of $6.1 I'd personally prefer to directly buy Bitcoin on the open market than invest in Marathon's capital-intensive business, but this mining stock could still outperform BTC over the long run as it scales up its business.

It's leveraging its AI investments to grow two businesses at scale. Meanwhile, it's using the considerable cash flows it generates to buy back shares, boosting the value of future earnings to shareholders. Microsoft's forward P/E ratio sits around 31.5, as of this writing. As a result, it's seeing expanding profit margins.

The two biggest areas to look at when it comes to dividend safety are its distribution coverage ratio and leverage ratio. The former measures how much cash in distributions the company is paying out, compared to how much distributable cash flow (operating cash flow minus maintenance capital expenditures) it's generating. billion to $3.75

Rithm Capital (NYSE: RITM) Q1 2024 Earnings Call Apr 30, 2024 , 8:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Hello, and welcome to the Rithm Capital first quarter 2024 earnings conference call. Should you invest $1,000 in Rithm Capital right now? Today, we're at $7.1

Centerbridge is acquiring Precinmac from Pine Island Capital Partners , Bain Capital’s Private Credit Group , and Compass Partners Capital , who purchased the company from GenNx360 Capital Partners in April 2020. We are excited to begin our next chapter of growth with Centerbridge.

An elevated leverage ratio led the master limited partnership (MLP) to slash its distribution to retain more cash for debt reduction in 2020. However, as leverage improved, the company's priority shifted back to rebuilding its payout. With an enterprisevalue (EV) of $98.5 That also gives the company lots of visibility.

Rithm Capital (NYSE: RITM) Q2 2024 Earnings Call Jul 31, 2024 , 8:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Good morning and welcome to the Rithm Capital second-quarter 2024 earnings call. Should you invest $1,000 in Rithm Capital right now? Today we have $7.3

It plans to spend about $95 million in maintenance capital expenditures (capex) over the rest of the year, so its distributable cash flow (DCF) will be about $1.6 Without reducing debt any further, the company is on track to get to 3 times leverage (net debt/adjusted EBITDA) by year end. or more a quarter in enhanced distributions.

Driven Brands' strategy is fairly capital intensive. For perspective, its enterprisevalue is just $6.2 For years, PayPal's leadership has talked about leveraging its consumer data. It wants to find ways to grow its enterprise business, and Chriss' expertise in this area will help. billion, or only 11.5

billion on growth capital projects in 2024. Its earnings growth has also helped drive down its leverage ratio , which it expects will be toward the low end of its 4.0-4.5 That lower leverage recently gave two credit rating agencies the confidence to upgrade Energy Transfer's credit rating to BBB with a stable outlook.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

While similar, distributions include a return on capital that is untaxed until the units are typically sold, making them tax-deferred. The company's balance sheet is currently in good shape, with leverage (as used by rating agencies) toward the low end of its 4x to 4.5x The master limited partnership (MLP) currently pays out a $0.32

It recently announced it was buying PFSweb for $181 million, or an enterprisevalue of $142 million, which includes the company's cash balance of $39 million. -based company known for its prowess in reverse logistics (processing returns). Now, GXO has made another promising deal. The deal is expected to close in the fourth quarter.

billion enterprisevalue. The highly accretive nature of the deals further supports Oneok's capital allocation strategy. The company continues to expect it will return 75% to 85% of its free cash flow after capital expenses to shareholders over the next several years. leverage ratio after closing its deals with GIP.

The deal puts an enterprisevalue of $16.5 Novo Nordisk, for its part, will leverage Catalent's status as a key manufacturing subcontractor to expand its fill-finish capacity to better meet the high demand for its popular obesity drug, Wegovy. per share in cash -- a 16.5% billion on Catalent. "We

Its FCF was lower compared to a year ago as the company increased its capital expenditures (capex) on new growth projects. Enterprise slowed down its growth projects during the pandemic but last year started to ramp them up once again. It ended the quarter with leverage of 3 times. It generated distributable cash flow of $1.8

Energy Transfer's leverage ratio is now in the lower half of its 4.0 Plenty of fuel to continue growing value Despite its surging unit price, Energy Transfer still trades at a bottom-of-the-barrel valuation compared to its midstream sector rivals. billion on growth capital projects this year. times target range. billion and $2.6

OceanSound Partners has acquired PAR Excellence Systems from Northlane Capital Partners. The Bethesda, Maryland-based firm was formed through the January 2017 spinout of American Capital Equity III LP from American Capital as a result of the acquisition of the company by Ares Capital.

Leveraging Thoma Bravo’s deep sector expertise and strategic and operational capabilities, the firm collaborates with its portfolio companies to implement operating best practices and drive growth initiatives. The firm has offices in Chicago , London , Miami , New York and San Francisco.

The $14 billion deal values the utilities at 1.3x enterprisevalue -to-rate base and 16.5 billion) annually in low-risk, fast-payback capital projects over the next three years. The company is leveraging its strong balance sheet to fund the deals, which it expects will close by the end of next year. It's paying $9.4

Alternative credit manager Kennedy Lewis Investment Management (Kennedy Lewis) has closed its third opportunistic credit fund, Kennedy Lewis Capital Partners Master Fund III LP and its associated parallel and co-investment vehicles, with $4.1in capital commitments.

Qualcomm also generates most of its profits from its higher-margin licensing business, which leverages its massive portfolio of wireless patents to squeeze royalties and licensing fees from every smartphone sold worldwide (including those that don't use Qualcomm's SoCs). It has an enterprisevalue of nearly $190 billion with 1.1

Lincoln International has reported that the Lincoln Private Market Index (LPMI), which tracks the enterprisevalue of U.S. contraction in enterprisevalue due to investor uncertainty surrounding interest rates and potential tariffs. However, those from 2021 saw leverage increase by 0.3x, while 2022 deals experienced a 0.6x

times average enterprisevalue (EV) -to- EBITDA multiple between 2011 and 2016, while today most midstream stocks trade at under a 10 times multiple. EV/EBITDA tends to be the most used metric to value midstream companies, as it takes into consideration their debt positions and takes out non-cash expenses. Trading at just 7.4

billion to $3 billion into growth capital projects in 2024. Meanwhile, its leverage ratio is trending toward the low end of its 4.0 On top of that, it has visible organic cash flow growth coming from its current slate of capital projects, which will provide a lift through 2026. Energy Transfer expects to invest $2.8

Its distributable cash flow (DCF), which is similar to free cash flow except that it only subtracts maintenance capital expenditures (capex) and not growth capex, was essentially flat at $1.1 Kinder Morgan ended the quarter with a leverage ratio (net debt divided by trailing-12-month adjusted EBITDA) of 4.1.

DCF is similar to free cash flow except that instead of subtracting out total capital expenditures (capex) , it only reduces the number by maintenance capex. The company ended the quarter with a leverage ratio (net debt divided by trailing-12-month adjusted EBITDA) of 4.1. It expects to end the year with leverage ratio of 3.9.

The Lincoln Private Market Index (LPMI), which tracks changes in the enterprisevalue of privately held companies in the United States, increased by 1.9% Compared to the public markets, the S&P 500’s quarter-over-quarter enterprisevalue increase of 4.5% outpaced the LPMI. in the second half of 2023 to 11.1x

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content