This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

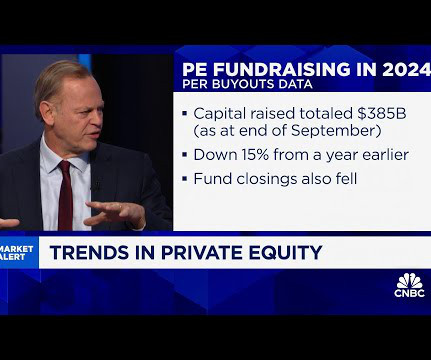

Buyout firms have long relied on controversial loans backed by equity stakes to enhance fund returns, but growing investor criticism has triggered a slowdown, according to a report by Bloomberg UK. This shift partly reflects a rebalancing of power, enabling LPs in private equity funds, such as pensionfunds to exert influence over GPs.

Annaly buys mortgages that are pooled into bond-like securities, often called something like a collateralized mortgage obligation (CMO). Annaly is really designed to be owned by total return investors who focus on asset allocation (such as insurance companies and pensionfunds). Image source: Getty Images.

It buys pools of mortgages that have been brought together into bond-like securities, often called something along the lines of collateralized mortgage obligations (CMOs). In fact, Annaly is most appropriate for institutional-level investors with a focus on asset allocation , as it provides exposure to the mortgage debt market.

Laura Benitez and Nishant Kumar of Bloomberg report hedge funds draw pension money to riskiest corner of a $1.3 Pension plans and insurers have been piling into funds that invest in equity tranches of collateralized loan obligations in recent months, according to several asset managers who spoke on the condition of anonymity.

A mortgage REIT like AGNC buys mortgages that have been pooled into bond-like securities, often referred to as something like a collateralized mortgage obligation (CMO). Generally, leverage is employed so that more CMOs can be bought, with the CMO portfolio acting as collateral for the loan.

It owns mortgages that have been pooled together into bond-like securities, which are usually called something like a collateralizeddebt obligation (CDO). Entities like insurance companies and pensionfunds could find it a very useful tool. However, it is not a traditional property-owning REIT.

Layan Odeh of Bloomberg reports CPPIB plows at least $5 billion into private equity in three months: Canada Pension Plan Investment Board poured at least $5 billion into private equity in the last three months of 2024 as the asset class regained appeal. 31, according to Bloomberg calculations. two packaging companies.

A higher cost of debt and slower economic growth have created a tough investing environment, pushing down the value of some private assets that pensionfunds own. Private credit has been one of the best-performing asset classes for some large pensionfunds in recent years, often earning double-digit percentage gains.

trillion of assets under management supporting defined benefit and defined contribution plans, PGIM serves more than half of the world's 300 largest pensionfunds. I mean my recollection is those debt protection products at very attractive margins. As a market leader with nearly $0.5

Paula Sambo of Bloomberg reports Canada pensionfund's credit head wants to take advantage of leveraged buyout boom: Canada’s largest pensionfund plans to nearly double the size of its credit holdings over the next five years, and it’s counting on an upturn in leveraged buyouts to generate some of that growth.

Funds raised money, bought businesses, loaded them with debt, exited at a profit and convinced happy investors to do it all over again — at ever greater scale. Some top industry figures don’t dispute the perils of gulping down more and more varieties of debt. “On Surging borrowing costs have stalled that engine.

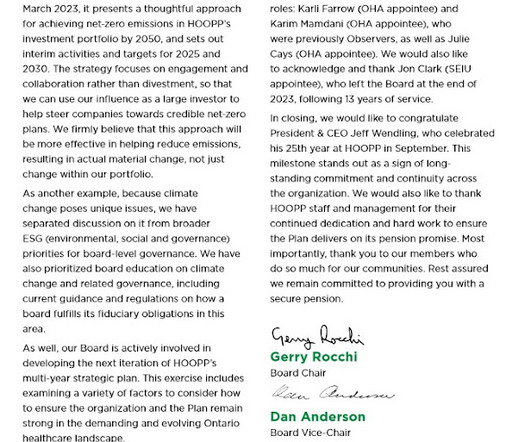

The Healthcare of Ontario Pension Plan (HOOPP) is just one of the numerous pensionfund and major ILS investors we track in our directories here. First, read my comment covering HOOPP's 2022 results where the plan remains fully funded despite losing 8.6%

In addition, some important public debt market investment opportunities in Canada have been getting smaller. For example, the federal government recently announced it would stop issuing real return bonds – an important liability matching asset for many defined benefit pensions in Canada.

Paula Sambo of Bloomberg also reports real-return bonds reap gains for HOOPP: Canadian inflation-protected securities known as real-return bonds are reaping gains for one of the country’s largest pensionfunds during a turbulent period for fixed-income markets. The pensionfund manager’s total assets increased to $112.6-billion,

Which is run by many insurance companies, pensionfunds who use Aladdin, and it’s a commercial enterprise for the firm. Didn’t it start as a bond shop, catering to pensionfunds and foundations? I mean, it started as largely mortgages, fixed income bonds shop, and you know, create a closed end funds.

Perhaps most famously you guys put on a CO bet, a collateralizeddebt obligation bet that was designed to do well if housing made some extreme moves and it was non-directional, it was hedged. The banks would have an equity trading desk and they’d have a debt desk, right? What about the refinancing of their debt?

They grew a business where they issued junk debt. So the initial idea of leveraged buyouts very high inflation really was financial engineering, truthfully, back in those days, because if you had 95 parts debt, and 5 parts equity, and 10 percent inflation, you know, you could triple your equity with no unit growth at all.

In fact, virtually all of our drawdown funds we've launched in our history, have been profitable for our investors. Our performance has helped secure retirees' pensions, fund students educations, pay healthcare benefits, and protect and grow the savings of individual investors. banks with an average of 12 times leverage.

Invested £93 million in a debt facility to Vårgrønn, owner of a 20% stake in Dogger Bank Wind Farm, which is an offshore wind farm currently under construction, located off the coast of the U.K. 7) Gordon Pape wrote and op-ed for the Globe and Mail stating the Canada Pension Plan changes will raise contributions at a very wrong time.

In addition to BMW and Volkswagen AG , Northvolt’s top investors included Goldman Sachs’s asset management arm, Denmark’s biggest pensionfund ATP, Baillie Gifford & Co. funds and a number of Swedish entities. Northvolt will also have access to about US$145 million in cash collateral.

So you could say instead of buying a million dollars of the s and p 500, I’m gonna take $50,000, use it as cash collateral to buy s and p 500 futures, a million dollars of s and p 500 futures, which will give me the total return. 00:28:05 [Speaker Changed] Exactly. So 00:28:20 [Speaker Changed] That’ll be equivalent.

That was sort of unfathomable at the time, that someone could buy a giant, publicly traded company strictly with low-cost debt. Well, first of all, the big fee that really ends up, and this is not a fee to the private equity firm, but the big problem with many of these deals is the debt interest costs, okay? MORGENSON: Absolutely.

00:16:44 [Speaker Changed] And, and, and for those people who may not be familiar with the London Interbank offered rate offered rate literally was a survey where they call up various bond debts and say, so what are you charging for an overnight loan? You need to come up with more collateral. I’m sorry.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content