This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Companies that pay dividends display a commitment to shareholders and tend to have prudent capital management. dividend yield The Blackstone Secured Lending Fund is a business development corporation ( BDC ) that invests in private company debt to generate income for dividend-focused investors. Ares Capital has a 9.7%

That will further reduce its total assets, and reduce its financial flexibility to borrow money at an attractive interest rate, as it will have less collateral. billion in debt, it may well have to further liquidate assets and dramatically curb its expenses by even more than it has planned to do so far. And, with $33.6 billion more.

We have a packed agenda lined up for the next three days, and we're excited to see our customers, partners, analysts, shareholders, and employees, all in person to share our passion for BI, AI, bitcoin, and innovation. billion in equity in a manner that we believe to be creative to existing shareholders. Debt financing.

Rather than selling off shares of Icahn Enterprises and incurring capital gains taxes as a result, Icahn had pledged a huge portion of his Icahn Enterprises holdings as collateral. That might not be enough to put all of Hindenburg's concerns to rest, but it made shareholders a lot more comfortable with Icahn Enterprises.

However, it wasn't great news, as the company was able to both push out some debt maturities and raise cash in the equity markets.but at a cost. The company also agreed to have these notes secured by a 49% stake in New Fortress' Brazil operations, giving creditors more collateral than they had prior. Of note, chairman and CEO Wesley R.

The difference between the monthly rental income and the debt payments constitutes the pool of money that the company can then use to cover its operating expenses and provisions for future investments, with the remainder of the cash flowing to shareholders as the dividend. billion in debt. It has a total of $10.1

We also maintained our disciplined approach to capital deployment, while continuing to invest in our businesses and returning excess capital to shareholders. We remain thoughtful in our capital deployment, preserving financial strength and flexibility, investing in our businesses for long-term growth and returning capital to shareholders.

Therefore, most of its Bitcoin transactions were funded through debt and equity. First, the company's debt has exploded from approximately $531 million in net cash to $2.1 billion in net debt since its spending spree began. MSTR Net Financial Debt (Quarterly) data by YCharts. What could go wrong for MicroStrategy?

In fact, REITs avoid corporate-level taxation as long as they pass at least 90% of their taxable income on to shareholders via dividends. So it makes complete sense that dividends are a big piece of the way Annaly Capital provides returns to shareholders. Dividends from REITs are taxed at an investor's regular income tax rate.)

Liquidity consisted of $578 million in unrestricted cash with a remaining in MSR line capacity, which is fully collateralized and immediately available. We feel good about the ability to continue to earn good returns for our shareholders. We look at all these portfolios. We run them. And we do call that out separately.

Those four parts are: one, we look for businesses with good returns on capital that don't use too much debt. Five years ago, at June 30, 2019, we had total net investments, that is our entire investment portfolio plus cash minus debt of $17.5 I think that this ought to produce excellent returns for our shareholders over time.

Default Risk -- Most baby bonds are classified as unsecured debt of the issuer. In other words, they're not backed by any underlying assets or collateral. If an issuer were to default, baby bondholders would get paid only after the claims of secured debt holders were met.

Most dividend-focused investors should probably own a few, given that they are specifically designed to pass income on to shareholders. However, some REITs own less desirable properties than others, and some REITs use too much debt. Annaly is a complex company I generally love REITs. Image source: Getty Images.

billion of transaction volume was driven by strong debt brokerage volume of $3.3 Our clients need capital, and our debt brokerage team did a fantastic job finding the appropriate capital for their needs. million premium write-off from the refinancing of acquired debt, and a $7.5 billion, up 40% year over year.

Both investments are subject to approval by CWEN's independent directors and are expected to be funded with existing sources of liquidity, such as retained CAFD generated over the next few years and excess debt capacity, which Sarah will discuss in more detail in the financial summary section. in CAFD per share for our shareholders.

