This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

billion through 2026 on new RNG facilities, Waste Management aims to generate an additional $450 million in free cash flow (FCF) annually once its capital expenditures (capex) start paying off. WM Return on InvestedCapital data by YCharts Measuring the company's profitability to its debt and equity, Waste Management's 10.5%

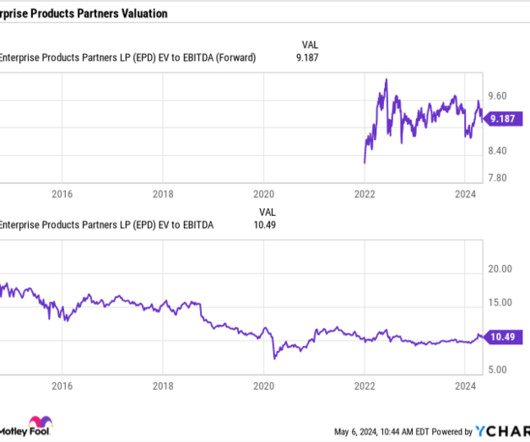

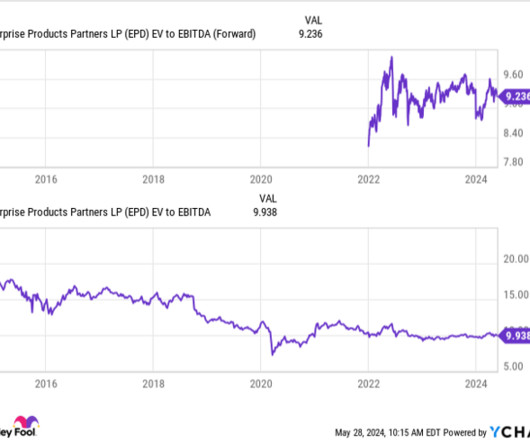

Last year, Enterprise picked up its growth capital expenditures to $3.5 Enterprise has averaged about a 13% return on investedcapital over the past five years. That part of the Enterprise story remains, but now investors should see more growth starting to come out of the company over the next several years.

The former measures how much cash in distributions the company is paying out, compared to how much distributable cash flow (operating cash flow minus maintenance capital expenditures) it's generating. On that front, Enterprise had a robust 1.7x Enterprise also has a solid backlog of growth opportunities, with $6.8 billion to $3.75

Over the last decade, MTY has averaged a return on investedcapital (ROIC) of 15%, generating high levels of FCF compared to the debt and equity it uses to fund its M&A ambitions. Compared to its weighted average cost of capital (WACC) of 7%, the company consistently creates value for investors.

That rapid growth was driven by the increased adoption of online payroll services and its rollout of additional human capital management (HCM) services for managing employees, expenses, and digital documents. At its peak, its enterprisevalue hit $31.9 Its adjusted EBITDA margin expanded from 39% in 2020 to 42% in 2022.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

Enterprise's business model has seen the company consistently grow its distributable cash flow (DCF) per unit (operating cash flow minus maintenance capital expenditures [ capex ]) most years, while keeping it pretty steady during difficult environments, such as when oil prices collapsed during 2014-2016. Image source: Getty Images.

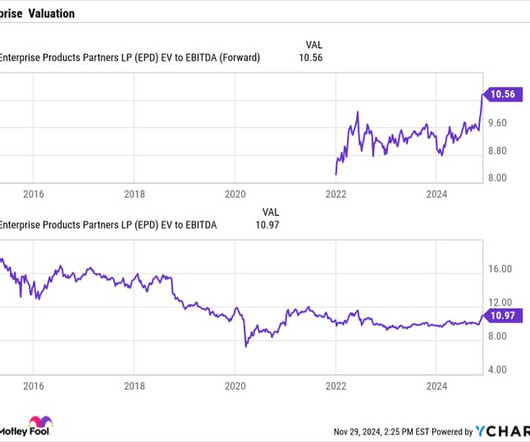

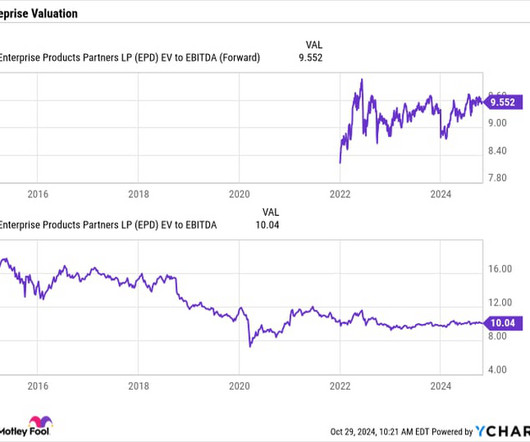

Meanwhile, it has historically been conservative with its leverage, distribution coverage ratio, and growth capital expenditure (capex) spending. Since 2018, Enterprise has averaged an approximately 13% return on investedcapital (ROIC) on its growth projects. It currently has $6.9

