This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Across the world, various economic development organizations, government agencies, and non-profits are putting in admirable and well-intentioned efforts to develop startup ecosystems. Everyone is excited when a new company gets funded in their ecosystem, but no one spends much time thinking about where the money comes from to fund that deal.

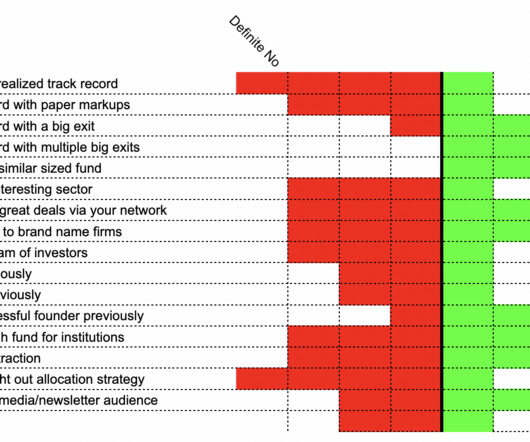

When I wrote this post about trying to measure the fundability of your startup, I kicked it off with, “You can’t” and proceeded to share all the ways that getting your company funded feels a bit like a craps shoot, while still trying find a method somewhere within the madness. Are you raising a size-appropriate fund?

These days, there are a ton of options for you if you''re a startup seeking guidence. Every single topic about running a company has been written about ad nauseum, there are incubators, accelorators, mentoring programs, events, talks, etc. Their guidance and network can also make these companies better. But what about investors?

I went back and calculated the number of companies in the first Brooklyn Bridge Ventures portfolio who have at least one founder who is female, from an underrepresented minority group, or LGBT. A whopping 17 of the 32 companies (53%) have founders that fit into those groups. So, yeah, it's quite a mix.

The startup ecosystem is a terrific manufacturer of bad fundraising advice. Well, if you add it to your startup, it does a few things. One, it usually implies that you’re going to start going cash flow negative to accelerate growth. Was she just an anomaly or is there something else going on here? That adds risk.

To be a good VC, you're going to offer up a lot of time to companies that may never pay back a dime--or even to deals you never wind up doing. There's no magic flow of great dealflow. You're going to spend a lot of time helping people that just aren't going to make it with their business. Start helping.

I believe that the next generation of top companies are far more likely to be founded by people not on VC radars today. Opening up our circle to create and scale genuine engagement for people outside of typical venture networks is how we do business—and we’re getting exceptional dealflow because of that.

across 159 investments into 107 companies. In addition to the fund, Super Angel Syndicate provides an opportunity to contribute more, from time to time, into individual companies via special purpose vehicles (SPVs). across 25 investments into 16 companies. I estimate the current value to be $10.3m which represents a 11.8%

At The Money: Finding Overlooked Private Investments , with Soraya Darabi, TMV (October 02, 2024) The Efficient Market Hypothesis informs us that stock markets reflect all of the information known about any company. But is that also true for start-ups and venture-funded private companies? And by the way, one quarter of U.S.

across 146 investments into 101 companies. In addition to the fund which is my primary vehicle, Super Angel Syndicate provides an opportunity for investors to contribute more, from time to time, into individual companies via special purpose vehicles (SPVs). across 25 investments into 16 companies.

People often ask me for advice on fundraising, generating dealflow, hiring, increasing visibility , triathlons, babies, etc.--a As is the case with any major company, career, or life function, the breadth of information one could pass along in each of these areas could fill a book. a really wide range of stuff.

Join a high-growth startup — The best way to learn to identify a future unicorn is to work for one. There’s a great, low-cost way to invest in early-stage companies even if you don’t have a trust fund or a prior 8-figure exit. Many syndicates are free to join and the best give you access to incredible dealflow.

Until you IPO, feeling like you’re good may just depend on what part of the fundraising cycle you’re taking a snapshot of your companies in. You're asked to participate in lectures and events at top tier academic institutions known for entrepreneurship and startups. A lot of people don’t feel today as they did two years ago.

She has been an early investor in companies that went public such as FIGS, Casper, and CloudFlare, as well as startups like Gimlett and Lightwell, that were later acquired by Spotify and Twitter. billion dollar startups have a founder who came here as a student. And by the way, one quarter of U.S.

When I started leading deals at First Round Capital, I sourced investments in 8 companies. We started talking about cycling and electronic shifters (which I definitely couldn’t afford) when he mentioned this new company. I don’t really have a particular goal with this post. I’m just sharing. Honestly, I hate fundraising.

Financing led by RA Capital Management with participation from Insight Partners, NVentures, Catalio Capital Management, Eli Lilly and Company, Gaingels, and Cooley LLP Funds to support clinical development of lead programs and expansion of small molecule pipeline focused on high-value GPCR targets BOSTON, Sept.

At this moment, I'm in the process of backing three companies that have at least one female founder and I just finished a round for a black female founder in December. Vetting dealflow is part of the job. Should more of those female founded companies have gotten funding, because they were better companies?

The story begins in 2010 after I started my first “venture-backed” company, only to shut it down four years later. I have invested the first checks into three companies that are each becoming category-defining, deployed $15 million from a collection of more than 300 LPs, and backed the founding teams of more than 100+ companies.

Per Cooley, “The average pre-money valuation for seed deals has remained relatively consistent since late 2021.” That said, these figures do not yet incorporate deals closed in Q4 2022, which, I believe will show a much more substantial decline in valuations for pre-seed and seed rounds than the preceding quarters of the year.

Last year resulted in a record-breaking year for deal volume on Axial, with 10,735 deals coming to market in 2024 a 7.8% The increase happened largely in the second half of the year, with both Q3 and Q4 resulting in 26% and 15% higher dealflow than the same periods in 2023, respectively.

And after we got into Y Combinator, basically the very first day, the general counsel who kind of keeps a watch over all the legal tech companies pulls us aside and is like, I don’t think your business idea is very good. A big perpetual insurance company versus lawyers come and go. Eva Shang : Exactly. There’s that John F.

It should not come as a surprise that when I invest in a company, even if I am already in constant communications with founders via other channels/formats, I expect them to send written updates. across 134 investments into 97 companies. buying shares from a company employee or another investor instead of from the company directly).

Uber’s ascent to the largest rideshare company in the world was fueled by a recurring cycle in which it blatantly ignored state and local laws, became entrenched and widely used in a community, and then tried to use its largesse to change the laws it was breaking." so they make up less than 10% of 10%. And investors? No current founders, pls.

He was a pre-IPO investor in companies like Facebook and Twitter. How does a kid from Arizona, from Phoenix, get interested in venture investing, not exactly known as a hotbed of early-stage tech companies. So indirectly, I became a hedge fund manager to manage our cash at the Squeeze Ball Company. LINDZON: Correct.

I was working directly with the CEO and president of both companies, but I realized that the biotech vertical was not my playing field for the long term, hence the NBA at Harvard to find another career path and, and that led me into asset management. I now, I’m chairperson of the board of a publicly listed company called SFC Energy.

Annie Lamont : So, when I joined Oak, which was really just a couple of years out of, out of Stanford, we were founding Genzyme the year that I joined one of the, also very first biotech companies. I said a number of dis drive companies, pc, I mean, we did actually invest in Compact during that period. I remember that one.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content