This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Resalecompany Winmark is a franchisor that owns concepts including Plato's Closet, Play It Again Sports, and Once Upon a Child. The company has tripled the return of the S&P 500 since its IPO, and delivered an annualized return of 18% over the past five years. So, investors may want to pay attention to it.

The resalecompany's capital allocation strategy and growth expectations. Brett Heffes: We have something that most companies crave and it's clarity of purpose. As I've mentioned earlier, we're Winmark the resalecompany and our mission is to provide resale for everyone. Right now we have about 1,300 stores.

Opendoor (NASDAQ: OPEN) seemed like a promising growth stock when it went public by merging with a special purpose acquisition company (SPAC) in Dec. The online real estate company streamlined home sales by making instant cash offers for homes, repairing those properties, and relisting them for sale on its online marketplace.

Wheaton Precious Metals (NYSE: WPM) is one of the larger streaming and royalty companies, competing with peers like Franco-Nevada (NYSE: FNV) and Royal Gold (NASDAQ: RGLD). That's where streaming and royalty companies like Wheaton come in. It earns money by offering the cut-price metals it buys for resale at market prices.

We are taking the right steps to shape DXC into a company that consistently delivers revenue growth and expanded margins, EPS, and free cash flow. In the quarter, we were impacted by a slowdown in customer expenditures, this is mainly the resale of IT equipment, such as PCs, networking gear and servers and project work. year to year.

Dividend-paying companies often demonstrate financial stability and a commitment to shareholder value, making them a reliable choice for long-term investors seeking income and capital appreciation. The annual yield of 0.73% isn't impressive on the surface, but the company has raised its dividend annually since 2004. million to 124.7

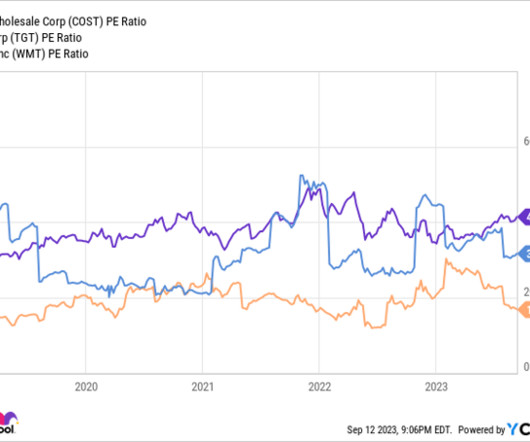

Two excellent examples are home improvement juggernaut The Home Depot (NYSE: HD) and resale goods franchisor Winmark (NASDAQ: WINA). HD and WINA Total Return Level data by YCharts This unstoppable up-and-to-the-right movement of the stocks' share price over time correlates nicely with each company's slow-and-steady compounding ways.

Measure on resales, Q4 industrial resales of $173 million declined 27% year on year. So, the reality going forward for this company is that the AI semiconductor business will rapidly outgrow the non-AI semiconductor business. billion of gross principal debt. We only expect a recovery in the second half of 2025.

In fact, last week, we held a well-attended VMware Explore Conference in Las Vegas, our first as a combined company. Finally, Q3 industrial resales of $164 million declined 31% year on year. We believe we are approaching bottom in Q3 as Q4 resales are expected to recover sequentially. billion of gross principal debt.

Finally, Q2 industrial resale of $234 million declined 10% year on year. And for fiscal '24, we now expect industrial resale to be down double-digit percentage year on year, compared to our prior guidance for high single-digit decline. billion of cash and 74 billion of gross debt. So, to sum it all up, here's what we are seeing.

I believe we have a global team that is reenergized to make the company better and more effective. In short, we are a key strategic technology partner, supporting global insurance companies with their customers, their agents, and their employees. This is a core competency of the company. Now, turning to our financial foundation.

