This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

USI Partners raised an additional $139m for its Southeast Asia-focused energy transition strategy, bringing the total fund size to $259m. These funds will support the SUSI Asia Energy Transition Fund (SAETF) and the Sustainable Asia Renewable Assets (SARA) platform. Source: Private Equity Wire Can’t stop reading?

Ron Kantowitz, managing director and head of direct lending, pointed to favourable market conditions, noting that record capital raised in the private equity sector is driving increased M&A activity and generating strong dealflow.

Shamrock Capital (Shamrock), an LA-based investment firm specialising in the media, entertainment, and communications sectors, has held the final closing of Shamrock Capital Growth Fund VI (Growth VI) and Shamrock Capital Clover Fund I (Clover I), with a combined $1.6bn in capital commitments.

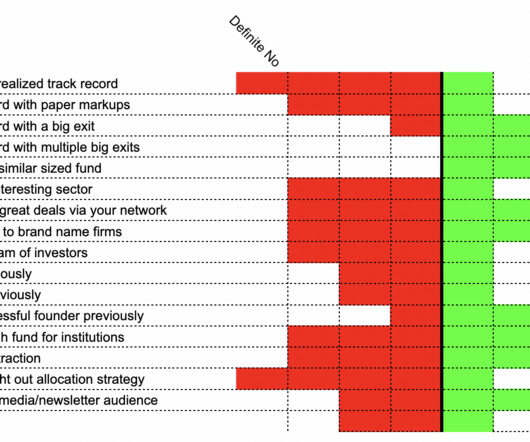

When I wrote this post about trying to measure the fundability of your startup, I kicked it off with, “You can’t” and proceeded to share all the ways that getting your companyfunded feels a bit like a craps shoot, while still trying find a method somewhere within the madness. Spinning out of a successful fund of a similar size?

The REIT has two big catalysts ahead that should increase its dealflow and ability to finance new investment opportunities. These deals enable companies to unlock the value of their real estate while providing them with the capital they can use to repay debt, expand their operations, or fund cash returns to shareholders.

Progressio SGR, the Italian private equity firm, is raising a new fund, Progressio Investimenti III, in response to LP demand and a doubling of proprietary dealflow over the past five years. As with previous funds, the money will predominantly be spent on proprietary deals and primary buyouts.

In particular, I've been looking closely at business development companies ( BDCs ). What are business development companies? At their core, they're capital providers to early-stage businesses looking for funding to get their operations off the ground. Moreover, underwriting protocols vary from one company to the next.

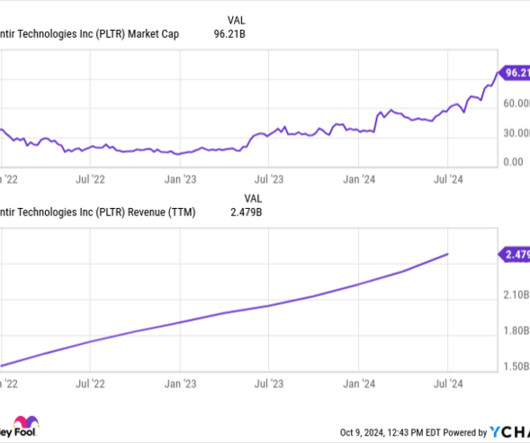

Below, I'll cover a number of catalysts that could spur even further growth for Palantir while also calling out some risks the company faces. Now that Palantir is part of the exclusive index, I would not be surprised to see the company receive more attention from large financial institutions.

Partners Group, a Swiss-based global private equity firm with $147bn in assets under management, is targeting $12bn for another private equity secondary strategy fund that will focus on deals in the Asia Pacific region, according to a report by Reuters.

Investors in the Fund, which were a mix of numerous new investors as well as existing New Mountain Net Lease investors, include pension funds, insurance companies, asset managers, endowments, family offices and high net worth individuals. Since inception, New Mountain’s net lease strategy has completed $1.9

Park Square Capital, a European private credit specialist, has successfully raised €3.4bn ($3.8bn) for its latest direct-lending fund, European Loan Partners II, which will lend to private equity-owned mid-market businesses across Europe, according to a report by Bloomberg.

