This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Capital One (NYSE: COF) is one bank that faced pressure as multidecade-high interest rates weighed on the sector as a whole, but its stock has performed much better recently. Here's what you need to know about the acquisition and Capital One's business before buying it today. billion last year. Image source: Getty Images.

Like many other electric vehicle start-ups, Nikola went public by merging with a special purpose acquisition company ( SPAC ) and set some overly ambitious long-term goals. In its pre-merger presentation in 2020, it claimed it could ship 600 battery-powered electric trucks (BEVs) in 2021, ship 1,200 BEVs in 2022, and ship 3,500 BEVs in 2023.

Nikola (NASDAQ: NKLA) initially impressed the bulls when it went public by merging with a special purpose acquisition company (SPAC) on June 3, 2020. Instead, it was being valued based entirely on the ambitious production targets it set during its pre-merger presentation in March 2020. just six trading sessions later.

Steve Bakke -- Vice President, Capital Markets and Investor Relations Thank you all for joining us today for Realty Income's fourth-quarter operating results conference call. billion merger with Spirit Realty Capital in an all-stock transaction in October, which closed subsequent to year-end on January 23rd. at the midpoint.

The strong cash flow will enable us to return to a debt-free status as we exit Q1 2025, paying off the remainder of the $1 billion debt inherited from the NuVasive merger. The acquisition of Nevro further expands our reach into the musculoskeletal market, adding an additional $2 billion market space for us to compete in and grow.

Cvent”), an industry-leading meetings, events and hospitality technology provider, today announced the completion of its acquisition by an affiliate of private equity funds managed by Blackstone (“Blackstone”) for $8.50 We do this by using extraordinary people and flexible capital to help companies solve problems.

Rover” or the “Company”), the world’s largest online marketplace for pet care, today announced the completion of its acquisition by private equity funds affiliated with Blackstone (“Blackstone”) in an all-cash transaction valued at approximately $2.3 With the completion of the acquisition, Rover stockholders are entitled to receive $11.00

Blue Owl Capital (NYSE: OWL) Q2 2024 Earnings Call Aug 01, 2024 , 10:00 a.m. ET Contents: Prepared Remarks Questions and Answers Call Participants Prepared Remarks: Operator Good morning, and welcome to Blue Owl Capital second-quarter 2024 earnings call. Should you invest $1,000 in Blue Owl Capital right now?

Transaction Terms The merger agreement includes a customary 30-day “go-shop” period expiring on December 29, 2023. During this period, Rover and its advisors will be permitted to solicit, consider and negotiate alternative acquisition proposals from third parties. Closing of the transaction is not subject to a financing condition.

Capital One Financial (NYSE: COF) Q2 2024 Earnings Call Jul 23, 2024 , 5:00 p.m. Welcome to the Capital One Q2 2024 earnings call. Jeff Norris -- Senior Vice President, Global Finance Thanks very much, Josh, and welcome, everyone, to Capital One's second quarter 2024 earnings conference call. Image source: The Motley Fool.

Capital One Financial (NYSE: COF) Q1 2024 Earnings Call Apr 25, 2024 , 5:00 p.m. Welcome to the Capital One Q1 2024 earnings call. To access the call on the internet, please log on to Capital One's website at capitalone.com and follow the links from there. Should you invest $1,000 in Capital One Financial right now?

Capital One Financial (NYSE: COF) Q3 2024 Earnings Call Oct 24, 2024 , 5:00 p.m. Welcome to the Capital One Q3 2024 earnings call. We're webcasting live over the Internet as usual and to access the call on the Internet, please log on to Capital One's website at capitalone.com and follow the links from there. billion or $4.41

Led by our employees' commitment to operational excellence and capital discipline, we outperformed on oil, natural gas, and NGL volumes for the quarter, as well as beating expectations on per-unit cash operating costs. And it reflects our confidence in the increasing capital efficiency of our business going forward. We generated $1.6

When IonQ (NYSE: IONQ) went public by merging with a special purpose acquisition company (SPAC) in October 2021, it called itself the only "public pure-play" on the quantum computing market. Like many other SPAC-backed tech companies, IonQ burned out as it broadly missed its pre-merger forecasts. IonQ's stock started trading at $10.60

On September 18th, we announced that we had mutually agreed to terminate our pending acquisition by WillScot. In accordance with the terms of the merger agreement, McGrath received a termination fee of $180 million. McGrath is on a strong footing as we emerge from the terminated merger agreement. We are not. per diluted share.

