This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The funds will focus on buyout and later-stage growth equity investments in middle market companies across Shamrock’s target sectors, seeking to capture Shamrock’s proprietary middle-market dealflow, thematic approach, and expertise, and value creation capabilities by utilising the same strategy Shamrock has implemented since 2001.

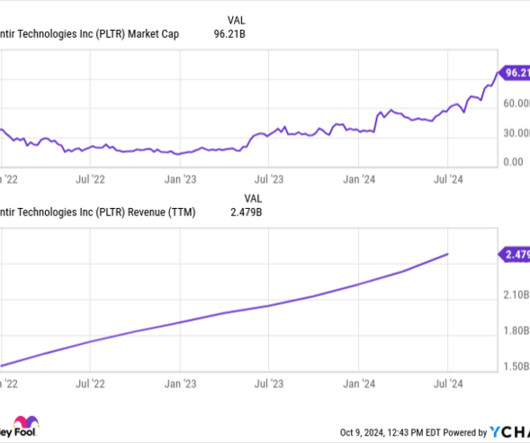

Institutional Coverage and Ownership: Back in September, Palantir reached a critical milestone as it was inducted into the S&P 500. Now that Palantir is part of the exclusive index, I would not be surprised to see the company receive more attention from large financialinstitutions.

LCP X is a 2022 vintage fund that is now more than 40% committed, with a diversified portfolio of more than 50 transactions with a variety of sellers, including public and corporate pensions, banks, and other financialinstitutions.

That said, we are seeing some signs of adverse market sentiment, particularly from large financialinstitutions in the United States that are impacting our revenue growth in the short-term as others in the space have also called out. There's not a lot of dealflow.

Our team's efforts continue to produce unique and proprietary dealflow, and we continue to identify attractive investment opportunities across all three external growth platforms. Our results for the quarter include the recognition of approximately $2 million of lease termination fees from a financialinstitution.

After college, I followed the conventional path of working at various large financialinstitutions in a number of roles. As far as what we are looking for, we’ve not had an issue with dealflow. I even took a stab at starting a dot-com company during the heyday which was my first foray into entrepreneurship.

We have a well-planned, balanced strategy that serves financialinstitution, crypto players and, of course, consumers to drive growth and provide choice in this space. I mean that's really subject to what kind of dealflow and deal activity we see.

There's also a variable around the sort of the level of dealflow a year ago and the benefit that comes from buying those funds at a discount to the fund returns in the short term. And the distributors, the big financialinstitutions recognize this as well. But long term, overall, it is an outstanding track record.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content