Fund investing, like adulting, is boring. That’s the first thing anyone trying to raise a fund needs to understand, as well as anyone thinking about investing in one. The partner at the fund, the VC, gets to do the fun part—the meeting with founders, vetting deals, negotiating, helping, etc. So what’s the point?

Lexington Partners (“ Lexington “), a leading manager of secondary acquisition funds, today announced the completion of fundraising for Lexington Capital Partners X, L.P. (“LCP X”) with $22.7 billion of total capital commitments. per share, private equity firm Sycamore Partners.

PARTNER CONTENT The landscape of venture capital deal sourcing has evolved significantly over the past few years. Gone are the days of rapid-fire deals and a “growth-at-all-costs” mentality. This shift means that the competition for high-quality deals is intense, while the urgency to deploy capital remains high.

Benefit Street Partners (BSP), a credit-focused alternative asset manager with approximately $75bn in AUM and a subsidiary of Franklin Templeton Investments, has closed its fifth flagship direct lending vehicle, BSP Debt Fund V, with $4.7bn of capital.

When I started leading deals at First Round Capital, I sourced investments in 8 companies. We started talking about cycling and electronic shifters (which I definitely couldn’t afford) when he mentioned this new company. That leaves me out raising with two funds under my belt and no big exit and no unicorn valuations.

Every single topic about running a company has been written about ad nauseum, there are incubators, accelorators, mentoring programs, events, talks, etc. We''ve done a lot to make sure startups get all the help we can get--and it''s leading to higher companies getting off the ground. But what about investors?

It will be the 105th deal out of Brooklyn Bridge Ventures, the firm I started back in September 2012, and it will be the last deal I’ll be making out of my third fund. It will also be my last venture capital deal.

On the positive side, funding happens so rarely, that you’re inevitably going to be asked how you did it—and it’s just human nature to think that it’s something you did, versus the inherent awesomeness of the idea, the team’s relevance to the challenge, etc. It’s not me, it’s them. What counts as a rabbit? That adds risk.

If dealflow is slow, a VC will take a meeting if you and your team seem mildly interesting even if your product isn’t. Some later stage funds will take a meeting long before they ever plan on writing a check with the promise of “opportunistic” seed investments (to the guy or girl they went to grad school with).

As liquidity constraints put pressure on the private equity industry, the secondaries market is expected to grow substantially over the next twelve months, with fundraising and dealflow set to expand, according to Investec’s latest Secondaries Report, Charting a Course for Further Growth.

I went back and calculated the number of companies in the first Brooklyn Bridge Ventures portfolio who have at least one founder who is female, from an underrepresented minority group, or LGBT. A whopping 17 of the 32 companies (53%) have founders that fit into those groups. Yet, here's the thing: I'm not actually aiming for diversity.

The company's actual financial condition and the results of operations may vary materially from those contemplated by such forward-looking statements. Additionally, this call will contain references to certain non-GAAP measures, which we believe are useful in evaluating the company's performance. Then youll want to hear this.

Most of the deals you fund have already been funded by someone else, so you're most likely going to see a deal through a seed investor you probably know. No VC has a magical stream of only high quality dealflow. Plus, direct screening can be useful to a VC's future dealflow.

They’re building campuses, districts, buildings, spaces, as well as running new educational efforts and contests—basically anything they can think of to foster the growth of new and innovative companies. Very little time and effort is spent helping professional, full time investors raise capital for venture funds.

Discover the advantages of a relationship bank providing leverage on both fund and portfolio level, optimizing your investments for maximum returns. They enhance Internal Rate of Return, provide funding certainty in competitive situations, or cater for additional investments. Unlock the power of leverage in private equity.

Oak Hill Advisors (“OHA”) served as a Lead Arranger for the unitranche financing to fund Bain Capital Private Equity’s (“Bain Capital”) acquisition of Harrington Industrial Plastics (“Harrington”) from Nautic Partners. and globally.

