This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Buyout firms have long relied on controversial loans backed by equity stakes to enhance fund returns, but growing investor criticism has triggered a slowdown, according to a report by Bloomberg UK. This shift partly reflects a rebalancing of power, enabling LPs in private equity funds, such as pensionfunds to exert influence over GPs.

And such REITs often employ leverage, usually using their loan portfolio as collateral, to enhance returns. In some ways, a mortgage REIT is more like a mutual fund than a company. That list might include pensionfunds, endowments, and insurance companies. And they are certainly nothing like a landlord.

Mortgage REITs buy mortgages that have been cobbled together into bond-like securities, often called collateralized mortgage obligations (CMO). This is vastly different from property-owning REITs, which are fairly simple to understand using kitchen table finance. Basically, you buy a property and rent it out. We can do it, or can we?

Annaly buys mortgages that are pooled into bond-like securities, often called something like a collateralized mortgage obligation (CMO). Annaly is really designed to be owned by total return investors who focus on asset allocation (such as insurance companies and pensionfunds). Image source: Getty Images.

It buys pools of mortgages that have been brought together into bond-like securities, often called something along the lines of collateralized mortgage obligations (CMOs). Insurance companies and pensionfunds are the types of investors that might appreciate this REIT. Annaly is what is known as a mortgage REIT.

Laura Benitez and Nishant Kumar of Bloomberg report hedge funds draw pension money to riskiest corner of a $1.3 Laura Benitez and Nishant Kumar of Bloomberg report hedge funds draw pension money to riskiest corner of a $1.3 trillion credit market: A high-stakes trade in the riskiest corner of a $1.3

Investors in the Fund, which were a mix of numerous new investors as well as existing New Mountain Net Lease investors, include pensionfunds, insurance companies, asset managers, endowments, family offices and high net worth individuals. investment giant Blackstone is reportedly weighing offers for half its stake in the real.

A mortgage REIT like AGNC buys mortgages that have been pooled into bond-like securities, often referred to as something like a collateralized mortgage obligation (CMO). Generally, leverage is employed so that more CMOs can be bought, with the CMO portfolio acting as collateral for the loan.

Rather, it buys mortgages that have been pooled into bond-like securities, sometimes called collateralized mortgage obligations or something similar. Mortgage REITs usually use leverage in an effort to enhance returns, with the mortgage securities they own acting as collateral.

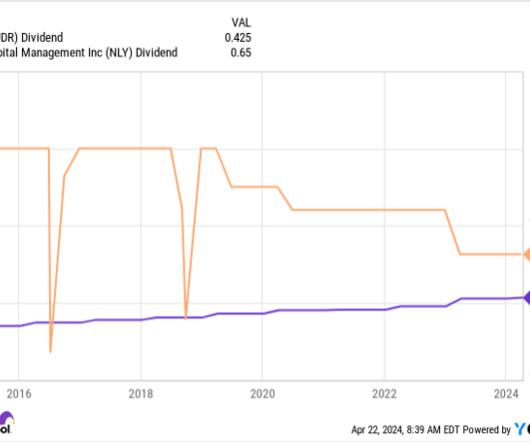

UDR Dividend data by YCharts To be fair, Annaly isn't a bad REIT -- it's just meant for large institutional investors, like pensionfunds, that focus on total return (which assumes dividend reinvestment) and asset allocation. That's very different from what most small dividend investors are looking for.

Technically, mortgage REITs like Annaly usually buy bond-like securities that represent a pooled collection of mortgages, often called something like a collateralized mortgage obligation (CMO). The portfolio of mortgages is often used as collateral for that leverage, which can be a problem if CMO values fall dramatically.

In this way, it's kind of like a mutual fund that focuses on mortgages. In fact, the most common asset allocators are large investors like pensionfunds, family offices, and endowments. They tend to use leverage, often with the portfolio of mortgage securities acting as collateral. Image source: Getty Images.

Oak Hill Advisors (“OHA”) served as a Lead Arranger for the unitranche financing to fund Bain Capital Private Equity’s (“Bain Capital”) acquisition of Harrington Industrial Plastics (“Harrington”) from Nautic Partners.

you would get from an S&P 500 index fund. In this case, it generally owns mortgages that have been pooled together to trade like a bond, often called something like a collateralized mortgage obligation (CMO). The Motley Fool has positions in and recommends Vanguard Specialized Funds-Vanguard Real Estate ETF.

