This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This shift partly reflects a rebalancing of power, enabling LPs in private equity funds, such as pensionfunds to exert influence over GPs. Using NAV loans for distributions is somewhat like kicking the can down the road, said Christian Wiehenkamp, Chief Investment Officer of Perpetual Investors.

Mortgage REITs buy mortgages that have been cobbled together into bond-like securities, often called collateralized mortgage obligations (CMO). This is vastly different from property-owning REITs, which are fairly simple to understand using kitchen table finance. Basically, you buy a property and rent it out. We can do it, or can we?

Annaly buys mortgages that are pooled into bond-like securities, often called something like a collateralized mortgage obligation (CMO). Annaly is really designed to be owned by total return investors who focus on asset allocation (such as insurance companies and pensionfunds). Image source: Getty Images.

And such REITs often employ leverage, usually using their loan portfolio as collateral, to enhance returns. In some ways, a mortgage REIT is more like a mutual fund than a company. That list might include pensionfunds, endowments, and insurance companies. And they are certainly nothing like a landlord.

It buys pools of mortgages that have been brought together into bond-like securities, often called something along the lines of collateralized mortgage obligations (CMOs). Insurance companies and pensionfunds are the types of investors that might appreciate this REIT. Annaly is what is known as a mortgage REIT.

Laura Benitez and Nishant Kumar of Bloomberg report hedge funds draw pension money to riskiest corner of a $1.3 Pension plans and insurers have been piling into funds that invest in equity tranches of collateralized loan obligations in recent months, according to several asset managers who spoke on the condition of anonymity.

Rather, it buys mortgages that have been pooled into bond-like securities, sometimes called collateralized mortgage obligations or something similar. Mortgage REITs usually use leverage in an effort to enhance returns, with the mortgage securities they own acting as collateral.

A mortgage REIT like AGNC buys mortgages that have been pooled into bond-like securities, often referred to as something like a collateralized mortgage obligation (CMO). Generally, leverage is employed so that more CMOs can be bought, with the CMO portfolio acting as collateral for the loan.

Technically, mortgage REITs like Annaly usually buy bond-like securities that represent a pooled collection of mortgages, often called something like a collateralized mortgage obligation (CMO). The portfolio of mortgages is often used as collateral for that leverage, which can be a problem if CMO values fall dramatically.

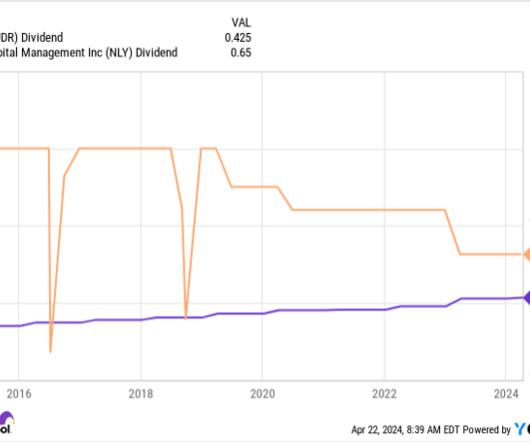

UDR Dividend data by YCharts To be fair, Annaly isn't a bad REIT -- it's just meant for large institutional investors, like pensionfunds, that focus on total return (which assumes dividend reinvestment) and asset allocation. That's very different from what most small dividend investors are looking for.

Investors in the Fund, which were a mix of numerous new investors as well as existing New Mountain Net Lease investors, include pensionfunds, insurance companies, asset managers, endowments, family offices and high net worth individuals. Source: Business Wire Can’t stop reading? billion rupees.

It owns mortgages that have been pooled together into bond-like securities, which are usually called something like a collateralized debt obligation (CDO). Entities like insurance companies and pensionfunds could find it a very useful tool. However, it is not a traditional property-owning REIT.

In fact, the most common asset allocators are large investors like pensionfunds, family offices, and endowments. They tend to use leverage, often with the portfolio of mortgage securities acting as collateral. That's not likely to be a small income investor. That increases risk.

Annaly is a mortgage REIT, which means it buys mortgages that have been pooled into what are often called collateralized mortgage obligations (CMOs), or something similar. Traditionally the list would include large, institutional investors like pensionfunds that focus on asset allocation.

In this case, it generally owns mortgages that have been pooled together to trade like a bond, often called something like a collateralized mortgage obligation (CMO). As that suggests, Annaly invests in mortgages. A unique REIT that most should avoid The truth is that Annaly isn't really meant for average investors.

OHA manages approximately $61 billion of capital across credit strategies in pooled funds, collateralized loan obligations and single investor mandates as of June 30, 2023.

Blackstone's unique investment business Blackstone manages investments for big money managers, including pensionfunds and institutional investors, and its $1 trillion in AUM makes it one of the largest asset managers in the world. Here's why this news is a big deal. What sets Blackstone apart from competitors is its investing style.

A higher cost of debt and slower economic growth have created a tough investing environment, pushing down the value of some private assets that pensionfunds own. Private credit has been one of the best-performing asset classes for some large pensionfunds in recent years, often earning double-digit percentage gains.

Layan Odeh of Bloomberg reports CPPIB plows at least $5 billion into private equity in three months: Canada Pension Plan Investment Board poured at least $5 billion into private equity in the last three months of 2024 as the asset class regained appeal. 31, according to Bloomberg calculations. billion 10-year net return of 9.2% billion.

trillion of assets under management supporting defined benefit and defined contribution plans, PGIM serves more than half of the world's 300 largest pensionfunds. As a market leader with nearly $0.5

Paula Sambo of Bloomberg reports Canada pensionfund's credit head wants to take advantage of leveraged buyout boom: Canada’s largest pensionfund plans to nearly double the size of its credit holdings over the next five years, and it’s counting on an upturn in leveraged buyouts to generate some of that growth.