We used most of that cash to pay down over $550 million of debt, bringing our net debt down to $3.9 billion, our lowest debt level since we were just a mining company in 2019. Q2 of 2023 was our largest quarterly debt reduction in company history. We also returned nearly $100 million to shareholders by buying back 6.5

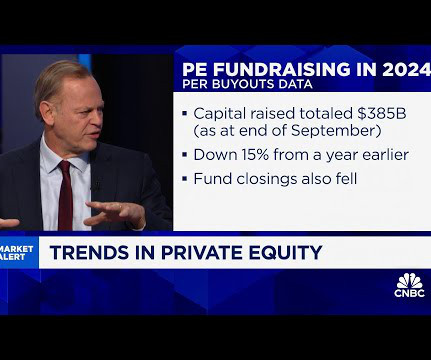

Investors have begun allocating more to private equity strategies than private debt, according to iCapital, which has more than $200 billion in alternative assets on its marketplace for money managers. Axel Springer SE will remain as a minority co-shareholder in the classified businesses, with an approximate 10% ownership stake.

billion in shareholder remuneration with payment in September. Since 2021, the total amount distributed in dividends and interest on capital translated into a 27% yield to our shareholders. billion from bond issuance, whose proceeds were mostly used to repurchase $500 million of higher cost debt and to repurchase $1.4

Our plan to source corporate growth capital is first from retained CAFD; second, with access corporate debt capacity in line with our target BB rating; and third, we may lead to issue external equity to fund investments to the extent such investment would be sufficiently accretive to shareholders. We also recognize that we had $2.1

billion, and we raised $525 million from debt investors, secured, in part, by the Deepwater Titan's five-year contract. By timely and opportunistically addressing certain debt maturities, we provided additional comfort to investors about our liquidity position. This operational performance is not by chance.

Bitcoins purchase their proceeds from Capital Markets activities, including equity and debt issuances are held at MicroStrategy, a wholly owned subsidiary of MicroStrategy. Our outstanding debt and-convertible notes remain unchanged at a total $2.2 These Bitcoins are not pledged to our Senior Secured Notes and are fully unencumbered.

The excess cash generated by our business is then dynamically allocated to our three capital allocation priorities: Deleveraging; selective M&A and return of capital to shareholders. As of June 30, our net debt-to-EBITDA ratio reached at 3.7 times year over year with net debt reached US$73.8 times down from 3.86

But in regards to selling those assets -- I mean, we always analyze different options in order to maximize shareholder value, but the business as a whole is performing well and generating cash. So, you have been able to access the volume from other players, and the collateral is working well as of now?

And within these coupons, only a small fraction of our pools are backed by generic collateral and approximately 70% have what we would characterize as high-quality prepayment protection and the benefits of our collateral selection were best seen in the latest prepayment report. We don't need to.

Our disciplined approach to capital deployment enables us to effectively balance investing in the long-term growth of our businesses with returning capital to shareholders. In the fourth quarter, we returned over $700 million of capital to shareholders. We have cash and collateral balances that earn short-term yields.

We closed out the year on a strong note with fourth-quarter financial results above our expectations as we continue to generate strong earnings and cash flows while returning capital to shareholders. I would encourage you all to check out Manufacture Like a Pro series of videos and other marketing collateral. We generated $77.8

As with prior programs, we may use the proceeds for general corporate purposes, which include the purchase of Bitcoin as well as the repurchase or repayment of our outstanding debt. Our outstanding debt and convertible notes remain unchanged at a total of $2.2 billion with a bundled weighted average interest rate of approximately 1.6%.

The combination of our next-generation cloud-native API technology will allow us to create new products and build a bespoke community bank for each industry we serve, while our industry remains woefully stuck in the mud, supporting and maintaining billions of lines of ancient code that they call technical debt. It is collateralized.

Total shareholder distributions in the quarter were $122 million, including $100 million of share repurchases. Net debt declined sequentially to NOK 260 million. Importantly, we now have access to the lower-cost investment-grade bond market for any future term debt needs. Moving to our guidance.