It owns mortgages that have been pooled together into bond-like securities, which are usually called something like a collateralized debt obligation (CDO). Entities like insurance companies and pensionfunds could find it a very useful tool. However, it is not a traditional property-owning REIT.

Annaly is a mortgage REIT, which means it buys mortgages that have been pooled into what are often called collateralized mortgage obligations (CMOs), or something similar. Traditionally the list would include large, institutional investors like pensionfunds that focus on asset allocation.

Blackstone's unique investment business Blackstone manages investments for big money managers, including pensionfunds and institutional investors, and its $1 trillion in AUM makes it one of the largest asset managers in the world. billion to investors from the nearly $70 billion fund. Here's why this news is a big deal.

Layan Odeh of Bloomberg reports CPPIB plows at least $5 billion into private equity in three months: Canada Pension Plan Investment Board poured at least $5 billion into private equity in the last three months of 2024 as the asset class regained appeal. Canadas largest pension notched a 3.8% 31, according to Bloomberg calculations.

A higher cost of debt and slower economic growth have created a tough investing environment, pushing down the value of some private assets that pensionfunds own. Private credit has been one of the best-performing asset classes for some large pensionfunds in recent years, often earning double-digit percentage gains.

trillion of assets under management supporting defined benefit and defined contribution plans, PGIM serves more than half of the world's 300 largest pensionfunds. US fundedpension risk transfer transactions of $6.3 As a market leader with nearly $0.5 Institutional retirement sales totaled $11 billion in the quarter.

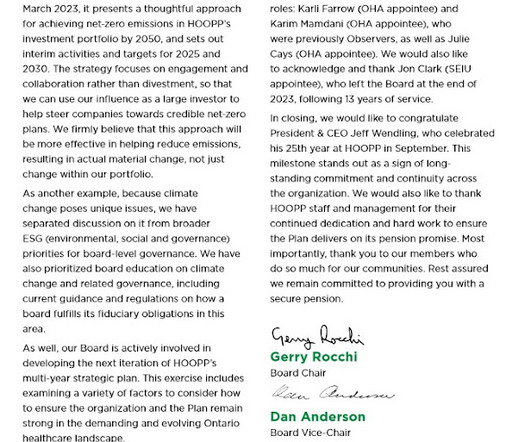

Artemis reports the Healthcare of Ontario Pension Plan (HOOPP) grew ILS investments 35% in 2022: Large Canadian institutional retirement fund, the Healthcare of Ontario Pension Plan (HOOPP), grew its allocation to insurance-linked securities (ILS) investments in 2022, with the asset class nearing 1% of its overall portfolio by the end of the year.

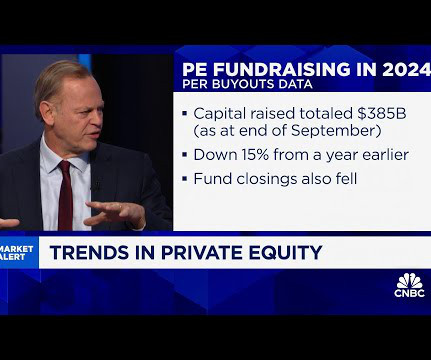

Funds raised money, bought businesses, loaded them with debt, exited at a profit and convinced happy investors to do it all over again — at ever greater scale. Concerns about PIK loans have also begun to impact the people who provide them, often private credit funds. Surging borrowing costs have stalled that engine.

With nearly half a trillion dollars of assets under management supporting defined benefit and defined contribution plans, PGIM is a market leader, servicing more than half of the world's 300 largest pensionfunds, including over two-thirds of the largest 100 U.S. pension plans, and is the largest pensionfund manager in Japan.

They’re talking about asset management firms, in which public pensionfunds often have investments, supporting shareholder proposals meant to achieve social justice or climate objectives yet of dubious financial value. Second, these anti-ESG articles miss the mark when it comes to Canada's large pension investment managers.