Cava stock trades like that of a software company at almost 10 times its enterprisevalue to sales, so it isn't cheap. return on investedcapital , which underlines how efficiently Chipotle deploys capital to create value. There could eventually be thousands of Cava stores.

DCF is similar to free cash flow, except that operating cash flow is only reduced by maintenance capital expenditures ( capex ) and not growth capex. Based on its DCF, Enterprise's distribution coverage ratio was 1.7x. Enterprise currently has $6.9 It produced distributable cash flow (DCF) of $1.96 billion, a 5% increase.

Its FCF was lower compared to a year ago as the company increased its capital expenditures (capex) on new growth projects. Enterprise slowed down its growth projects during the pandemic but last year started to ramp them up once again. At a similar return, the approximately $10.5 It generated distributable cash flow of $1.8

Furthermore, its enterprise-value-to-free-cash-flow (EV/FCF) ratio is well below its average over the same time, highlighting the market's uncertainty around the company. Cash ROIC measures a company's FCF generation compared to its debt and equity, meaning that higher figures show outsized returns on capital deployed.

The fourth quarter comes in ahead of plan Earlier this year, Carnival CEO Josh Weinstein unveiled a new three-year plan called SEA Change, which stands for Sustainability, EBITDA per available lower berth day (ALBD), and Adjusted return on investedcapital (ROIC). times that forward EPS guidance. EV/EBIT ratio.

Most of that decline occurred in early November amid concerns that the company was cannibalizing its user base with its newer Beti platform, which provides a better return on investment (ROI) for its clients but generates lower revenues per customer. Based on those estimates and its enterprisevalue of $2.5

Operating profit, so the margin percentage, how much money you make off of each sales dollar drives value. Incremental investment; the rate of investment, how much do you need to invest in fixed assets and working capital to drive that next dollar of sales or next dollar of profits? We'll get into this.

We continue to invest thoughtfully and in a highly capital-efficient model to extend our network leadership, and it shows. That, combined with our capital efficiency has led to a record adjusted free cash flow quarter that grew 54% year over year and once again led the major wireless companies in free cash flow margin.

That is the cash that is left over after the company has paid all of its bill, made all of its capitalinvestments, made all of its investments and working capital. But then, so whether that's price or whether it's enterprisevalue, we can, there's applications for each. They end up with 5%.

Total market capitalization has increased from 3 billion to 90 billion. They've been, by and large, very good investments across, you know, not just the big ones, but the smaller ones as well. You know, obviously, there's a number of them that are synergistic to us, but you know, we have a strict adherence to creating value.

It's a lot like return on investedcapital. You're talking about a company which has developed everything in house for a long period of time, and suddenly is able to capitalize on that. But I'll say this. There actually is no single definition for ROIC. Total assets of 66 billion, goodwill of only 4.4 You name it.

compounded annually, which will allow us to use our cash flow generation to pay down debt and rebuild the balance sheet as we work toward investment-grade leverage metrics. Essentially, we've pull forward our most important sustainability goal and expect a step change in both profitability and return on investedcapital in just three years.

And following the Fitch upgrade in July, our balance sheet now has two investment-grade ratings and our dividend yield is in line with the S&P 500. We are focused on finishing the year strong, delivering industry-leading performance with a return-to-earnings growth and margin expansion, positioning us well as we head into 2025.

Trades around 55 times free cash flow, 31 times enterprisevalue to forward EBITDA so the value of its debt and equity compared to its forward earnings. What it might be going on here is a bit of investment. When you invest in your capital base and make it bigger, that lowers your return on investedcapital.

Palo Alto's shares currently trade for an enterprise-value -to-revenue ratio of 14.6. With a market capitalization of $124 billion, as of this writing, that would put its value at about $142 billion at the end of 2025. The consumer segment slowdown points to the biggest risk of investing in Micron: cyclicality.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content