Now a second factor leading to the decline in yields in the fourth quarter is this change in debt issuance dynamics as the treasury chose to issue incremental supply in the front end of the yield curve, taking advantage of the record amount of cash in money market funds while exerting less pressure on longer-term yields.

Our press release and the shareholder letter were issued earlier today and are posted on the Investor Relations section of our website. A reconciliation of GAAP non-GAAP results other than with respect to our non-GAAP financial outlook is provided in today's press release and in our shareholder letter. I'll elaborate on this later.

I guess the real question is around timing and how you see your ability to free up some of that restricted cash and start to bring on some of those closed one or more of those deals that you're talking about in the shareholder letter? So, you talked about corporate debt solutions. I mean I really don't have any debt.

C3 AI and Microsoft will create joint webinar sales collateral to train the Microsoft and C3 AI sales forces on our joint offering solutions and value propositions. There is no question that this has been and continues to be in the best interest of our shareholders. Total allowance for bad debt remains at less than $0.5

I know our shareholders want to own a company they can count on for profitability and growth with strong ethics, values, and integrity. As of December 31st, 2023, consolidated gross debt was $4.1 Debt, net of our $1.2 At the same time, we are funding high-return projects for the benefit of our customers and shareholders.

I would point out that corporate debt interest expense increased from $67 million to $75 million sequentially, reflecting two months of interest expense from the senior notes issued in August. Also, we've chosen very high-quality collateral where customers have low note rates and large equity cushions.

I am proud of the work we have done during my time at Planet Fitness to deliver value to our franchisees and our shareholders. We are capitalizing on our strong momentum, along with our proactive forward-thinking mindset to drive enhanced value for shareholders. Now to our debt. I know that we have a lot more work to do.

And consistent with prior quarters, we favored high-quality prepayment-protected collateral with durable cash flows. While repo rates remained stable, even declining 2 basis points in Q2, securitized debt expense increased in Q2 due to the high volume of securitizations we completed in the first six months of 2024.

Our disciplined approach to capital deployment, coupled with the added capital flexibility achieved through our de-risking transactions, enables us to effectively balance investing in the long-term growth of our businesses with returning capital to shareholders. Turning to Slide 12 and in summary. dollar and yen-denominated?

Following our successful $750 million debt issuance in June, we used the proceeds to purchase a like amount of securities with a similar duration in order to maintain a relatively neutral balance sheet position and bolster liquidity. In some instances, we're adding additional collateral to support the credit. billion to $4.8

Over the last two years, we found some of the best OAS yields on deep out-of-the-money collateral, and you've heard us comment on the high-quality stable cash flow those pools will provide us for years to come. How much of it is debt that you -- the advances, I guess, the funding lines? So it's all debt. Your line is now open.

Those managers experienced in due diligence with sufficient scale to build out funds with higher-quality collateral and low leverage in defensive sectors may be able to provide a better cushion. forward base rates, which implies that nearly 20% of the private credit market does not have sufficient cash flow to cover their debt.

Underwriting fees were up meaningfully with debt up 56% and equity up 26%, primarily driven by favorable market conditions. And to be fair, your long-term shareholders really don't care about whether it's 87% or 85%, right? Our shareholders will be very well-served by just waiting. 1 with year-to-date wallet share of 9.1%.

And to note, we've achieved a 6% return year to date and kept book value largely unchanged, notwithstanding heightened uncertainty caused by the changing path of Fed rate hikes, the regional banking turbulence, and debt ceiling negotiations. We also reduced our holdings of seasoned intermediate coupons and 15-year MBS.

The rebound in Banking gained speed during the quarter, led by near-record levels of investment-grade debt issuance as improved market conditions enables issuers to pull forward activity. billion in capital to our common shareholders, and that includes $500 million through share buyback. During the first quarter, we returned $1.5

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content