Freschia Gonzales of Wealth Professional reports HOOPP achieves 9.38% return in 2023: The Healthcare of Ontario Pension Plan (HOOPP) announced a return of 9.38 This performance secures the Plan's funded status at 115 percent, demonstrating its robust financial health by having $1.15 in assets for every dollar owed in pensions.

But he spent most of his career allocating capital to various hedge funds, private equity, venture, etc. And so my summer job at business school, I worked for a hedge fund that Yale had money with. RITHOLTZ: Hedge fund, private equity, and Yale endowment, right? Now there’s 11,000 hedge funds and 500 are generating alpha.”

See the 10 stocks *Stock Advisor returns as of July 17, 2023 Also note that nothing on this call constitutes an offer to sell or a solicitation of an offer to purchase an interest in any Blackstone fund. In fact, virtually all of our drawdown funds we've launched in our history, have been profitable for our investors.

The pensionfund had solid returns from its portfolio of public stocks, which gained 10.4 But stocks make up only 19 per cent of the pensionfund’s assets after it shifted billions of dollars from equities into government bonds and credit investments, seeking to take advantage of high interest rates. dollar to earn a 4.4-per-cent

Paula Sambo of Bloomberg reports Canada pensionfund's credit head wants to take advantage of leveraged buyout boom: Canada’s largest pensionfund plans to nearly double the size of its credit holdings over the next five years, and it’s counting on an upturn in leveraged buyouts to generate some of that growth.

As a result, we invest a significant percentage of the funds we manage on behalf clients outside Canada (the percentage varies over time – but today it is approximately 65%), and mostly in developed markets (approximately 93% today). This allows us to diversify client portfolios and expand our investment opportunity set.

They are not like any other fund that you’ll hear me talk about. For me, I sat mostly in their internal, really an internal hedge fund. So Alec Lilitz and Ross Lazar founded the firm and, you know, I did join the day we launched our, our main fund. They have an incredible track record. It’s immense.

BARRY RITHOLTZ, HOST, MASTERS IN BUSINESS: This week on the podcast, another extra special guest, Robin Grew, President of Man Group, $145 billion publicly traded hedge fund in the UK, and soon to be Man Group’s CEO. GREW: So, Man is a — as you said hundred million – 145-billion-dollar hedge fund. Is that right?

They have $37 billion in clients and their own funds, of which they have invested across a variety of disciplines from credit to strategic capital, as well as taking companies private and helping them grow into something more substantial than they’ve been in the past. That’s our private equity fund. RITHOLTZ: Right.

And in fact, it wasn’t even luck because I left in ’08 and I started my hedge fund. And if somebody said what would be the worst month in history to start a credit hedge fund, May of ’08 may have been the one or certainly closer. We haven’t even talked about the various funds you run. RIEDER: Yeah.

The Fund, which includes the combination of the base CPP and additional CPP accounts, achieved a 10-year annualized net return of 9.6%. For the quarter, the Fund’s net return was 0.1%. For the period, the Fund’s net return was negative 0.7%.

In addition to BMW and Volkswagen AG , Northvolt’s top investors included Goldman Sachs’s asset management arm, Denmark’s biggest pensionfund ATP, Baillie Gifford & Co. funds and a number of Swedish entities. Still, work on a bridge funding deal continued, with an agreement coming close to fruition as recently as October.

Not only did he stand up a research shop from a dorm room in college and started selling model portfolios to fund managers, but eventually created a suite of first mutual funds. 00:09:05 [Speaker Changed] How, how did the fund actually perform when it was live 00:09:09 [Speaker Changed] Quite well, right? Where did they go?

You also had this thing called monitoring fees, where a company that was purchased by a private equity fund or firm would have to pay the firm fees for its monitoring, for its oversight, for its management expertise that it was providing to the company. MORGENSON: It can be collateralized loan obligations, now it’s big private debt.

I remember it really well because I just finished building this house in West Virginia and we, we were taking occupancy in early August, and it was, it was literally the same day that BMP Paraba shut off redemptions from some of their mutual funds, caused all sorts of chaos in Europe. We were running the commercial paper funding facility.

The actuarial change helped cause its funding ratio its assets, compared with its future pension obligations, or liabilities to slip for a second straight year. The plan closed 2024 at a funding ratio of 111 per cent, versus 115 per cent at the end of 2023, and 117 per cent for 2022. markets but have begun to outperform.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content