And importantly, these things also allow it to do it all with the best capital efficiency in the industry. We also celebrated another major milestone in our Sprint merger integration as we are now substantially complete with both the billing migration and retail rationalization, well ahead of our year-end target. million and $29.2

Last week, we notified the Spirit that certain conditions to close may not be satisfied prior to the outside date set out in the merger agreement. We are evaluating our options under the merger agreement, which remains in effect. Next, continued costs and capital discipline are a top priority. Turning to the balance sheet.

See the 10 stocks » *Stock Advisor returns as of July 22, 2024 We are delighted to announce that we closed our merger with Cambridge Trust on July 12 and successfully converted all banking customers that we get. And we believe our best days are still ahead of us due to the strategic benefits of the Cambridge merger. 10 overall.

Barrick's continuing investment in its future and its ability to uncover and unlock the value opportunities embedded in its global asset portfolio has positioned us ideally both to capitalize on the current market fundamentals, as well as to continue to thrive throughout the future cycles, which are inevitable. billion for the quarter.

The company still has a huge amount of debt on its books, its history of acquisitions is littered with duds, and its sales and earnings growth will likely proceed at slow paces even in optimistic scenarios due to the competitive environments of the categories it operates in.

Blue Owl Capital (NYSE: OWL) Q4 2023 Earnings Call Feb 09, 2024 , 8:30 a.m. Actual results may differ materially from those in forward-looking statements as a result of a number of factors, including those described from time to time in Blue Owl Capital's filings with the Securities and Exchange Commission. per share for the year.

The first is to maintain a fortress balance sheet, which we believe will continue to be a competitive advantage over time and allow us to capitalize on opportunities as they become available. The second is our anticipated merger with Cambridge Trust, which demonstrates how we are capitalizing on opportunities.

Non-GAAP EPS was $0.72, increasing 36% versus prior year, even with the 32% increase in outstanding shares driven by the merger. The combination of these two businesses is one of the strengths of our merger, offering a broad range of product and market-changing innovation. Operations remains the strength of the merger.

Our forward-looking statements do not reflect the potential impact of significant transactions we may enter into such as mergers, acquisitions, dispositions, joint ventures, or any material agreements that we may enter into, amend, or terminate. million in total revenue and a stable capital structure. Turning to the bottom line.

September 1st marked the one-year anniversary of the Globus NuVasive merger, making this quarter the fourth consecutive combined earnings release with sales growth strong financial performance, and best-in-class innovative product launches. During our third quarter, we passed the one-year mark since the closing of the NuVasive merger.

Globus delivered another robust post-merger quarter in Q2 with sales of $630 million, growing 116% or $338 million. Non-GAAP EPS was $0.75, increasing 20% versus prior year even with the 35% increase in outstanding shares driven by the merger. Scavilla -- President, Chief Executive Officer, and Director Thanks, Brian.

Private equity’s role in M&A in 2024 In 2023, the financial services (FS) industry experienced a decline in mergers and acquisitions (M&A) for the second consecutive year. Within the three main FS subsectors—capital markets, banking, and insurance—expectations for 2024 M&A activity vary.

Roughly $7 million worth of cancels came from a single client event, a historic merger of two major global banks in Europe that affected us across index, ESG, and analytics. Just last week, we closed our acquisition of the London-based index provider, Foxberry. Turning to our other recent acquisitions.

Gwen’s practice ranges from in-court restructurings to bespoke, out-of-court liability management solutions. With a broad regulatory and transactional background, he also guides investment advisers in mergers and acquisitions. He has a versatile skillset and deep experience with platform acquisitions and sales.

Since we announced the merger agreement with WillScot Mobile Mini on January 29 and while the transaction is still pending, we continue to operate with a business-as-usual mindset. As always, and now during the pending merger, our focus will remain on the execution of our strategic plans and delivering positive financial results.