IAIM aims to leverage the origination and proprietary dealflow capabilities of Investec’s direct lending team to deliver private market investment solutions for investors. In her previous role within Investec, she led cross-sector ESG research on UK listed companies. Forry has been with Investec for almost seven years.

PGIM Private Capital, the private capital arm of Prudential Financial $1.34tn global investment business PGIM, provided $7.5bn of senior debt and junior capital to more than 130 middle-market companies and projects globally in H1 2024. The first half of 2024 has been more stable for issuance than the same period last year.

Union Square Advisors, a technology-focused investment bank, is expecting to see an increase in technology sector deal-making in 2024, with recent positive momentum continuing over the course of the year. The report also notes that there is significant capital on the sidelines today that is available to be deployed.

Direct lenders meanwhile, doubled their activity over the same period, funding $20.6bn in buyout financing in the first half of the year. Technology firms led M&A activity, with deals amounting to $64bn.

I got the space through Bizly , a company that I invested in that just launched to the public today. I'm excited to work with Ron Shah on this company and it's a testament to the kind of long term relationships that have building the dealflow pipeline at Brooklyn Bridge Ventures. And yes, I closed that investor.

Disagreements over valuations have been a barrier for buyout firms attempting to exit their portfolio companies, according to a report by Bloomberg, which cites an Ares Management (Ares) executive speaking at this year’s IPEM in Cannes. If they can wait, why would you want to put your average company up for sale right now?”

That isn't a huge deal, since it's normal for acquisitions to be lumpy. And the company has $2.6 billion in liquidity available to fund new deals, so closing acquisitions won't be an issue of investment capacity. That's good news, though the timing is hard to predict. Some of that could roll over into 2025.

Thill's primary thesis was that there are better investment opportunities among big tech companies than Palantir, despite its progress in its market. Some short-sellers view Palantir as a glorified government contractor, given its heavy reliance on public sector dealflow. of its combined portfolio. Image Source: Getty Images.

I believe that the next generation of top companies are far more likely to be founded by people not on VC radars today. That believe has not only translated into the most diverse portfolio run by an investor who looks like me, with over 50% of the teams including diverse founders, but also into top quartile returns in our last fund.

but in a moment of clarity, I realized that everything I get--dealflow, fund investors, opportunities to hire people, etc.--comes To be a good VC, you're going to offer up a lot of time to companies that may never pay back a dime--or even to deals you never wind up doing. There's no magic flow of great dealflow.

Imagine this: You conduct a survey of 250 Series B and beyond CROs and VPs of Sales for B2B SaaS companies to understand everything about what drives sales success and what profiles of candidates turned out to be the most successful hires. What successful founder wouldn’t reach out to me to brainstorm strategies and potential first hires?

Importantly and atypically, over half of our Q1 debt brokerage dealflow was on non-multifamily assets in retail, hospitality, industrial, and office. While some deals will need to be adjusted or even reworked, many deals remain on track. They have done this in the past and are doing this today.

Main Street issued a press release yesterday afternoon that details the company's second quarter financial and operating results. This document is available on the Investor Relations section of the company's website at mainstcapital.com. Please note that information reported on this call speaks only as of today, August 4, 2023.

Will Turner, Director – Fund Services, chats to Private Equity Wire about industry trends and some of the current challenges and opportunities facing the firm and its clients… PEW: Can you outline the industry trends which have been driving growth and development within your firm over the past year?

If we ever do get to the one-person unicorn, that’s going to be a lot of people trying to beat out Sequoia and Benchmark to fund its solitary round—a $2mm seed that it never looks back from for additional capital. When Roger Ehrenberg set out to professionalize his angel investing into a fund, he used “Data” as the theme.

Private equity deal sourcing is a bit like hunting for unicorns in a field of donkeys: everyone claims theyve discovered the secret sauce, but only a few actually have a process that worksand even those will admit that luck sometimes plays a role. Flexibility: Deals here allow for more creative structuring and tailored approaches.

The adjustments exclude the compensation expense impact of mark-to-market volatility associated with certain deferred cash compensation plans and the nonoperating impact of an economic hedge, which the company began in 2023. Lower incentive compensation and distribution and servicing costs were partially offset by higher direct fund expense.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content