03, 2023 Ricky Mulvey: What I've learned from this is I would not suggest setting up a hedge fund that is completely based on investing in companies based on stadium naming rights. Every time a stadium rights deal is announced, this fund buys $1,000 worth of stock in the purchasing company. There might be other factors at play.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon. Then you’ll want to hear this. points year to year to 8.2%

As usual, I'm going to give a macro and strategic overview of the company. The strategic benefits of driving volume came and will continue to come with advantages that are both immediately valuable, as well as durable for the company's future. homebuilding debt-to-total cap ratio with $6.3 Situated today with a 9.6%

While our company has an impressive collection of assets, technology, and people, it's clear that we need to sharpen our execution and accelerate our performance. I have learned that there are many compelling attributes of DXC that are either underappreciated or unknown outside the company. Organic revenue growth was down 4.5%

I'll start with a brief discussion covering current market conditions and some of our recent company milestones. News and World Report added us to the list of the 2024-2025 Best Companies to work for. And about 80% of our buyers in Q2 received some sort of financing incentives consistent with our mortgage company capture rate.

Finally, Q3 industrial resales of $236 million declined 3% year on year, reflecting weak demand in China. And in Q4, though, we expect an improvement with industrial resales up low single-digit percentage year on year, reflecting largely seasonality. And on a consolidated basis for the company, we're guiding Q4 revenue of 9.27

And finally, Q1 industrial resales of $215 million declined 6% year on year. In fiscal '24, we continue to expand industrial resales to be down high single digits year upon year. billion of gross debt. The weighted average coupon rate and years to maturity of our $48 billion in fixed-rate debt is 3.5% years, respectively.

Jessica Hansen -- Senior Vice President, Communications Forestar, our majority-owned residential lot development company reported revenues of $334 million for the second quarter on 3,289 lots sold with pre-tax income of $59 million. Forestar had approximately $800 million of liquidity at quarter end with a net debt to capital ratio of 16.4%.

Before we begin, I would like to remind everyone that this conference call may include forward-looking statements regarding the company's operating and financial performance in future periods. These statements are based on the company's current expectations and available information.

This migration allows greater process optimization across the company and provides timely, actionable insights for strategic decision-making to drive business performance. We believe our commitment to IP protection represents a cornerstone to company advancement and stakeholder value. Moving to GIS. The book-to-bill ratio was 0.67

[Operator instructions] The Children's Place issued its third-quarter 2023 earnings press release earlier this morning, and a copy of the release and presentation materials have been posted to the Investor Relations section of the company's website. On this call, the company will reference various non-GAAP financial measurements.

As usual, I'm going to give a macro and strategic overview of the company and our performance. We all reach that inevitable moment of retirement, but it is uncommon for that moment to coincide with the timing where the company is well prepared as well. debt to total capitalization, down from 13.3% This is that rare moment.

Howard and Andrew, combined with Chris, who runs ITO, gives us three former CXOs of Fortune 500 companies, leading almost 70% of our revenue. year-to-year decline, 160 basis points came from a reduced level of low-margin resale revenues, which was in line with our expectations. Debt levels decreased modestly in the first quarter to $4.5

On rare occasions, our expert team of analysts issues a Double Down stock recommendation for companies that they think are about to pop. Right now, were issuing Double Down alerts for three incredible companies, and there may not be another chance like this anytime soon. Total debt at the end of the quarter was equal to $3.8

Our return on assets ranks in the top 25% of all S&P 500 companies for the past three-, five- and 10-year periods. Forestar had approximately $860 million of liquidity at year-end with a net debt-to-capital ratio of 12.4%. FHA and VA loans accounted for 60% of the mortgage company's volume. Return on equity was 19.9%

As usual, I'm going to go ahead and give a macro and strategic overview of the company. debt to total capital capitalization ratio, down from 14.2 We expect to continue to generate considerable earnings and cash flow, and accordingly, we'll continue to retire debt and purchase stock optimistic -- opportunistically.

Jessica Hansen -- Vice President, Investor Relations Forestar, our majority-owned residential lot development company, reported revenues of $306 million for the first quarter on 3,150 lots sold, with pre-tax income of $51 million. Forestar had more than $840 million of liquidity at quarter-end with a net debt to capital ratio of 14.9%.