NII is essentially the difference between what banks make on interest-earning assets, such as loans, and pay out on interest-bearing liabilities, such as deposits. At a recent industry conference, JPMorgan Chase's chief operating officer, Daniel Pinto, said he thought consensus estimates for net interest income (NII) in 2025 were too high.

This is a transformative merger that positions us as one of the largest open internet advertising platforms. The news of our merger with Teads allows us to take a massively forward in executing this strategy. The reception we've seen from many industry players reinforces our confidence in the merger's rationale.

In addition, we completed three portable storage tuck-in acquisitions, opening some new markets and increasing density in others. On January 29th, we announced the merger with WillScot Mobile Mini for $3.8 Additional information about the merger will be set forth in the joint proxy statement that we will file together with WillScot.

On the call today, I will discuss our key strategic accomplishments in the core areas of the portfolio review third quarter highlights and results and outline our preliminary capital production and cost outlook for 2025. In the US, since 2020, we have executed more than $5 billion of acquisitions and over $2.5

I'm going to talk about the highlights of the third quarter, then we're going to do some -- a little bit of strategic updates and we're going to end up with Tony talking about the results and capital allocation. We have the plan, Frontier acquisition. And the third is our capital allocation priorities. It's just adding capacity.

Yesterday, we announced the second-quarter 2024 earnings and affirmed our full-year 2024 financial guidance, with record Rocky Mountain region volumes, continued progress on acquisition-related synergies and solid demand on our products and services drove our strong second-quarter performance and provide momentum into the second half of 2024.

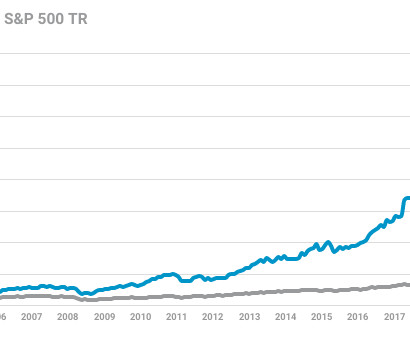

See the 10 stocks *Stock Advisor returns as of March 21, 2024 The acquisition of Valens in January of 2023 was a key tactical move for SNDL, enhancing our upstream capabilities in Canadian cannabis. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*. We achieved a positive free cash flow of 1.4

As we announced on July 17th, our board, after consultation with its financial advisor and outside legal counsel, unanimously determined that the July 13th revised unsolicited proposal by 3D Systems Corporation would reasonably be expected to result in a superior proposal as defined in Stratasys merger agreement with Desktop Metal.

Our results for the start of 2024 illustrate our focus on thoughtful, disciplined growth and continue to demonstrate the consistency of our global operating and acquisition platform. This quarter's bias toward international volume is a testament to the diversity of geographies we consider to allocate capital. Welcome, everyone.

Before Kirsten tells you more about our financial performance for the quarter, let me provide a brief update on our pending acquisition of VMware. the Hart-Scott-Rodino pre-merger waiting periods have expired, and there is no legal impediment to closing under U.S. merger regulations. merger regulations. In the U.S.,

The fourth quarter capped a productive year of continued transformation to make Prudential a higher growth, more capital-efficient, and more nimble company. Over the course of 2023, we executed several attractive transactions adding to our capital efficiency. Turning to Slide 3. Turning to Slide 5.

We continue working toward a successful closing of our pending merger transaction with Magellan while remaining focused on the growth of our legacy assets. Strong producer activity and a constructive volume outlook also drove the increase in our capital expenditure guidance. We now expect a 2023 net income midpoint of $2.49

Working capital cash usage was lower by approximately $32 million driven by raw material price declines and working capital initiatives under our turnaround strategy. So this is really one of the really very positive things about this proposed merger that we will have some synergies, but we are really not competing product by product.

While our call today will focus on the results of first-quarter 2024, I do want to provide a few updates on the merger process. See the 10 stocks » *Stock Advisor returns as of May 6, 2024 First, we received overwhelming shareholder approval of the merger on March 12th, helping us achieve a key milestone in the process.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content