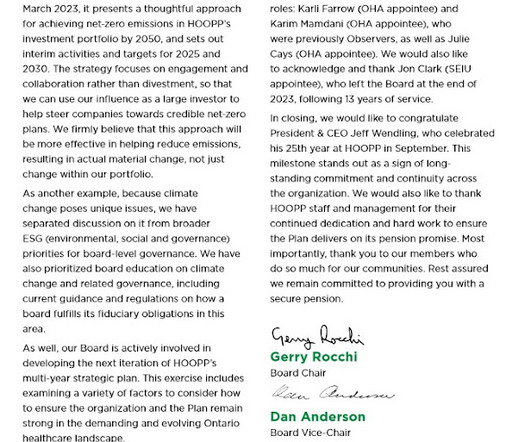

The Healthcare of Ontario Pension Plan (HOOPP) is just one of the numerous pensionfund and major ILS investors we track in our directories here. First, read my comment covering HOOPP's 2022 results where the plan remains fully funded despite losing 8.6%

They’re talking about asset management firms, in which public pensionfunds often have investments, supporting shareholder proposals meant to achieve social justice or climate objectives yet of dubious financial value. Nor is it supported by the empirical evidence.

NAV lenders sometimes charge interest in the mid to high teens, and some borrowers have used holiday homes, art and cars as collateral. One senior pensionfund executive says they try to avoid managers who use NAV as they view it as firms being lazy about exits, adding that they’d prefer to crystallize losses than get distributions this way.

Even in jurisdictions where hedging is more feasible, hedging currency requires access to liquidity to post as collateral. There's been a lot of discussion lately on why Maple 8 pensionfunds do not invest more in Canada, specifically in Canadian equities. Investors need be prepared for and accept this added risk.

With nearly half a trillion dollars of assets under management supporting defined benefit and defined contribution plans, PGIM is a market leader, servicing more than half of the world's 300 largest pensionfunds, including over two-thirds of the largest 100 U.S. pension plans, and is the largest pensionfund manager in Japan.

The pensionfund had solid returns from its portfolio of public stocks, which gained 10.4 But stocks make up only 19 per cent of the pensionfund’s assets after it shifted billions of dollars from equities into government bonds and credit investments, seeking to take advantage of high interest rates. dollar to earn a 4.4-per-cent

Paula Sambo of Bloomberg also reports real-return bonds reap gains for HOOPP: Canadian inflation-protected securities known as real-return bonds are reaping gains for one of the country’s largest pensionfunds during a turbulent period for fixed-income markets. The pensionfund manager’s total assets increased to $112.6-billion,

Which is run by many insurance companies, pensionfunds who use Aladdin, and it’s a commercial enterprise for the firm. Didn’t it start as a bond shop, catering to pensionfunds and foundations? I mean, it started as largely mortgages, fixed income bonds shop, and you know, create a closed end funds.

Perhaps most famously you guys put on a CO bet, a collateralized debt obligation bet that was designed to do well if housing made some extreme moves and it was non-directional, it was hedged. So it, it really has and, and pensionfunds, they’re on hold today. I wanted to talk about a couple of trades from that era.

And the Japanese regulators were having a tough time with cross collateralization and issues about whether there were balance sheet accounting issues. In part because I again benefited from being in the mix when we were the second bank that was raided by the Japanese regulators after they’d gone into Credit Suisse. Is that right?

And he said, “Well, it has to be this and that “and it has to be collateralized with a letter of credit.” Public pensionfunds that manage hundreds of billion dollars can be manned by professionals that make $80 to $150,000 a year. ” And I was like, “What?” SEIDES: Yeah.

And if they don’t need a loan, we can lease them their own building back in a net lease, and have both the credit of the company and the real estate as collateral. KLINSKY: In the private equity fund and strategic equity fund, it’s the big pensionfunds in the U.S. KLINSKY: Yup.

In fact, virtually all of our drawdown funds we've launched in our history, have been profitable for our investors. Our performance has helped secure retirees' pensions, fund students educations, pay healthcare benefits, and protect and grow the savings of individual investors. banks with an average of 12 times leverage.

My take: I would say the key advantage IMCO and other large Canadian pensionfunds is certainty of cash flows and access to top private equity, real estate, infrastructure and private debt partners around the world. Leveraging these investment advantages are some of the strategies IMCO uses to enhance returns on behalf of our clients.

In addition to BMW and Volkswagen AG , Northvolt’s top investors included Goldman Sachs’s asset management arm, Denmark’s biggest pensionfund ATP, Baillie Gifford & Co. funds and a number of Swedish entities. Northvolt will also have access to about US$145 million in cash collateral.

So you could say instead of buying a million dollars of the s and p 500, I’m gonna take $50,000, use it as cash collateral to buy s and p 500 futures, a million dollars of s and p 500 futures, which will give me the total return. 00:28:05 [Speaker Changed] Exactly. So 00:28:20 [Speaker Changed] That’ll be equivalent.

MORGENSON: It can be collateralized loan obligations, now it’s big private debt. Pensionfunds, perhaps, maybe aren’t growing as much as they need them to. But so you had these dividend recaps. And it has really done a lot to attract the high net worth retail customers into that.

00:21:10 And so we started an advisory group of people, you know, hedge funds, pensionfunds, insurance companies, you know, buy side investors. You need to come up with more collateral. And at that point, the, the, the, the borrower might say, I don’t have the collateral, the building’s yours.

In late 2022, the Liberals announced they would stop issuing the popular bonds, which helped pensionfunds that pay out inflation-indexed benefits balance their assets and liabilities. Canadian bonds remain the backbone of the Funds investing strategy.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content