I'll remind listeners that this call contains forward-looking statements, including management's views on the company's business strategy, outlook, plans, objectives and guidance for future periods. billion of debt outstanding, including $819.7 million drawn on our credit facility, resulting in a debt-to-capital ratio of 43.8%

As you may recall, Loriann took the reins as CFO in addition to her role as COO effective March 1st at the start of the company's fiscal year, and I would personally like to welcome Loriann to today's call. The company assumes no responsibility to update any such forward-looking statements. Credit card debts are at all-time highs.

Today's call is being recorded, and a replay will be available on the company's website at www.lgihomes.com. Before we begin, I'll remind listeners that this call contains forward-looking statements, including management's views on the company's business strategy, outlook, plans, objectives, and guidance for future periods.

Before we begin, I would like to remind everyone that this conference call may include forward-looking statements regarding the company's operating and financial performance in future periods. These statements are based on the company's current expectations and available information.

Any forward-looking statements made on today's call represent management's current opinions, and the company assumes no obligation to update or supplement these statements because of subsequent events. Orange County, and Atlanta, both underperformed mainly for reasons related to bad debt, skips and evictions, and fraud. Similar to L.A.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon. Ricky Mulvey: Asit, this is a company with $9.4

I will start with a brief discussion about what we are seeing in the market and provide an overview of recent company milestones. And lastly, the resale home market remains tight as existing buyers are hesitant to leave their low rate mortgages, which limits available inventory and helps to increase new home demand. at June 30, 2023.

Industrial resales were 962 million. In fiscal '24, we expect industrial resales to be down low single digits year on year. billion of gross debt, of which 1.6 Harlan Sur -- JPMorgan Chase and Company -- Analyst Hey, good afternoon, and thanks for taking my question. We ended the fourth quarter with 14.2 billion EBITDA.

Operator instructions] To allow everyone an opportunity to ask a question, the company requests that each analyst only ask one question. See the 10 stocks *Stock Advisor returns as of January 16, 2024 Following management's perspective of the company's results, we will move to a Q&A session. Please go ahead, sir.

The company reports earnings tonight. Even if a lot of institutional investors don't, Paramount will still remain a publicly traded company. It really seems like nobody knows what's going to happen here and what happens to the company afterwards. billion in long term debt, just $2.5 Deidre Woollard: I'm doing OK.

I'll start with a brief discussion covering market trends and provide an overview of our recent company achievements. News and World Report's Best Companies to Work For and the Phoenix Business Journal's Best Places to Work, an honor for us in our hometown. Steve Hilton -- Executive Chairman Thank you, Emily. Now turning to Slide 7.

That said, the balance sheet remains an important priority, and I will talk about plans for further debt reduction in a few minutes. Our cost of capital synergy estimate assumed terming out Callon's $2 billion debt at APA's lower long-term cost of borrowing. billion three-year term loan to refinance this debt. Thanks a lot.

During the spring selling season with a healthy supply of move-in ready inventory, we were able to capitalize on strong market conditions generated by the increasing need for housing for millennials and Gen Zs as well as the move-down Baby Boomers who continue to find our limited inventory, limited availability of resale housing supply.

Earlier today, the company issued a press release comparing results of operations for the 13-week period ended August 3, 2024 to the 13-week period ended July 29, 2023. Additionally, please note that remarks made about the future expectations, plans and prospects of the company constitute forward-looking statements. Please go ahead.

We will maintain our disciplined approach to investing capital to enhance the long-term value of our company, including returning capital to our shareholders through both dividends and share repurchases on a consistent basis. Horton and had more than $780 million of liquidity at quarter end, with a net debt to capital ratio of 19.1%.

Declines at the mature Qasr gas field in Egypt and at Alpine High, where we have deferred drilling and completion activity, will result in total company natural gas production continuing to decline through the rest of this year. Charles Meade -- Johnson Rice and Company -- Analyst Good morning, John, to you and your whole team there.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content